|

|

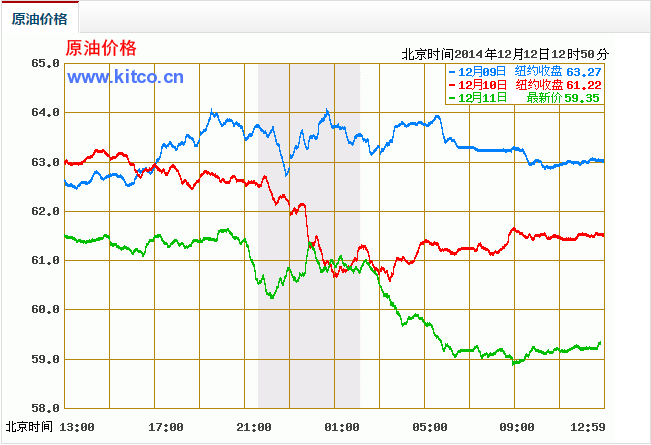

Oil

Dec 12, 2014 12:02:09 GMT 7

oldman likes this

Post by zuolun on Dec 12, 2014 12:02:09 GMT 7

|

|

|

|

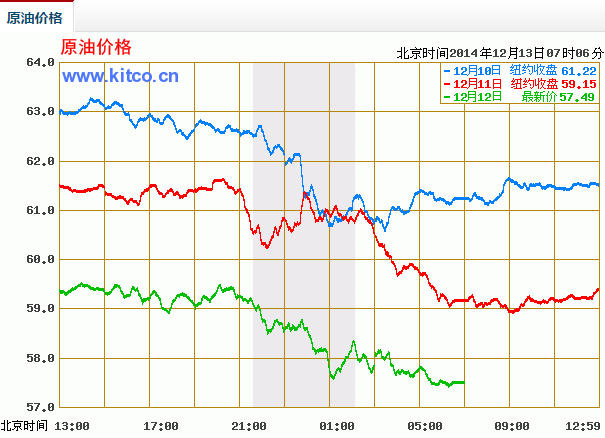

Oil

Dec 13, 2014 8:18:00 GMT 7

oldman likes this

Post by zuolun on Dec 13, 2014 8:18:00 GMT 7

|

|

|

|

Post by oldman on Dec 13, 2014 16:34:52 GMT 7

I think the oil crisis will last for at least a year. If it is resolved too quickly, the shale oil producers will make a comeback and the OPEC countries may not have achieved their objective. However, when the price of oil remain depressed, the most efficient shale gas producers will remain and these companies are likely to become oil giants of the future. When there is a crisis, only a handful of companies will survive but those that survive are likely to become blue chip oil companies of the future and they will buy up those that have fallen by the wayside. Eventually, I think that these low cost producers may make an impact that OPEC may not have foreseen and these companies may then dominate the oil industry worldwide. Yes, they have to thank OPEC for forcing down the price of oil and in return, they have to become more efficient to survive.. and later, to thrive. Yes, I do not share the common sentiments that OPEC will come up on top after the dust has settled. Only time will tell. As for identifying such companies, I don't have the expertise or knowledge as most of these companies are US based. Hence, I will give this potential opportunity a miss. And as far as the oil related companies are concerned, I will not rush to look for fallen angels now. Maybe in a year's time, I will re-look at these stocks. IMO, some good fundamental companies revenue and share price are pull down due to external factor like oil price. It may be a temporally setback to these companies. Yes, it is falling knife, but I will term as fallen angel. |

|

|

|

Post by oldman on Dec 14, 2014 13:47:05 GMT 7

Investing is about timing. Right now, I don't think it is the right time to get into oil related stocks. However, when these stocks have collapsed much further, there will come a time when I too will be interested. Let me expand my thoughts further. When you are a cartel, you have the power to increase the selling price and make more profits. When a cartel decides that it does not want to make more profits, one is best to sit up and ponder. The cartel will not take such a decision unless it feels strongly that its business model will be under significant pressures in the years ahead. Perhaps it is shale oil or alternative power sources but whatever it is, the cartel is willing to take short term pains to protect its long term interests.

Put another way, the cartel will know that unless it can persevere and hold down oil prices for at least a year or more, it is unlikely to be successful in its objective. Now, if you agree with this thought process, then, most of the oil related companies will be under pressure as future projects are likely be postponed and existing contracts may be rescind. Oil majors have significant powers and I am sure their contracts will allow them a way out, legally.

