|

|

Post by zuolun on Mar 27, 2015 14:45:49 GMT 7

|

|

|

|

Post by zuolun on Apr 22, 2015 9:25:13 GMT 7

|

|

|

|

Post by zuolun on Apr 24, 2015 17:40:19 GMT 7

|

|

|

|

Post by zuolun on May 1, 2015 19:17:52 GMT 7

|

|

|

|

Post by sptl123 on May 1, 2015 23:02:46 GMT 7

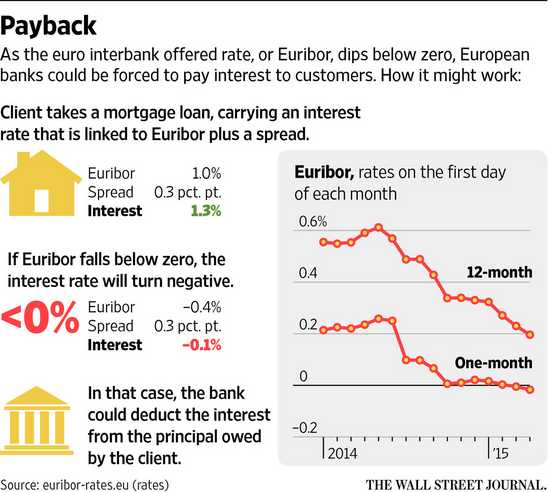

Bro Zuolun, I am also astonished to learned that more than 30% ( 2 trillion) of all government debt in the eurozone – is trading on a negative interest rate. We all know that yield and bond price has an inverse relationship. When one buy a bond at PAR, yield is equal to interest rate. Coupon rate is fixed, so when price goes up, yield drop and when price down, yield up. Normally higher yield signal a lack of confident for a given bond, lower yield because there were more buyers than sellers and people are welling to pay more for the quality of a bond. These are commonsense so far. If we put the maturity aside, when we say negative interest rate, it means someone pay $ 106 or more for a $ 100 par value bond which has a coupon rate of 5%. Why would people want to do that? Unless he expect the price will be $ 107 or higher in the future? But at the price of $ 106, the yield is already -1% and why would the next buyer or any one want to invest something for gain of -2%, -3% or something make them poorer.......? Something economists thought was impossible is happening in EuropeAfter reading the above, I still do not fully understand. |

|

|

|

Post by zuolun on May 2, 2015 7:09:25 GMT 7

Bro Zuolun, I am also astonished to learned that more than 30% ( 2 trillion) of all government debt in the eurozone – is trading on a negative interest rate. We all know that yield and bond price has an inverse relationship. When one buy a bond at PAR, yield is equal to interest rate. Coupon rate is fixed, so when price goes up, yield drop and when price down, yield up. Normally higher yield signal a lack of confident for a given bond, lower yield because there were more buyers than sellers and people are welling to pay more for the quality of a bond. These are commonsense so far. If we put the maturity aside, when we say negative interest rate, it means someone pay $ 106 or more for a $ 100 par value bond which has a coupon rate of 5%. Why would people want to do that? Unless he expect the price will be $ 107 or higher in the future? But at the price of $ 106, the yield is already -1% and why would the next buyer or any one want to invest something for gain of -2%, -3% or something make them poorer.......? Something economists thought was impossible is happening in EuropeAfter reading the above, I still do not fully understand. , To fully understand this unusual phenomena, read Usury, 0% interest rates, and worthless currencies.  解铃还需系铃人。 解铃还需系铃人。 To solve and end a complex problem, the root cause must be fixed by the same person who created it. Bangladesh’s central banker: QE doesn’t workBy Jonathan Wheatle 6 Feb 2015 Developed country central banks that see quantitative easing as a route to recovery are merely inflating bubbles, driving up the prices of assets held by rich people and failing to deliver growth on the ground. So says Atiur Rahman, governor of the central bank of Bangladesh. “QE will lead to bubbles and overheating,” he said during a visit to beyondbrics on Friday. “They are creating liquidity in the air and never really touching the ground.” Rahman was in London to receive an award as central banker of the year in the Asia-Pacific region from The Banker, an FT publication, in recognition of his achievement in supporting lending to farmers and small and medium-sized enterprises (SMEs) without compromising growth and macroeconomic stability. He said such policies should be pursued by other central banks who had failed to drive lending to the productive parts of their economies. “Mervyn King [governor of the Bank if England for 10 years until July 2013] used to lament that he was not reaching SMEs,” Rahman said. “I am worried that QE is only going to the banks, not to the real economy.” He said initiatives launched under his tenure had resulted in about a quarter of all credit in Bangladesh going to SMEs, of which 10 to 15 per cent was in the form of directed credit mandated and supplied by the central bank. Funds were provided by the bank at its base rate of 5 per cent a year, and loaned on by commercial banks at an additional 5 per cent to SMEs led by men and 4 per cent to SMEs led by women, in an effort to encourage female participation in the economy. “At first the banks were reluctant but now they recognise that lending to SMEs is a good business,” he said. Banks were typically lending their own funds to SMEs at interest rates of about 15 per cent a year, compared with an average corporate lending rate of about 12.5 per cent. He said a culture of micro-finance built up over many years in Bangladesh by pioneers such as the Grameen Bank had laid the ground for expanding finance to SMEs and other parts of the economy previously outside the financial system. He said 80 per cent of adults in Bangladesh now had bank accounts, up from about 55 per cent five years ago. The assets of the banking system had risen from the equivalent of 57 per cent of GDP in 2009 to 72 per cent of GDP in 2014. But even in Bangladesh, authorities had previously been slow to encourage lending to small businesses, especially in rural areas. “None of the nine central bank governors before me ever went out to the rural areas,” Rahman said. He had made 101 visits to rural areas over the past four years, mostly at weekends. “You have to get out and visit people, go into their houses, to see what programmes are needed, ” he said. “Central bankers in the advanced economies are not going out to see their economies on the ground.” |

