Post by zuolun on Mar 27, 2015 10:37:49 GMT 7

Major Substantial Shareholder, Dayang up stake in Perdana to 29.88% or 222,853,980 shares ~ 20 Mar 2015

Perdana: Substantial Shareholder - All transactions

Malaysia Trade Policies (Rules and Regulations on Take-Overs and Mergers)

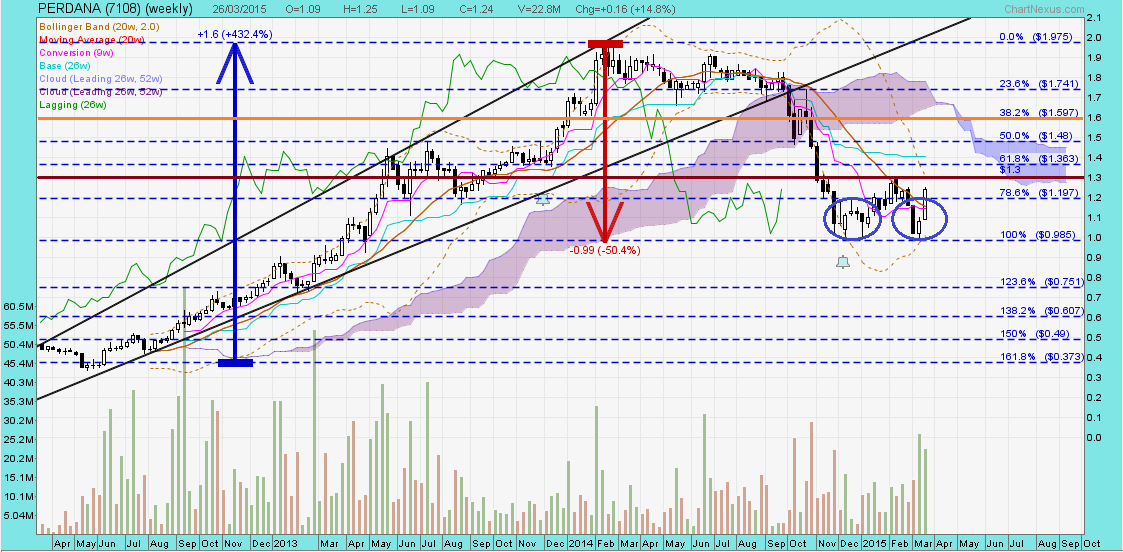

Perdana ~ Double Bottom formation, biased to the upside, TP RM1.60

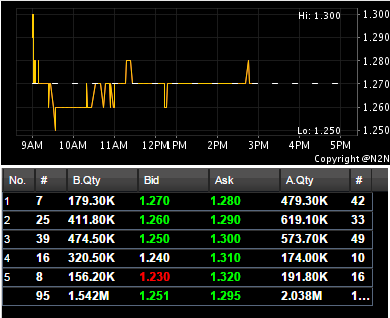

Perdana closed with a white marubozu @ RM1.24 (+0.04, +3.3%) with 4.6m shares done on 26 Mar 2015.

Immediate support @ RM1.19, immediate resistance @ RM1.30.