Oil related companies will then be under pressure from both revenues and profits and as they announce lower revs and profits, the market will punish these shares further. What I am saying is that it may be wiser to wait till later to then take positions in such companies. Investors need to be able to have their own crystal ball and forecast what is likely to happen in the future. More importantly, they must know how to position themselves to make money from their crystal ball gazing. In other words, smart investors will be looking into the fundamentals of oil related companies and will be following the oil market closely. He would have done his homework to determine an entry point. For a deep value investor like me, I will only enter at a very deep discount. If I were to hazard a guess, oil may hover around US$40 a barrel for a while.   "Given the fall in oil and commodity prices, I am inclined to classify all related stocks as potential falling knives." Hmmm, ... i wonder. During the 2008/09 crisis, oil price was falling off the cliff too. As would be expected during those periods of "falling knives", analysts were keen to join the herd and forecasting lower and lower prices of oil. As oil price were dipping towards $50/bbl, then $40/bbl, analysts and soothsayers were trying their utmost to outdo one another by being the more bearish. CNOOC, 883 HK, understandably crashed thru the roof, hurdling towards sub-HK$5 during the trough. Yet, if one had dilligently accumulated during those times, one would have done very well. Not too long ago when oil price was still at about $100/bbl, CNOOC was trading well above $20. And yes, you guessed it, the same herd of analysts were calling for big buys with target prices gunning towards $25-30/sh! With oil price having seen a sharp correction in the past two months, CNOOC is now barely holding at $10. I am no expert on oil price. Of course, the dynamics of the oil industry also appear to have changed with the advent and success of the shale evolution in recent times. Still, there must be an intrinsic value for oil. The question is finding out what that breakeven cost is, whether between the different exploration companies or between the traditional oil and shale. my point is, classifying all oil-related stocks as falling knives seem rather harsh. Just as spot oil could go up, come down, ... who could say it would not go up again? OPEC could decide to cut supply drastically, demand could pick up, a large number of the shale operators could be out of business. While it would be a tad optimistic to believe oil price could return to $100/bbl anytime soon, surely a price of $70/bbl isn't as out of reach as we think? Recall that when oil was $70/bbl, many of the oil majors would still be very profitable. |

|

|

|

Oil

Dec 14, 2014 14:24:06 GMT 7

oldman likes this

Post by zuolun on Dec 14, 2014 14:24:06 GMT 7

oldman, your comment is much appreciated. It reminds me of one of your postings, which has been proven right. "If big money sells at a significant loss, they must have their reasons." - oldmanIf oil goes lower and hover around US$40 a barrel then KepCorp's share price may hit S$4.08, the 78.6% FIBO level.  Investing is about timing. Right now, I don't think it is the right time to get into oil related stocks. However, when these stocks have collapsed much further, there will come a time when I too will be interested. Let me expand my thoughts further. When you are a cartel, you have the power to increase the selling price and make more profits. When a cartel decides that it does not want to make more profits, one is best to sit up and ponder. The cartel will not take such a decision unless it feels strongly that its business model will be under significant pressures in the years ahead. Perhaps it is shale oil or alternative power sources but whatever it is, the cartel is willing to take short term pains to protect its long term interests.

Put another way, the cartel will know that unless it can persevere and hold down oil prices for at least a year or more, it is unlikely to be successful in its objective. Now, if you agree with this thought process, then, most of the oil related companies will be under pressure as future projects are likely be postponed and existing contracts may be rescind. Oil majors have significant powers and I am sure their contracts will allow them a way out, legally.

Oil related companies will then be under pressure from both revenues and profits and as they announce lower revs and profits, the market will punish these shares further. What I am saying is that it may be wiser to wait till later to then take positions in such companies. Investors need to be able to have their own crystal ball and forecast what is likely to happen in the future. More importantly, they must know how to position themselves to make money from their crystal ball gazing. In other words, smart investors will be looking into the fundamentals of oil related companies and will be following the oil market closely. He would have done his homework to determine an entry point. For a deep value investor like me, I will only enter at a very deep discount. If I were to hazard a guess, oil may hover around US$40 a barrel for a while.

|

|

|

|

Post by gemini8 on Dec 14, 2014 14:33:00 GMT 7

Fair point.

