BoJ fears for JPY ~ 11 Feb 2016

Dollar pushes higher as Yellen remarks support ~ 10 Feb 2016

Yen soars, triggering alarm and major stock sell-off in Tokyo ~ 10 Feb 2016

Mexico peso hits record low, analysts blame bondholders ~ 9 Feb 2016

Rupee volatility rises most in a week on India stock selloff ~ 9 Feb 2016

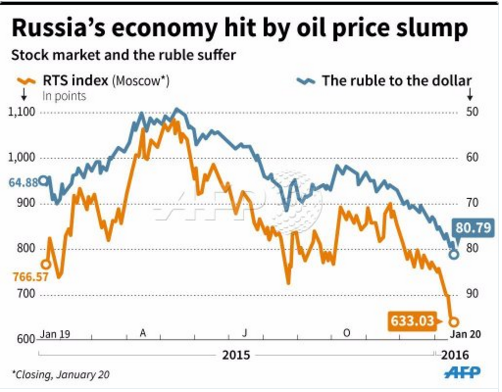

The Ruble's never moved this much in sync with crude oil: Chart ~ 9 Feb 2016

It’s always about the Yen...

It’s always about the Yen... ~ 8 Feb 2016

USD/JPY: Things could get ugly ~ 8 Feb 2016

USD/CAD rises on sustained oil rout ~ 8 Feb 2016

US$100bn to support the pound after Brexit ~ 8 Feb 2016

Dollar drops to 1-year low vs. yen as oil prices fall ~ 8 Feb 2016

GM suspends Egypt operations due to currency crisis ~ 8 Feb 2016

Japan stocks gain as Yen weakens against dollar after payrolls ~ 8 Feb 2016

Emerging stocks drop with oil; currencies slump against dollar ~ 8 Feb 2016

Saudi currency devaluation would carry major political risk ~ 5 Feb 2016

USD/JPY rejected at 117, reverts to 2-week lows ~ 5 Feb 2016

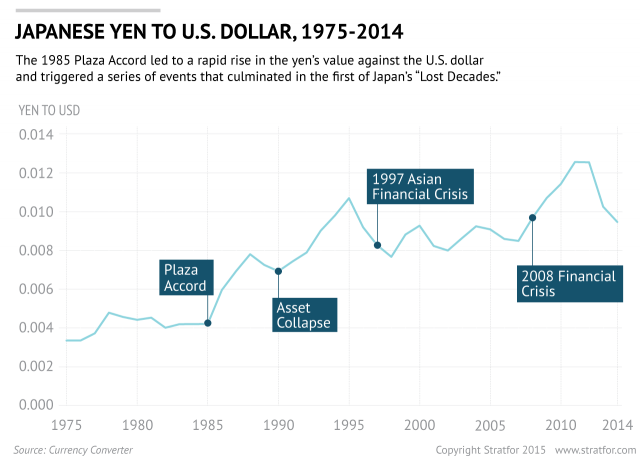

Japan’s wrong way out ~ 5 Feb 2016

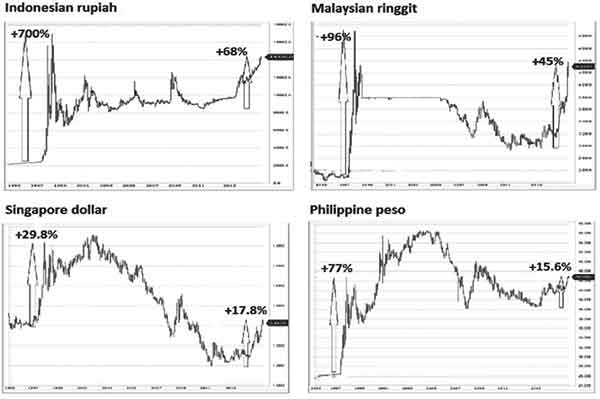

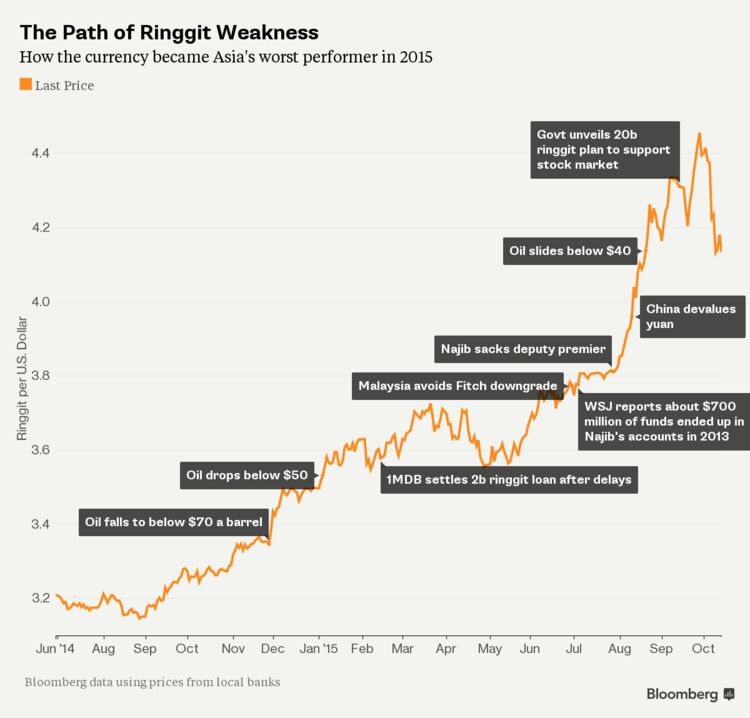

Malaysian Ringgit: A dead cat bounce? ~ 3 Feb 2016