Perdana (weekly) ~ Double Bottom formation, biased to the upside, TP RM1.60

Perdana as at 19 July 2012

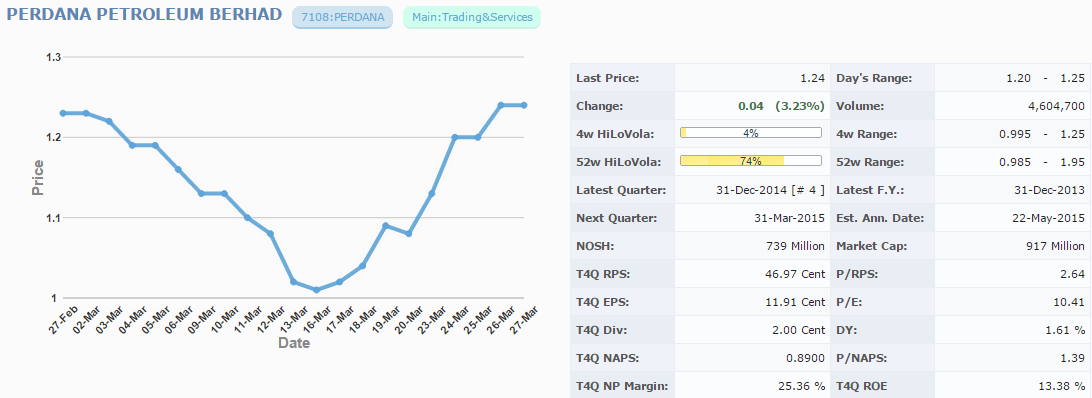

Perdana Petroleum (7108) Factsheet

Exercise of 970,800 Perdana-WA (7108WA) @ RM0.71 per share ~ 20 Mar 2015

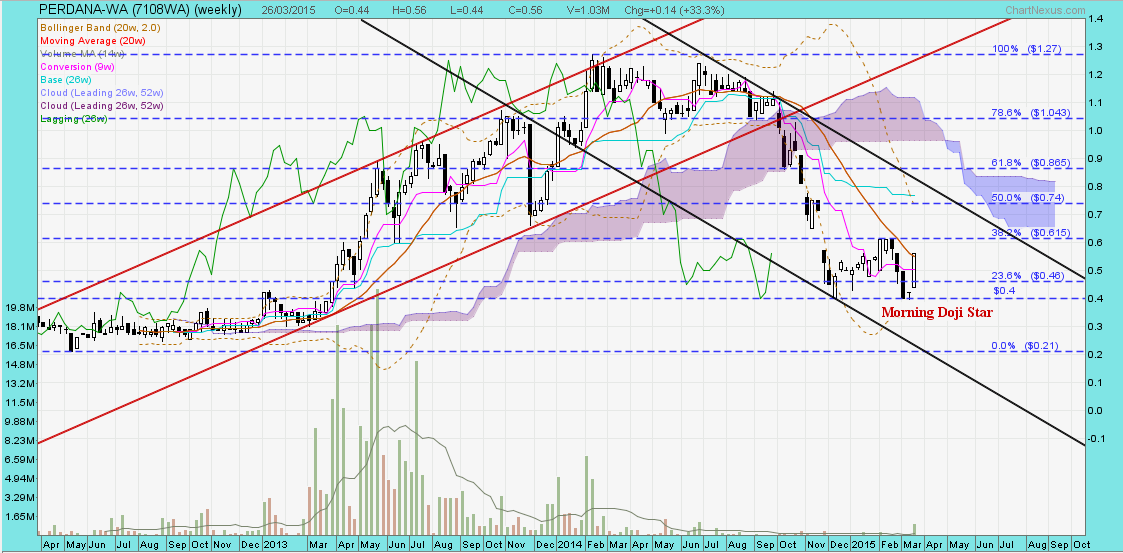

Perdana-WA (weekly) closed with a bullish morning doji star @ RM0.56 (+0.14, +33.3%) with 1.03m shares done on 26 Mar 2015.

As at 26 Mar 2015, Perdana-WA (7108WA) @ RM0.56 + Exercise price @ RM0.71 per share = RM1.27 per share.

CIMB rated Perdana Petroleum Add, TP RM1.61 - Let it GO?

27 Mar 2015

Armed with a fresh war chest, cash-rich Dayang raised its stake in Perdana to 29.9% last week, raising the possibility of a general offer (GO). Interestingly, we note that another major shareholder, Lembaga Tabung Haji (LTH), is likely to exit Perdana, which is no longer shariah-compliant. We continue to value the stock at 10.5x CY16 P/E, still at a 30% discount to the oil & gas big caps. Perdana remains an Add and our top oil & gas small-cap pick, with the potential GO and an expanding fleet as the potential re-rating catalysts.

What Happened

Perdana's share price has jumped 18% since 16 Mar, the day its major shareholder, Dayang, resumed purchasing Perdana shares after a hiatus of almost five months. Dayang bought 11.5m shares on 16-18 Mar, taking its stake to 29.9%. Earlier, on 12 Mar, Dayang completed a private placement of 52.1m shares at RM3.37/share, raising gross proceeds of RM176m that were earmarked for "working capital and/or potential investment project(s)".

What We Think

Dayang became Perdana's shareholder in Dec 2011 through a 10% private placement and has since increased its stake to the current level. The synergies between the two companies are in the area of brownfield services, which require workbarges and workboats. Perdana currently has five workbarges and a workboat deployed to Dayang on long-term charters. More than 70% of Perdana's vessels are on long-term charters (FY13: 65%).

