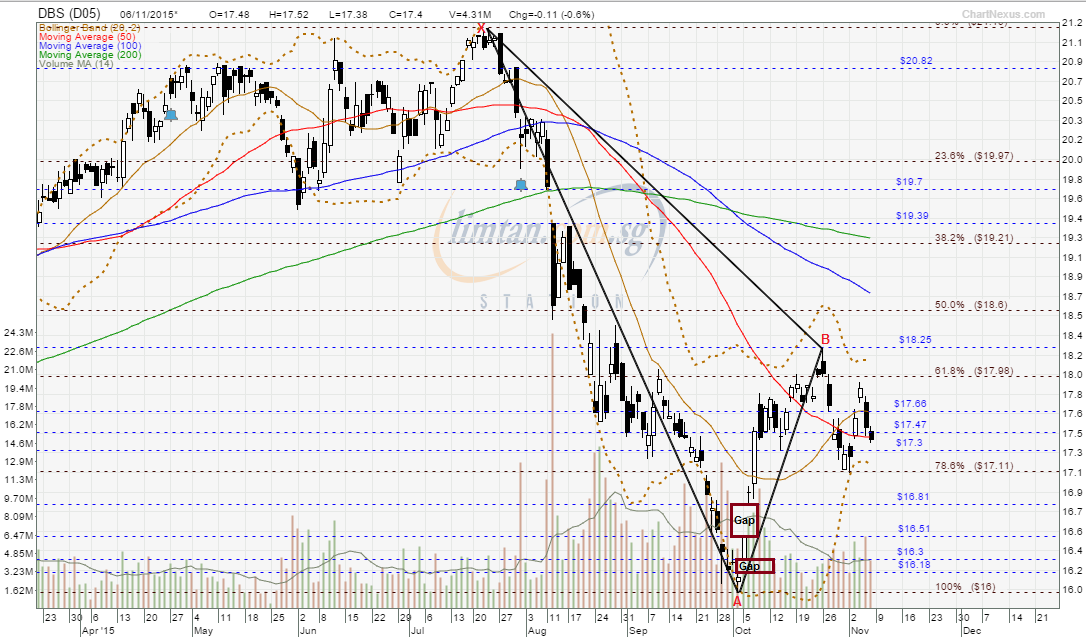

Short Singapore BanksDBS ~

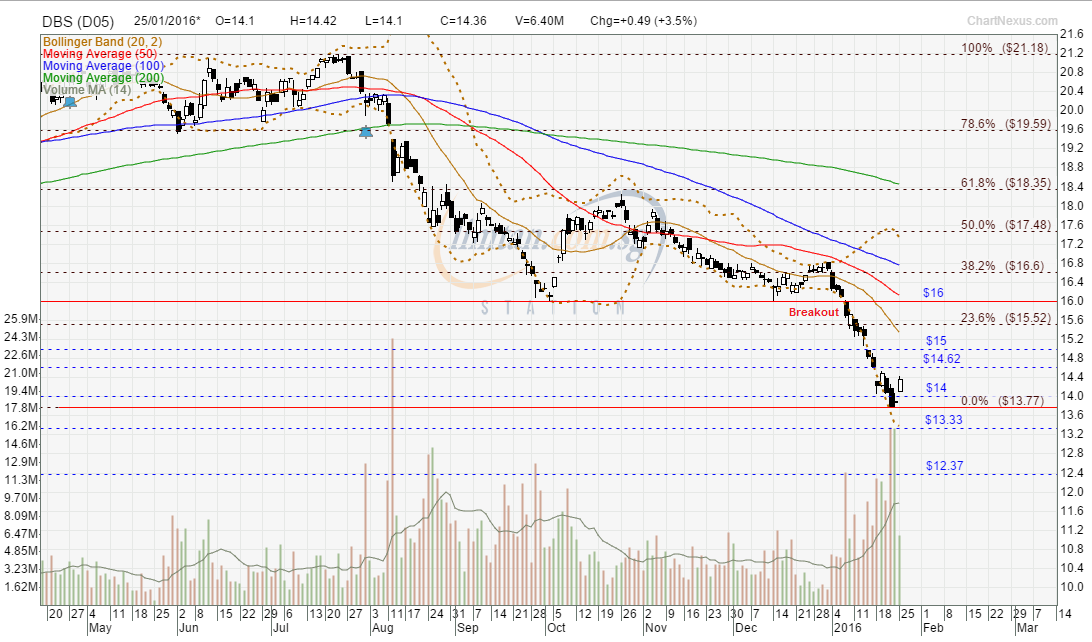

Major bearish trend reversal with 5-wave down, interim TP S$11.20DBS gapped down with a black marubozu and traded @ S$13.50

(-0.28, -2%) with 6.68m shares done on 2 Feb 2016 at 1420 hrs.

