The bane of negative interest rates ~ 29 Feb 2016

Is Singapore headed for a recession? ~ 29 Feb 2016

Combined revenues of S'pore's top 1000 companies hit S$3t mark ~ 29 Feb 2016

Undesirable lending practices uncovered at some local banks: MAS ~ 29 Feb 2016

Singapore's 2015 tourism receipts dip 6.8% to $22b as business travel falters ~ 29 Feb 2016

Licensed moneylenders to get access to borrowers' data ~ 25 Feb 2016

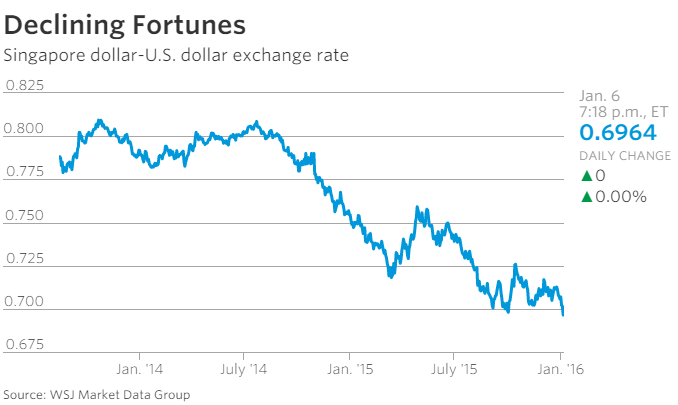

Will the MAS ease as exports tumble? ~ 18 Feb 2016

Likelihood of MAS easing monetary policy rising ~ 13 Feb 2016

Is the next financial crisis finally here? ~ 11 Feb 2016

Singapore REITs hit 5-year high in distribution yield amid market slump ~ 25 Feb 2016

A tweak to the inflation forecast, a debate over MAS's Sing dollar policy

A tweak to the inflation forecast, a debate over MAS's Sing dollar policy24 Feb 2016

The Monetary Authority of Singapore (MAS) on Tuesday lowered its 2016 headline inflation forecast, but kept its core inflation projection unchanged - leaving economists to grapple with what this will mean for April's monetary policy statement.

Some think the central bank is now tilting towards a weaker Singapore dollar policy; others believe no revision is on the cards; and then there are those who say it is too early to make a call.

Singapore's full-year headline inflation rate is now expected at -1 to 0 per cent - lower than the previous official forecast of -0.5 to 0.5 per cent.

In a joint statement, the MAS and the Ministry of Trade and Industry (MTI) said the lower inflation projection is due to the significant step-down in global oil prices in recent months, and the larger-than-expected decline in Certificate of Entitlement (COE) premiums at the start of the year.

However, the forecast for core inflation - which strips out the costs of accommodation and private road transport - remains unchanged at 0.5 to 1.5 per cent.

MAS and MTI said that this reflects the smaller weight of oil-related items and the exclusion of private road transport costs.

They added: "Core inflation is still expected to pick up gradually over the course of 2016, as the disinflationary effects of oil as well as budgetary and other one-off measures ease."

Their joint remarks came as data from the Department of Statistics showed that consumer prices continued to fall 0.6 per cent year-on-year in January - the 15th consecutive month of negative inflation.

MAS's decision to lower its headline inflation forecast while keeping its core inflation projection intact drew a range of views on its implications for monetary policy.

Economists such as HSBC's Joseph Incalcaterra and Credit Suisse's Michael Wan read it to mean that the central bank is in no rush to ease based on inflation.

Others, like Citi's Kit Wei Zheng and ANZ's Ng Weiwen interpret it as yet another sign of the rising possibility of a weaker Singapore dollar policy come April.

Said Citi's Mr Kit: "While the unchanged core inflation forecast suggests an April easing is not a foregone conclusion, MAS may not completely ignore headline disinflation if it interprets lower COE premiums as partly a symptom of underlying demand weakness.

"With the risk that growth has been weaker than MAS's October expectations, we suspect the hurdle to further policy easing may be closer to being cleared. Besides growth and inflation data, we would watch labour market developments, and the Budget on March 24." Meanwhile, Barclays's Leong Wai Ho told BT that his bank is now re-looking its stance on MAS's upcoming meeting. "It's under review, so we probably won't say anything at this stage ... But all indicators show that hurt levels are rising. I don't think it will be good for Q1."

At a 0.6 per cent decline, January's inflation rate was unchanged from December, and was exactly in line with market expectations.

Core inflation, however, remained in positive territory and edged up to 0.4 per cent in January from 0.3 per cent a month ago. This was mostly due to the smaller reduction in electricity tariffs as well as higher food and retail goods inflation, which more than offset the fall in services inflation. The biggest drag on overall inflation was accommodation cost, which declined by 3.1 per cent in January after December's 3 per cent fall.

This alone took away 0.71 percentage points from the headline inflation rate and reflects the persistently weak rental market, noted Mr Leong.

With the sharper fall in car prices amid weaker COE premiums, private road transport cost was 1.8 per cent lower - extending the 1.1 per cent decline the month before.

MAS and MTI said: "The cost of oil-related items fell at a slower rate of 3.2 per cent in January compared to the 7 per cent decline in the previous month, mainly due to a smaller drop in electricity tariffs, which reflected the low base in January last year."

But services, food and retail items inflation remained in positive territory, with food and retail climbing higher. Food inflation rose 1.7 per cent from 1.5 per cent in December; the overall cost of retail items was 0.6 per cent higher - mainly due to a faster pace of increase in clothing and footwear prices.

On the services front, inflation moderated to 0.5 per cent in January from 0.9 per cent a month earlier, mostly because of a slower pace of increase in education-services fees and holiday travel costs.

But the slowdown was not broad-based; healthcare services costs picked up as the disinflationary effects of enhanced medication subsidies introduced in January last year dissipated.

Looking ahead, MAS and MTI said global oil prices are expected to average lower for the whole of this year than last year.

On the domestic front, wages are expected to continue rising this year, although more moderately than last year.

They added: "The pass-through of wage costs to consumer prices may also remain tempered by the subdued economic growth environment."

OCBC economist Selena Ling said: "I think the road is still open (for MAS to ease) in April, but it's more like a wait-and-see story, given how quickly things evolve. I don't think (Tuesday's headline inflation downgrade) pre-sets them on a certain course."