To recap, Perdana ended FY14 with a record net profit of RM88m (+55% yoy), propelled by a higher average vessel utilisation rate of 91% (FY13: 80%). The company declared a full-year DPS of 2 sen, the first since FY09 after a boardroom tussle and a vessel glut that caused losses. The company has an order book of around RM1.1bn up to FY19, keeping its young fleet of 19 vessels, of which 17 are in operation, busy. The fleet's average age is 4.8 years.

Interestingly, Perdana's third largest shareholder, LTH, is likely to exit Perdana, which dropped off the Securities Commission's list of shariah-compliant securities in Nov 2014 and will stay out of the list in the May and Nov 2015 reviews. We understand that LTH's average cost is around RM1.80/share. At the current share price, LTH's stake is worth RM75m. Should Dayang acquire LTH's block entirely, a GO would be triggered.

What You Should Do

We advise investors to accumulate.

Perdana: Substantial Shareholder - All transactions

Malaysia Trade Policies (Rules and Regulations on Take-Overs and Mergers)

Perdana ~ Double Bottom formation, biased to the upside, TP RM1.60

Perdana closed with a white marubozu @ RM1.24 (+0.04, +3.3%) with 4.6m shares done on 26 Mar 2015.

Immediate support @ RM1.19, immediate resistance @ RM1.30.

Perdana (weekly) ~ Double Bottom formation, biased to the upside, TP RM1.60

Perdana as at 19 July 2012

Perdana Petroleum (7108) Factsheet

Exercise of 970,800 Perdana-WA (7108WA) @ RM0.71 per share ~ 20 Mar 2015

Perdana-WA (weekly) closed with a bullish morning doji star @ RM0.56 (+0.14, +33.3%) with 1.03m shares done on 26 Mar 2015.

As at 26 Mar 2015, Perdana-WA (7108WA) @ RM0.56 + Exercise price @ RM0.71 per share = RM1.27 per share.

CIMB rated Perdana Petroleum Add, TP RM1.61 - Let it GO?

27 Mar 2015

Armed with a fresh war chest, cash-rich Dayang raised its stake in Perdana to 29.9% last week, raising the possibility of a general offer (GO). Interestingly, we note that another major shareholder, Lembaga Tabung Haji (LTH), is likely to exit Perdana, which is no longer shariah-compliant. We continue to value the stock at 10.5x CY16 P/E, still at a 30% discount to the oil & gas big caps. Perdana remains an Add and our top oil & gas small-cap pick, with the potential GO and an expanding fleet as the potential re-rating catalysts.

What Happened

Perdana's share price has jumped 18% since 16 Mar, the day its major shareholder, Dayang, resumed purchasing Perdana shares after a hiatus of almost five months. Dayang bought 11.5m shares on 16-18 Mar, taking its stake to 29.9%. Earlier, on 12 Mar, Dayang completed a private placement of 52.1m shares at RM3.37/share, raising gross proceeds of RM176m that were earmarked for "working capital and/or potential investment project(s)".

What We Think

Dayang became Perdana's shareholder in Dec 2011 through a 10% private placement and has since increased its stake to the current level. The synergies between the two companies are in the area of brownfield services, which require workbarges and workboats. Perdana currently has five workbarges and a workboat deployed to Dayang on long-term charters. More than 70% of Perdana's vessels are on long-term charters (FY13: 65%).

To recap, Perdana ended FY14 with a record net profit of RM88m (+55% yoy), propelled by a higher average vessel utilisation rate of 91% (FY13: 80%). The company declared a full-year DPS of 2 sen, the first since FY09 after a boardroom tussle and a vessel glut that caused losses. The company has an order book of around RM1.1bn up to FY19, keeping its young fleet of 19 vessels, of which 17 are in operation, busy. The fleet's average age is 4.8 years.

Interestingly, Perdana's third largest shareholder, LTH, is likely to exit Perdana, which dropped off the Securities Commission's list of shariah-compliant securities in Nov 2014 and will stay out of the list in the May and Nov 2015 reviews. We understand that LTH's average cost is around RM1.80/share. At the current share price, LTH's stake is worth RM75m. Should Dayang acquire LTH's block entirely, a GO would be triggered.

What You Should Do

We advise investors to accumulate.