Immediate support @ S$13.33, immediate resistance @ S$13.71.

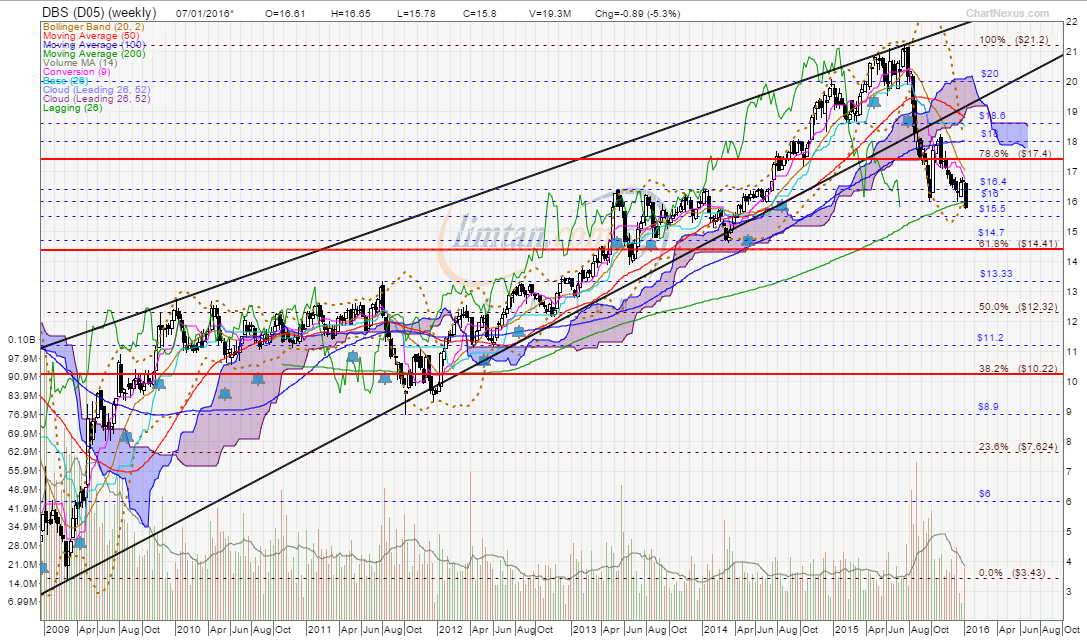

DBS (weekly) chart pattern is similar to

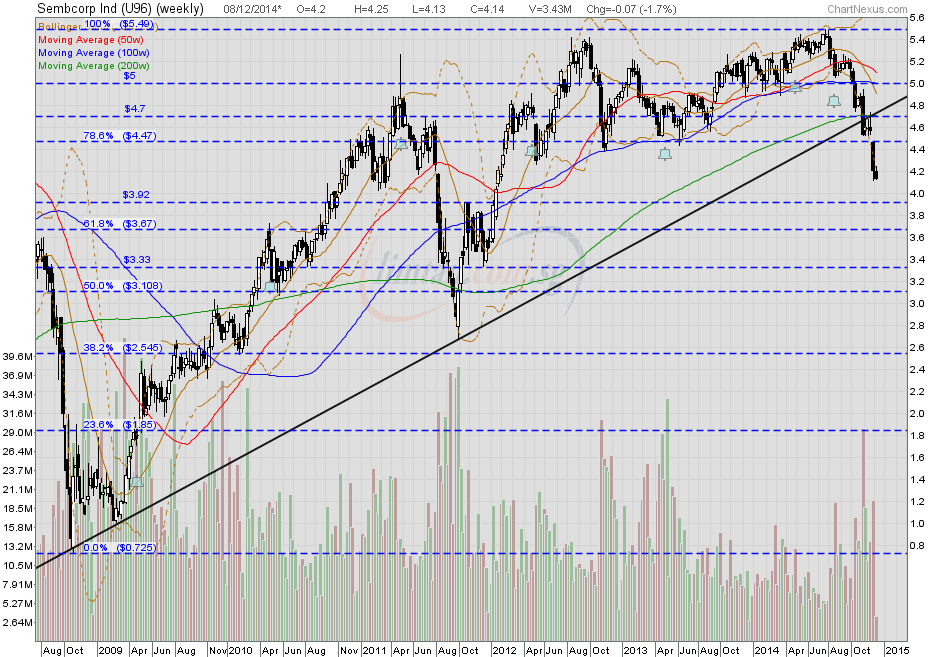

SembCorp Ind (weekly) dated 8 Dec 2014 DBS had peaked @ S$21.20 on 23 Jul 2015, it's now riding on sub-wave-iii of wave-v of A-wave of the corrective ABC-wave down.