|

|

|

Post by zuolun on May 4, 2015 4:40:22 GMT 7

Satyajit Das on elite robbing 99%Bro Zuolun, I am also astonished to learned that more than 30% ( 2 trillion) of all government debt in the eurozone – is trading on a negative interest rate. We all know that yield and bond price has an inverse relationship. When one buy a bond at PAR, yield is equal to interest rate. Coupon rate is fixed, so when price goes up, yield drop and when price down, yield up. Normally higher yield signal a lack of confident for a given bond, lower yield because there were more buyers than sellers and people are welling to pay more for the quality of a bond. These are commonsense so far. If we put the maturity aside, when we say negative interest rate, it means someone pay $ 106 or more for a $ 100 par value bond which has a coupon rate of 5%. Why would people want to do that? Unless he expect the price will be $ 107 or higher in the future? But at the price of $ 106, the yield is already -1% and why would the next buyer or any one want to invest something for gain of -2%, -3% or something make them poorer.......? Something economists thought was impossible is happening in EuropeAfter reading the above, I still do not fully understand. , To fully understand this unusual phenomena, read Usury, 0% interest rates, and worthless currencies. 解铃还需系铃人。 To solve and end a complex problem, the root cause must be fixed by the same person who created it. Bangladesh’s central banker: QE doesn’t workBy Jonathan Wheatle 6 Feb 2015 Developed country central banks that see quantitative easing as a route to recovery are merely inflating bubbles, driving up the prices of assets held by rich people and failing to deliver growth on the ground. So says Atiur Rahman, governor of the central bank of Bangladesh. “QE will lead to bubbles and overheating,” he said during a visit to beyondbrics on Friday. “They are creating liquidity in the air and never really touching the ground.” Rahman was in London to receive an award as central banker of the year in the Asia-Pacific region from The Banker, an FT publication, in recognition of his achievement in supporting lending to farmers and small and medium-sized enterprises (SMEs) without compromising growth and macroeconomic stability. He said such policies should be pursued by other central banks who had failed to drive lending to the productive parts of their economies. “Mervyn King [governor of the Bank if England for 10 years until July 2013] used to lament that he was not reaching SMEs,” Rahman said. “I am worried that QE is only going to the banks, not to the real economy.” He said initiatives launched under his tenure had resulted in about a quarter of all credit in Bangladesh going to SMEs, of which 10 to 15 per cent was in the form of directed credit mandated and supplied by the central bank. Funds were provided by the bank at its base rate of 5 per cent a year, and loaned on by commercial banks at an additional 5 per cent to SMEs led by men and 4 per cent to SMEs led by women, in an effort to encourage female participation in the economy. “At first the banks were reluctant but now they recognise that lending to SMEs is a good business,” he said. Banks were typically lending their own funds to SMEs at interest rates of about 15 per cent a year, compared with an average corporate lending rate of about 12.5 per cent. He said a culture of micro-finance built up over many years in Bangladesh by pioneers such as the Grameen Bank had laid the ground for expanding finance to SMEs and other parts of the economy previously outside the financial system. He said 80 per cent of adults in Bangladesh now had bank accounts, up from about 55 per cent five years ago. The assets of the banking system had risen from the equivalent of 57 per cent of GDP in 2009 to 72 per cent of GDP in 2014. But even in Bangladesh, authorities had previously been slow to encourage lending to small businesses, especially in rural areas. “None of the nine central bank governors before me ever went out to the rural areas,” Rahman said. He had made 101 visits to rural areas over the past four years, mostly at weekends. “You have to get out and visit people, go into their houses, to see what programmes are needed, ” he said. “Central bankers in the advanced economies are not going out to see their economies on the ground.”