Dollar weakens amid falling yields and rising growth fears ~ 3 Feb 2016

Why Saudi Arabia's 3 decade old currency peg will fall in 2016 ~ 4 Feb 2016

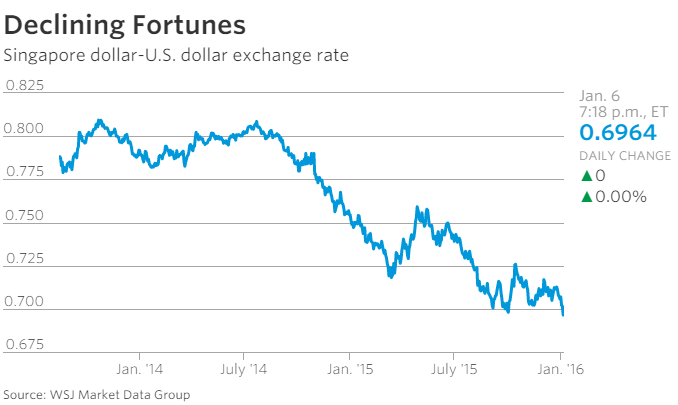

Hong Kong’s dollar peg: Next in the firing line?

Hong Kong’s dollar peg: Next in the firing line? ~ 25 Jan 2016

Relax, the Hong Kong dollar peg is not in any danger ~ 21 Jan 2016

Hong Kong Monetary Authority vows short sellers will not find it easy to mount assault on Hong Kong dollarBy Eric Ng

27 Jan 2016

A more robust system for local banks to obtain liquidity and an enlarged monetary base make it near impossible for currency speculators to mount a successful attack on the Hong Kong currency, according to the Hong Kong Monetary Authority, which said there’s few parallels with conditions today and those in 1997 to 1998 which saw authorities launch a shock and awe defence of the financial system at the height of the Asian financial crisis.

Howard Lee, the HKMA’s executive director responsible for monetary management, said the changed circumstances compared to almost 20 years ago when the crisis happened means it is more difficult for speculators to short-sell the Hong Kong dollar to push up interest rates and cause wider financial markets turbulence. To do so would require speculators to muster hundreds of billions of Hong Kong dollars.