DBS (weekly as at 7 Jan 2016) ~ Uptrend is broken, downward bias, interim TP S$11.20 SembCorp Ind (weekly) — Uptrend is broken, biased to the downside, TP S$3.33

SembCorp Ind (weekly) — Uptrend is broken, biased to the downside, TP S$3.33 Singapore loan growth may be stuck in the red after dropping to 16-year low

Singapore loan growth may be stuck in the red after dropping to 16-year low ~ 2 Feb 2016

Another monetary policy easing is unwarranted, says DBS ~ 1 Feb 2016

Broker's call: CIMB rated DBS as 'BUY' TP S$19.58 ~ 1 Feb 2016

Banks on the hook for bad energy loans ~ 1 Feb 2016

The week ahead: All eyes on DBS ~ 31 Jan 2016

Round 1 goes to the bears ~ 30 Jan 2016

DBS keeps 6.1% for the Philippines growth target for 2016 ~ 29 Jan 2016

Business outlook of services sector firms sinks to 4-year low in January ~ 29 Jan 2016

Here's why DBS is not stressing over its steadily shrinking trade book ~ 28 Jan 2016

Tepid reception to DBS Tier-2 bonds shows risk aversion18 Jan 2016

[SINGAPORE] Hopes that a spree of bank capital issuance would prop up the sluggish Singapore dollar bond market took a blow last week with the tepid reception to a Tier 2 offering from DBS Group. On paper, the offering was a perfect match for investors hungry for safe havens in a period of heightened volatility.

However, even Singapore's biggest banking group was not completely immune to weak global markets and had to settle for modest takings. DBS sold a S$250m 12-year non-call seven subordinated bond - its first Basel III-compliant Tier 2 - at a yield of 3.8 per cent last Wednesday. The pricing came in slightly higher than initial guidance of high 3 per cent, typically taken to indicate a target of 3.75 per cent.

The issue drew a book of S$300m from 52 accounts, prompting rival bankers to point out that the deal had difficulty attracting investors, despite the higher-than-expected yield.

"In current volatile markets, investors are just too averse to risk, and issuers looking to sell bonds must be prepared to temper their pricing and deal size expectations," said one head of debt origination.

That said, the 3.8 per cent yield translated into 110bp over Singapore dollar SOR, a rather tight spread for bonds that are subordinated and subject to regulatory writedown triggers.

DBS, aware of investors' jitters, had also targeted a modest size of S$200m to S$300m.

"It was a reasonable trade that achieved good pricing," said one debt syndicate banker, observing that the modest size reflected the current liquidity available in the market.

The episode suggests that foreign banks seeking to raise subordinated bank capital in Singapore may also have to adjust their expectations.

Among the names checking the market are banks that have raised T2 paper in the local market before, such as Australia and New Zealand Banking Group and ABN Amro, as well as those that have not, such as Commonwealth Bank of Australia and Societe Generale.

ANZ was said to be eyeing a deal in the latter half of last week, before Asian stocks tumbled once again on Thursday. ANZ sold its first Basel III T2 in Singapore last March with a S$500m 12-year non-call seven at 3.75 per cent, a size no other foreign bank had since been able to match. Investors said there was still liquidity in the market as there had been a lack of high-grade paper and they needed to put their funds to work.

They suggested the main obstacle to the foreign banks launching deals was pricing.

ABN AMRO had been indicating a spread of around 200bp over SOR the previous week for a 10 non-call five T2, but investors wanted 20bp more and pushed back.

The worsening market conditions last week would have raised investor expectations to 240bp and above for an ABN trade.

Some bankers are not expecting a wave of new T2 notes due to the market volatility, but others disagree, pointing to Singapore's proven appetite for bank capital and the relatively low funding costs set by benchmark issues from local banks.

"The issuers will just have to do the deals piecemeal rather than a single large issue," said a banker involved in one of the planned transactions.

"There is no place for ego in these choppy times."

Singapore Banks: Deteriorating ~ 24 Nov 2015

DBS is the pick of Singapore’s bank stocks ~ 12 Nov 2015

DBS China picked to test yuan payment system ~ 9 Oct 2015

DBS’ selloff is overdone: It’s time to buy ~ 22 Sep 2015

6 reasons why DBS is the top pick among banks ~ 7 Sep 2015

Analysts: Rates hike imminent; OCBC and DBS top picks ~ 27 July 2015

Delinquent loans are a sore spot for local banks ~ 6 July 2015

At what price would Benjamin Graham buy DBS? ~ 30 Dec 2014