|

|

|

|

Post by zuolun on May 5, 2015 15:09:52 GMT 7

|

|

|

|

Post by zuolun on May 5, 2015 21:52:40 GMT 7

The rich get richer ~ 4 May 2015 Bangladesh’s central banker: QE doesn’t workBy Jonathan Wheatle 6 Feb 2015 Developed country central banks that see quantitative easing as a route to recovery are merely inflating bubbles, driving up the prices of assets held by rich people and failing to deliver growth on the ground. So says Atiur Rahman, governor of the central bank of Bangladesh. “QE will lead to bubbles and overheating,” he said during a visit to beyondbrics on Friday. “They are creating liquidity in the air and never really touching the ground.” Rahman was in London to receive an award as central banker of the year in the Asia-Pacific region from The Banker, an FT publication, in recognition of his achievement in supporting lending to farmers and small and medium-sized enterprises (SMEs) without compromising growth and macroeconomic stability. He said such policies should be pursued by other central banks who had failed to drive lending to the productive parts of their economies. “Mervyn King [governor of the Bank if England for 10 years until July 2013] used to lament that he was not reaching SMEs,” Rahman said. “I am worried that QE is only going to the banks, not to the real economy.” He said initiatives launched under his tenure had resulted in about a quarter of all credit in Bangladesh going to SMEs, of which 10 to 15 per cent was in the form of directed credit mandated and supplied by the central bank. Funds were provided by the bank at its base rate of 5 per cent a year, and loaned on by commercial banks at an additional 5 per cent to SMEs led by men and 4 per cent to SMEs led by women, in an effort to encourage female participation in the economy. “At first the banks were reluctant but now they recognise that lending to SMEs is a good business,” he said. Banks were typically lending their own funds to SMEs at interest rates of about 15 per cent a year, compared with an average corporate lending rate of about 12.5 per cent. He said a culture of micro-finance built up over many years in Bangladesh by pioneers such as the Grameen Bank had laid the ground for expanding finance to SMEs and other parts of the economy previously outside the financial system. He said 80 per cent of adults in Bangladesh now had bank accounts, up from about 55 per cent five years ago. The assets of the banking system had risen from the equivalent of 57 per cent of GDP in 2009 to 72 per cent of GDP in 2014. But even in Bangladesh, authorities had previously been slow to encourage lending to small businesses, especially in rural areas. “None of the nine central bank governors before me ever went out to the rural areas,” Rahman said. He had made 101 visits to rural areas over the past four years, mostly at weekends. “You have to get out and visit people, go into their houses, to see what programmes are needed, ” he said. “Central bankers in the advanced economies are not going out to see their economies on the ground.”

|

|

|

|

Post by zuolun on May 8, 2015 4:24:51 GMT 7

|

|

|

|

Post by zuolun on May 11, 2015 6:52:24 GMT 7

|

|

|

|

Post by zuolun on Jun 10, 2015 5:12:00 GMT 7

|

|

|

|

Post by zuolun on Jun 14, 2015 7:14:30 GMT 7

|

|

|

|

Post by zuolun on Jun 15, 2015 10:03:25 GMT 7

|

|

|

|

Post by zuolun on Jun 23, 2015 15:47:18 GMT 7

|

|