“It is now very difficult for “double play” to work because the Hong Kong dollar monetary base is now much bigger than that in 1997-98,” he said in a statement posted on the authority’s web site on Wednesday.

Double play refers to the strategy used by speculators in the Asian crisis of shorting stocks and Hang Seng Index futures, followed by short-selling of Hong Kong dollar to push up interest rates, so as to create panic in the wider financial markets to reap huge profits on stocks and index futures and currency bets.

Lee said unlike in 1998 when the Hang Seng Index comprised primarily interest rates sensitive property and bank plays, it has a much broader industry representation and is less sensitive to interest rate movements.

Hong Kong stocks are also much cheaper based on price-to-earnings and price-to-book value multiples compared to 1997, leaving less room for speculative attacks to succeed.

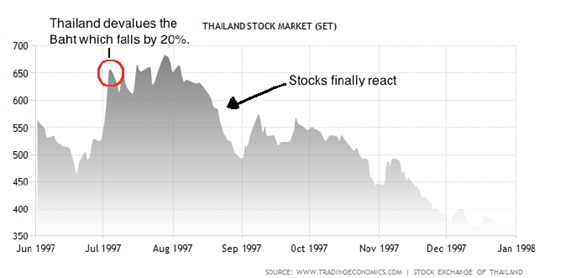

His comments came after recent weakness of the Hong Kong dollar, the yuan and local stocks. Some have expressed concerns about a re-run of the Asian crisis which began in Thailand and spread like a contagion across the region, with sharp increases in interest rates pushing Hong Kong stock and property prices lower, eventually leading to a painful, protracted recession.

It also came after George Soros, who gained fame for his success speculating against the British pound in 1992 and the Malaysian ringgit and Thai baht in the Asian financial crisis of 1997/98, said last week that a hard landing in the Chinese economy was “unavoidable” and that he was shorting Asian currencies.

Chinese state media Xinhua this week warned those engaging in “reckless speculation and vicious shorting will face higher trading costs and possibly severe legal consequences.

Lee said recent Hong Kong dollar weakness “is a normal phenomenon amid widening interest rate differentials between the Hong Kong dollar and US dollar after the US rate hike.”

The Hong Kong dollar 12-month futures traded as low as 7.89 last week, the weakest since 1999, igniting concerns over whether the currency peg would remain in place. [The Hong Kong Monetary Authority (HKMA) Chief Executive, Norman Chan Tak-lam attends a press conference to announce the investment results of the Exchange Fund as of the end of 2015 at HKMA in Central. Photo: K. Y. Cheng, SCMP] The Hong Kong Monetary Authority (HKMA) Chief Executive, Norman Chan Tak-lam attends a press conference to announce the investment results of the Exchange Fund as of the end of 2015 at HKMA in Central. Photo: K. Y. Cheng, SCMP

“The weakening of the Hong Kong dollar forward rate to below 7.85 does not mean that the market is speculating on an imminent depeg of the Hong Kong dollar with the US dollar,” Lee said.

He noted that Hong Kong’s current monetary base of HK$1.6 trillion far exceeds the HK$190 billion in 1998. The city’s foreign reserves of US$360 billion significantly outpace the US$70-US$90 billion in 1998.

The HKMA’s introduction of a mechanism in 1998 to provide banks access to overnight Hong Kong dollar liquidity via repurchase transactions using Exchange Fund bills and notes that currently amounts toHK$850 billion, has also dampened excessive volatility in interest rates, he added.

He also sought to allay fears that interest rates will soar to levels reminiscent to the 280 per cent overnight Hong Kong inter-bank offered rate (Hibor) seen during the Asian crisis.

“We expect that even if the Hong Kong dollar interbank rates would continue to rise in response to [fund]outflows, the pace of the increase would not be as rapid as that seen in 1997-98,” he said.