China’s debt turned a corner (and no-one noticed)The increase in China’s debt grabbed headlines worldwide – the turnaround is yet to receive much attentionBy David Mann

31 Mar 2015

Much of the negativity about world growth prospects at the moment seems to stem from the absence of a credit boom in any major market and worries over the consequences of higher US interest rates for the first time since 2006.

The lack of a credit boom means that growth is more subdued than it was in the run-up to the global financial crisis.

Positive signsIn particular, there are fears about China’s growth prospects, given the recent bad news concerning weak credit demand, high real interest rates and tight liquidity. However, we see three reasons for at least some optimism:

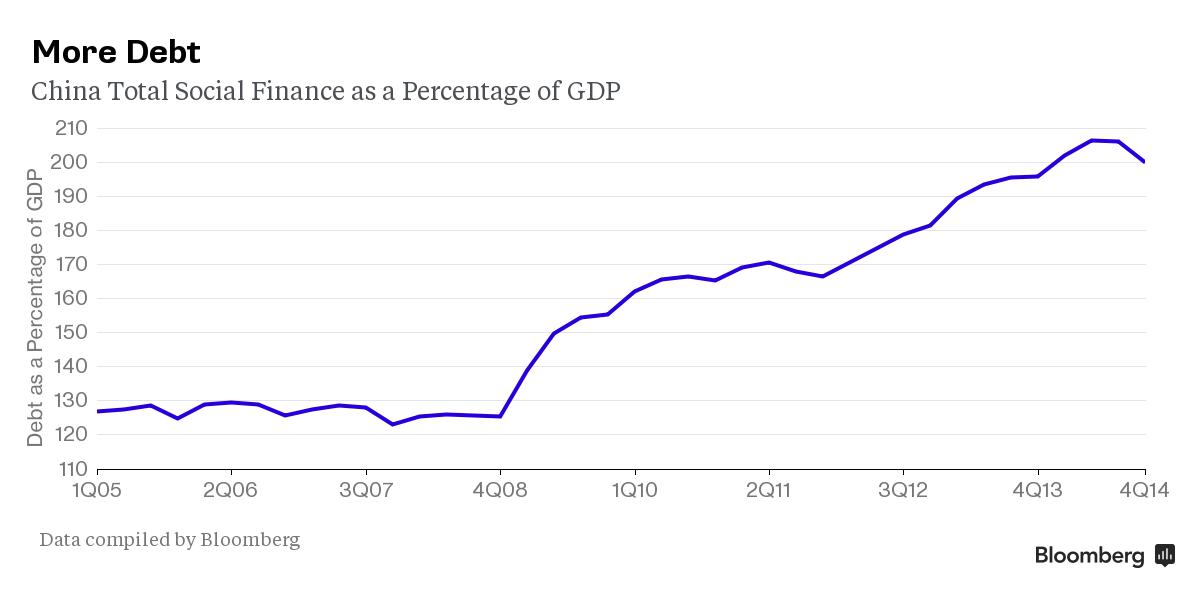

First, China’s debt-to-GDP ratio stabilised as of mid-2014, albeit at a relatively high 251 per cent of GDP.

While China’s dramatic debt increases of the past five years grabbed headlines worldwide, as the ratio leapt nearly 100 percentage points from 155 per cent of GDP, the fact the ratio has begun to stabilise has not yet received much attention.

This is an important milestone in China’s debt turnaround, following years of excess. Over the past five years, total credit growth in China was on average 8 percentage points faster than nominal GDP growth – way beyond the point at which credit growth becomes inefficient for any economy.

Since mid-2014, China’s credit has been growing in line with GDPHowever, since mid-2014, China’s credit has been growing in line with GDP. Essentially, this means China is now getting more ‘bang for its buck’ for every new unit of borrowing. Also, attitudes to debt have changed, with loan officers in China much more averse now to taking the risk of a loan going bad than previously.

While this doesn’t mean that China’s leverage risks have been resolved, as the excessive debt accumulation of prior years still needs to be dealt with, it does mean that debt challenges are no longer escalating, which is good news.

Resuming past excesses is not an option. China’s debt-to-GDP ratio is still relatively high compared with other economies at a similar stage of development, so debt cannot be used to boost growth significantly in the near future without risking even more solvency issues later.

The official non-performing loan ratio is set to keep rising through 2015 and beyond. Most likely not all of the bad debt will be recognised immediately, which comes with both benefits and potential costs.

On the upside, we are unlikely to see a sudden jump in China’s non-performing loan ratio, which could have led to a possible market panic.

On the downside, those unrecognised bad loans may mean that interest costs are turned into principle and count towards new credit growth. Unfortunately, by definition this part of credit growth is not going to generate new GDP.

A careful watchWe will need to watch carefully whether this ‘evergreening’ of bad loans becomes too large a share of new credit growth. Importantly, this does not appear to be the case so far.

The second reason to be a bit more upbeat about China is the sign of positive sentiment among property developers. Results of our recent property market survey of 30 companies in five major cities around China – which we have been running twice a year since 2010 – indicate that the industry will be in better shape by the second half of 2015, which bodes well for China’s growth.

Developers believe the excessive amount of inventory in lower-tier cities will be worked through by the second half of 2015. They also anticipate better appetite for land investment among their peers before the end of this year. This is good news, given the drag on GDP growth from the sector recently.

While we all should be getting used to China’s ‘new normal’ of slower growth we should not be worried about the slowdown deepening even furtherFinally, our SME survey of over 600 companies across China showed a slight improvement in sentiment in January from a low in December.

The results indicate that this optimism is being supported by broad-based policy easing in China. And, as we expect to see more monetary easing in the form of at least two more reserve requirement ratio cuts and a further lowering of policy rates, business confidence could continue to improve.

While we all should be getting used to China’s ‘new normal’ of slower growth we should not be worried about the slowdown deepening even further in 2015 and 2016.

Reforms will drive growthThere are many reasons to be less bearish on China than the present consensus, and the fact that there is no unsustainable credit booming taking off again in China, or anywhere else in the world’s major economies, should be a source of relief.

Growth of 7 per cent annually means that GDP doubles every 10 years – a very respectable rate for any economy at China’s present stage of development. While by no means guaranteed, we are also waiting for potential growth-boosting measures over the longer term from structural reform of rural land, the ‘hukou’ system and the state owned enterprise sector.

We are also encouraged by the planned CNY 1 trillion debt swap initiative, which aims to convert more than 50 per cent of the local government due for re-financing in 2015 into lower interest cost bonds.

In the meantime, expect financial reforms from China in 2015 to help shift its allocation of capital even more towards being determined by market forces – making growth more sustainable.