I would agree that OPEC has not taken its recent decision to cut prices lightly. Clearly it seems prepared to take the necessary short term pains to maintain its market share and weed out the weaker shale operators and other alternative source(s).

Indeed, timing is important in investing; although there is another school of thought that trying to time the market is an impossible thing. At this juncture it also seems likely to me that the depressed state of the oil price would last for some time yet, but that would be a consensus view point, wouldn't it? And "consensus view" is invariably "dangerous"? ...anyhow, i am always wary, and question myself even more, when my view is consensus' view. Rem it wasn't so long ago when oil price was still hovering at $100/bbl, and v few were expecting it oil to take such a sharp turn on the downside, as it has done. My own gut feeling is that, while oil price is likely to remain depressed for a while yet, the share prices of some of the oil majors are beginning to look interesting. I am not talking about the likes of KepCorp in Singapore, which has not fallen as much vis-a-vis some of those in HK/China. Certainly, it is not inconceivable that oil price could fall further to $40/bbl, perhaps even $30/bbl, or worse ... but perhaps on the basis that one can never time the market to perfection (yes, not even mighty Warren Buffett, re XOM-US), an averaging strategy beginning with oil price at current levels (which has already declined 40% and counting), then at $50/bbl, $40bbl etc might make sense? ... Given a choice, everybody would wish to enter at "as deep a discount to intrinsic value" as possible; hence the saying "price is what you pay; value is what you get".

|

|

|

|

Post by oldman on Dec 14, 2014 14:42:26 GMT 7

Actually, investing is not difficult if you have the mindset that you are going to miss some good deals. You see, if oil does not crash further, I would have missed this opportunity. But this is OK, as there will be other opportunities. Most investors cannot take the pain of missing opportunities. I, on the other hand, know that I will miss many opportunities but will make up for it because I will eventually buy into an opportunity at a ridiculously low price... .which will then enable me to ride this all the way to the top. In the words of Warren Buffett, "You don’t have to swing at everything–you can wait for your pitch". I would then like to add that when you pitch, make sure you pitch BIG! Fair point. I would agree that OPEC has not taken its recent decision to cut prices lightly. Clearly it seems prepared to take the necessary short term pains to maintain its market share and weed out the weaker shale operators and other alternative source(s). Indeed, timing is important in investing; although there is another school of thought that trying to time the market is an impossible thing. At this juncture it also seems likely to me that the depressed state of the oil price would last for some time yet, but that would be a consensus view point, wouldn't it? And "consensus view" is invariably "dangerous"? ...anyhow, i am always wary, and question myself even more, when my view is consensus' view. Rem it wasn't so long ago when oil price was still hovering at $100/bbl, and v few were expecting it oil to take such a sharp turn on the downside, as it has done. My own gut feeling is that, while oil price is likely to remain depressed for a while yet, the share prices of some of the oil majors are beginning to look interesting. I am not talking about the likes of KepCorp in Singapore, which has not fallen as much vis-a-vis some of those in HK/China. Certainly, it is not inconceivable that oil price could fall further to $40/bbl, perhaps even $30/bbl, or worse ... but perhaps on the basis that one can never time the market to perfection (yes, not even mighty Warren Buffett, re XOM-US), an averaging strategy beginning with oil price at current levels (which has already declined 40% and counting), then at $50/bbl, $40bbl etc might make sense? ... Given a choice, everybody would wish to enter at "as deep a discount to intrinsic value" as possible; hence the saying "price is what you pay; value is what you get". |

