|

|

Post by zuolun on Oct 2, 2014 11:17:38 GMT 7

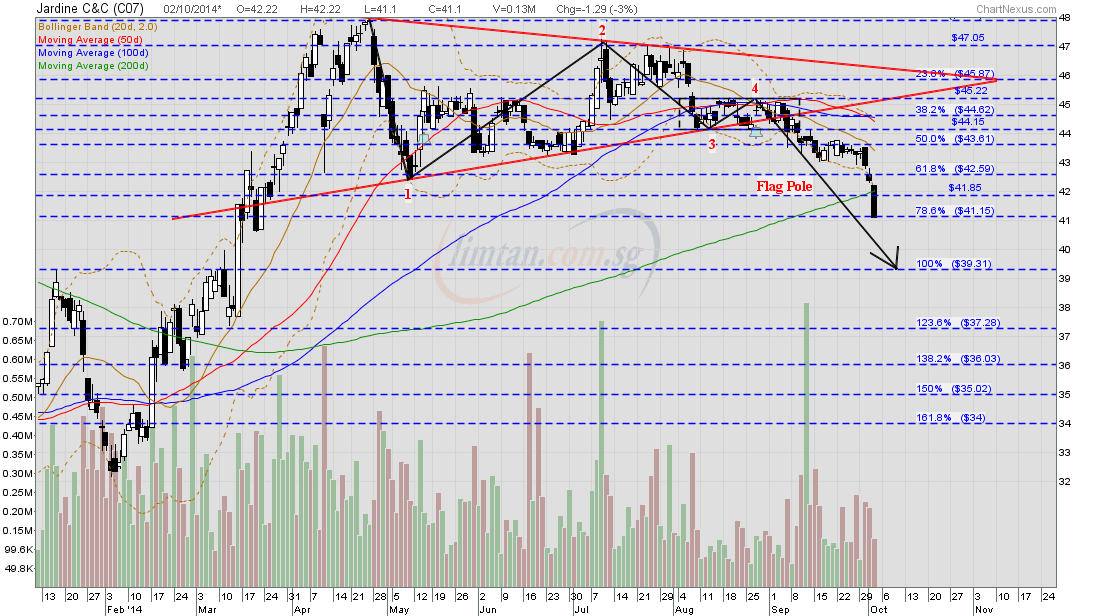

JC&C — Broke the 200d SMA convincingly, biased to the downside, interim TP S$39.31JC&C had a long black marubozu @ S$41.10 (-1.29, -3%) with 129 lots done on 2 Oct 2014 at 12.15 noon.

