|

|

Post by zuolun on Jun 1, 2015 16:03:37 GMT 7

The Amtrak Economy! | Andy Hoffman ~ 28 May 2015

|

|

|

|

Post by zuolun on Aug 10, 2015 11:04:11 GMT 7

Will US stock indexes and the dollar finally break this week? ~ 7 Aug 2015

|

|

|

|

Post by zuolun on Aug 25, 2015 9:41:52 GMT 7

|

|

|

|

Post by newbiee on Aug 26, 2015 16:14:00 GMT 7

|

|

|

|

Post by newbiee on Aug 26, 2015 16:15:32 GMT 7

Hi Bro Zuolun,

Can you draw up the S&P500 Elliot Wave. What's your view on S&P?

Thanks Ya.

|

|

|

|

Post by zuolun on Aug 26, 2015 16:29:09 GMT 7

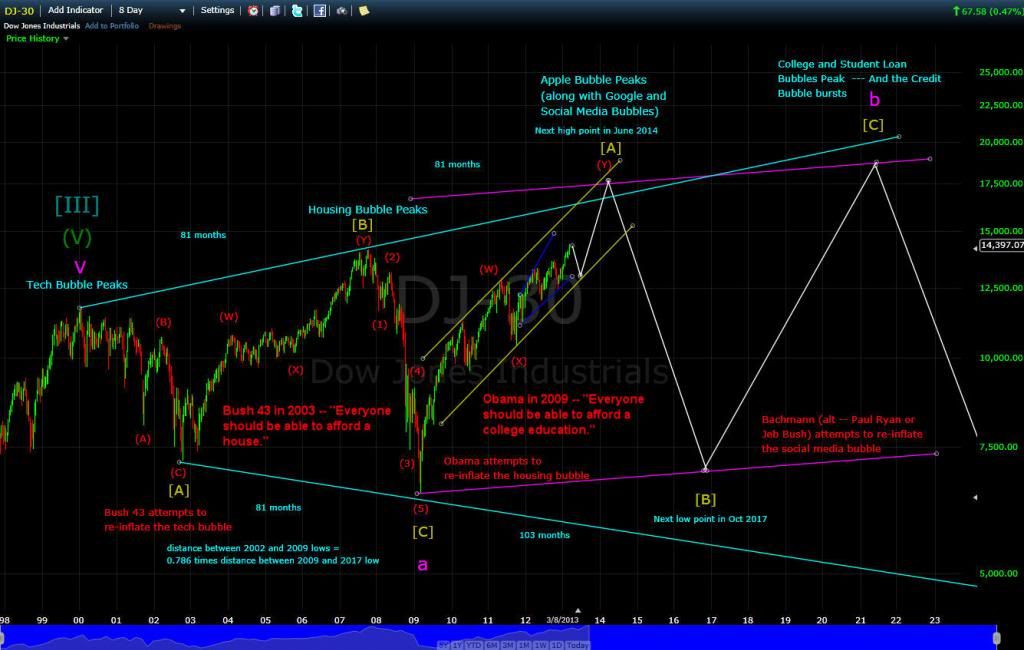

Hi Bro Zuolun, Can you draw up the S&P500 Elliot Wave. What's your view on S&P? Thanks Ya. , I did not renew my subscription for the US stock market charting program. My current FOC version cannot draw longterm charts; for the Elliot Wave pattern on the S&P500, refer to the thread here. |

|

|

|

Post by newbiee on Aug 26, 2015 17:03:34 GMT 7

Thanks for your prompt reply but i can't open, it prompt me error.....  |

|

|

|

Post by zuolun on Aug 26, 2015 17:15:57 GMT 7

Thanks for your prompt reply but i can't open, it prompt me error..... I've double checked that the link here is ok...something is wrong with you PC.  |

|

|

|

Post by zuolun on Aug 27, 2015 11:40:56 GMT 7

|

|

|

|

Post by pain on Aug 28, 2015 14:30:53 GMT 7

My heart is weak but I have a strong stomach.  Thanks for your prompt reply but i can't open, it prompt me error..... I've double checked that the link here is ok...something is wrong with you PC. |