|

|

|

Oil

Dec 14, 2014 15:23:07 GMT 7

oldman likes this

Post by zuolun on Dec 14, 2014 15:23:07 GMT 7

|

|

|

|

Oil

Dec 15, 2014 6:49:39 GMT 7

oldman likes this

Post by zuolun on Dec 15, 2014 6:49:39 GMT 7

Actually, investing is not difficult if you have the mindset that you are going to miss some good deals. You see, if oil does not crash further, I would have missed this opportunity. But this is OK, as there will be other opportunities. Most investors cannot take the pain of missing opportunities. I, on the other hand, know that I will miss many opportunities but will make up for it because I will eventually buy into an opportunity at a ridiculously low price... .which will then enable me to ride this all the way to the top. In the words of Warren Buffett, "You don’t have to swing at everything–you can wait for your pitch". I would then like to add that when you pitch, make sure you pitch BIG! , It may be a BIG bull trap instead of a great opportunity on oil and gas related stocks.  Chart watchers transfixed as oil trend lines die one by one Chart watchers transfixed as oil trend lines die one by one — 13 Dec 2014 Tumbling oil prices ripple across the globe — 13 Dec 2014 Santos directors double down on plunging stock — 12 Dec 2014 Santos to cut jobs, slash capital spending by $700m as oil prices slide — 12 Dec 2014 Slow demand, rising supply put further pressure on oil price - IEA — 12 Dec 2014 Cenovus Energy slashes spending by 15%, warns of deeper cuts — 11 Dec 2014 Goodrich, Oasis Petroleum cut spending for 2015 as oil slides — 10 Dec 2014 Market, not OPEC, will determine oil price: UAE official — 9 Dec 2014 Low oil prices could cut Alberta revenue by $7 billion — 9 Dec 2014 Tumbling oil prices set off alarm in Korea′s overseas construction orders — 2 Dec 2014 |

|

|

|

Post by oldman on Dec 15, 2014 10:56:30 GMT 7

zuolun , I am one terrible investor as I will only buy when the business comes for free and the company has net cash above its market cap. Ideally, it has no borrowings and has manageable cashflow. Yes, I am damn demanding as an investor, especially for the current oil related stocks.

|

|

|

|

Oil

Dec 15, 2014 13:11:38 GMT 7

oldman likes this

Post by zuolun on Dec 15, 2014 13:11:38 GMT 7

zuolun , I am one terrible investor as I will only buy when the business comes for free and the company has net cash above its market cap. Ideally, it has no borrowings and has manageable cashflow. Yes, I am damn demanding as an investor, especially for the current oil related stocks. , If a fundamentally strong stock collapsed into uncharted territory, I'll normally reassess the survival strength of the co's management staffs (past and present)...when my charts fail to give me a decisive buy signal / confirmation on when to buy. Malaysian Chinese Business: Who Survived the Crisis? — Oct 2003 |

|

|

|

Post by oldman on Dec 15, 2014 13:38:06 GMT 7

As I grow older as an investor, I become even more careful with my investments. Agree that the ability of a fallen angel to survive is critical. Frankly, this is easier to assess than the sincerity of management. I have been caught in situations where management just takes care of themselves at the expense of minority shareholders. You may be surprised that my experience is that it is not easy to find management who are honest and ethical and will take care of the interests of minority shareholders. When I find one, I am now more likely to remain committed as a shareholder. zuolun , I am one terrible investor as I will only buy when the business comes for free and the company has net cash above its market cap. Ideally, it has no borrowings and has manageable cashflow. Yes, I am damn demanding as an investor, especially for the current oil related stocks. , If a fundamentally strong stock collapsed into uncharted territory, I'll normally reassess the survival strength of the co's management staffs (past and present)...when my charts fail to give me a decisive buy signal / confirmation on when to buy. Malaysian Chinese Business: Who Survived the Crisis? — Oct 2003 |

|

|

|

Oil

Dec 15, 2014 13:46:11 GMT 7

zuolun likes this

Post by oldman on Dec 15, 2014 13:46:11 GMT 7

zuolun , the videos are really good stuff. I learnt a lot from these videos on the 7 sisters. Thank you very much.

|

|

|

|

Post by zuolun on Dec 15, 2014 13:59:30 GMT 7

As I grow older as an investor, I become even more careful with my investments. Agree that the ability of a fallen angel to survive is critical. Frankly, this is easier to assess than the sincerity of management. I have been caught in situations where management just takes care of themselves at the expense of minority shareholders. You may be surprised that my experience is that it is not easy to find management who are honest and ethical and will take care of the interests of minority shareholders. When I find one, I am now more likely to remain committed as a shareholder. One of Warren Buffett's famous quotes.  |

|

|

|

Oil

Dec 15, 2014 14:16:14 GMT 7

oldman likes this

Post by zuolun on Dec 15, 2014 14:16:14 GMT 7

zuolun , the videos are really good stuff. I learnt a lot from these videos on the 7 sisters. Thank you very much. , I'm glad that you made an effort to watch all of them. I believed many readers wouldn't be interested watching the 7 sisters because of the duration of each video clip... |

|