|

|

|

|

Post by zuolun on Oct 3, 2014 12:12:34 GMT 7

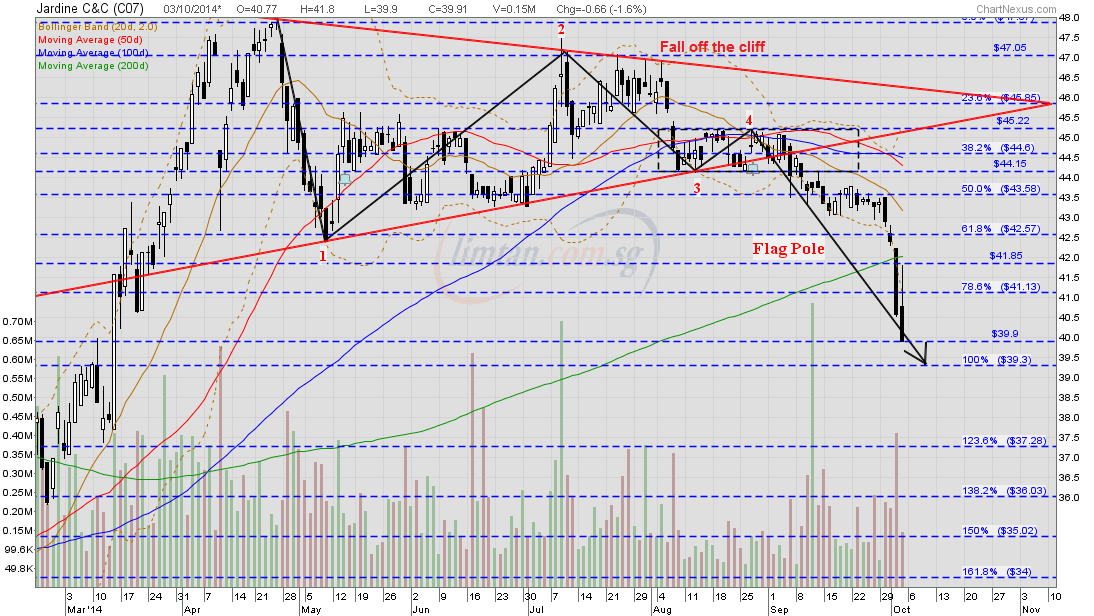

JC&C — Bearish symmetrical triangle breakout, Interim TP S$39.30, Next TP S$32.18JC&C had an inverted hammer @ S$39.91 (-0.66, -1.6%) with 145 lots done on 3 Oct 2014 at 1.10 pm. Immediate support @ S$37.28, immediate resistance @ S$41.85.

|

|

|

|

Post by zuolun on Nov 5, 2014 10:23:32 GMT 7

|

|

|

|

Post by zuolun on Mar 12, 2015 14:11:16 GMT 7

Jardine C&C traded @ S$40.68 (-0.34, -0.6%) with 141,200 shares done on 12 Mar 2015 at 3.05pm

DBSV downgraded Jardine C&C to HOLD TP S$44.95.

12 Mar 2015

Jardine Cycle & Carriage: HOLD (Downgrade from BUY); S$41.02; JCNC SP

Sedate earnings outlook

Price Target :SOPS$44.95 (Prev S$49.88)

By: Paul YONG CFA+65 6682 3712; paulyong@dbs.com

• Cut FY15/16 earnings forecasts for Astra Intl by 15%/17%;recommendation likewise downgraded to HOLD

• A weaker IDR vs USD outlook further justifies our JC&C FY15/16 forecasts being cut by 27%/35%

• Dividend payout likely to remain tepid; with total dividends cut to US 85cts for FY14 from US 108cts

• Downgrade to HOLD with S$44.95 target price

Weak rupiah and Astra performance hit 2014 numbers. JC&C's FY14 results showed an 11% y-o-y decline in underlying profit to US$793m, although Astra only registered a 3% y-o-y decline in Rupiah terms - due to the Rupiah weakening against the US$ by 15% over the year. Higher contribution from other interests rose 40% y-o-y to US$82m, marginally offsetting the weaker Astra performance.

Astra's profit estimates slashed. Trimming 4W sales estimates and margins for Astra amidst a competitive environment with weak demand, we have lowered our FY15/16 earnings forecasts for Astra by 15%/17%. Meanwhile, as the US$ is expected to strengthen against the Rupiah to 13660 by end-2015 and 13870 by 1Q16, we have cut our FY15/16 US$ earnings forecasts for JC&C by 27%/35%. We now project JC&C's earnings (in US$ terms) to decline 7% y-o-y to US$759m and grow a modest 2% y-o-y to US$775m in FY16.

Downgrade to HOLD. Our target price has been lowered to S$44.95, mainly due to our reduced target price for Astra Intl (from Rp8,600 to Rp8,000), and a slightly weaker IDR vs SGD expectation. With FY14 total dividends cut to US 85cts from US 108cts the year before on weaker earnings, the dividend yield on JC&C is also a mere pedestrian 2.9%. At 14x PE, it is trading around +1SD from its mean of 10.1x since 2007.

|

|

|

|

Post by zuolun on Jun 12, 2015 14:54:27 GMT 7

New liquidity requirement of 0.1% of issued shares, possibility that JC&C may have to be removed from the STI ~ 2 Jun 2015 JC&C — Bearish descending triangle breakout, TP S$31.40JC&C had a spinning top and traded @ S$36.80 (+0.05, +0.1%) with 86,500 shares done on 12 Jun 2015 at 0400 hrs. Immediate support @ S$36.00, immediate resistance @ S$37.60.  JC&C — Bearish symmetrical triangle breakout, Interim TP S$39.30, Next TP S$32.18JC&C had an inverted hammer @ S$39.91 (-0.66, -1.6%) with 145 lots done on 3 Oct 2014 at 1.10 pm. Immediate support @ S$37.28, immediate resistance @ S$41.85.

|

|

|

|

Post by zuolun on Jun 16, 2015 7:53:11 GMT 7

|

|

|

|

Post by zuolun on Jun 20, 2015 11:13:32 GMT 7

|

|

|

|

Post by zuolun on Jun 26, 2015 17:50:09 GMT 7

|

|

[/b]

[/b]