|

|

|

Post by zuolun on Sept 19, 2015 8:58:59 GMT 7

|

|

|

|

Post by zuolun on Sept 29, 2015 8:44:13 GMT 7

|

|

|

|

Post by zuolun on Oct 4, 2015 12:23:53 GMT 7

Peter Schiff: We're in deep economic shit! ~ 3 Oct 2015 It's 2006 All Over Again ~ 30 Sep 2015 Global monetary system: Thrills and spills ~ 3 Oct 2015 Asia’s ‘recession barometer’ is flashing ~ 3 Oct 2015 One world, one bank, one currency ~ 1 Oct 2015 Global economy loses steam as Chinese, European factories falter ~ 1 Oct 2015 The credit bubble, the bears and the central bankersBy Gillian Tett 1 Oct 2015 When officials at the International Monetary Fund and World Bank first decided to hold this year’s annual meeting in Peru, some hoped that the location would offer a celebratory backdrop. For after the 2008 western financial crisis, it initially seemed as if emerging markets — including those in Latin America — had seized the baton of global growth. After all, they were not involved in the craziness of the credit bubble that led up to the crisis, with all its subprime mortgage sins. No longer. Next week, when the IMF and World Bank meet in Lima, officials will certainly wail about the feeble pace of developed world growth. What is really unnerving policymakers, however, is not the west but the state of emerging markets. Growth is slowing everywhere from China to Peru. In addition, it is becoming clear that emerging markets have become caught up in a new credit bubble. And the consequences — like those of the western credit bubble of the previous decade — could be deeply destabilising for the global economy and unpleasant for investors. This is not least because the way that financial flows operate today in, say, Shanghai is almost as mysterious for investors as subprime mortgages were in California a decade ago, and just as dangerously contagious. One way to get a sense of how risks are changing is to look at what has happened to emerging market corporate debt. A decade ago, this seemed to be running at fairly modest levels, at least compared with parts of the western world. But as the IMF notes in its latest financial stability report, between 2004 and 2014 emerging market corporate debt increased from $4,000bn to $18,000bn, with much of the growth occurring after 2008. This gross number conceals big variations. Though corporate borrowing has recently surged in China, Turkey, Chile, Brazil, India and Mexico, it has declined in South Africa, Hungary and Bulgaria. But measured overall, the IMF calculates that emerging market liabilities are now twice the size of their equity; a mere four years ago, they were at par. It is a striking swing that raises questions about whether emerging market companies can service this debt if (or when) central bankers in the developed world — notably the US Federal Reserve — start to raise interest rates. But there is a second way to frame the problem, which is to look at emerging markets debt not in isolation but in the global context of “money”. After all, as Matt King, an analyst at Citi, notes it is important to remember that there are two ways that “money” — in the widest sense — can be created. The first is through central bank action; quantitative easing has pumped trillions of dollars into the global system. The second part of the equation occurs when private-sector banks and markets recycle those central bank funds — and, most crucially, amplify these, sometimes on a massive scale. For the past two years it was QE, the first part of the equation, that grabbed investors’ attention; the second part is often ignored because the data are poor. However, Citi has tried to calculate global private-sector money creation and reached a startling conclusion: three-quarters of all global private money creation in the past five years has occurred in emerging markets. More specifically, since 2000 $8,000bn of flows have gone into emerging markets — and this has generated $5,000bn of private emerging market credit each year. This raises a crucial question: what happens when this process of emerging market private money creation slows or goes into reverse? Some policymakers hope any shock could be contained by more money creation on the part of western central banks — a bit more QE might calm markets, or so the argument goes. But Mr King of Citi doubts this will work: the emerging market bubble is so big that it is far from clear central banks could plug the gap if (or when) this money creation slows down; the world is reaching a point of “credit exhaustion”. If this analysis is even partly correct (and I believe it is), the implications are alarming. That helps explain why markets have had such a nervy air recently, and why some of the savviest hedge fund managers, such as John Burbank of San Francisco-based Passport Capital, are now emerging markets bears. It also sheds light on why the IMF is so worried about what happens when US rates rise. But until then, perhaps the real message is that it is no longer enough for investors to just watch the Fed. All eyes should now be fixed on emerging markets, too; starting with what does (or does not) happen next week in Peru.

|

|

|

|

Post by zuolun on Oct 13, 2015 12:42:18 GMT 7

|

|