|

|

SMRT

Dec 27, 2013 9:38:18 GMT 7

odie likes this

Post by zuolun on Dec 27, 2013 9:38:18 GMT 7

|

|

|

|

Post by oldman on Dec 30, 2013 8:02:44 GMT 7

It is my nature to look at stocks that have fallen from grace. Numbers here are still not attractive enough. Not easy for them to increase their fare structure sufficiently when the public perception is that the trains and buses are still crowded and reliability remains an issue. Likely that capital expenditure will still need to be increased over the years to resolve the reliability issue. I don't see any tipping point apart from the gov taking back full control of the coy. Even then, I doubt the premium will be much. Hence, rather stay on the sidelines. At $1.15, SMRT is capitalised at $1.75 bil. Half year profits is just $30.6 mil. Pity those who invested in SMRT based on dividend yields as in FY2012, the total dividends was 7.45cts per share. With the interim dividend cut from 1.5cts to 1ct, the total dividend for FY2014 is now more likely to be 2cts. Dividends should always be seen as a subset of profits. If profits cannot be maintained, dividends too are unlikely to be maintained. Also, for me, I much prefer investing in companies that reduce its debt burden first before paying dividends. Zuolun, I agree that if it drops back to 60cts, I may take a second look.  Looking at the HY results ended 30 Sept 2013: Rev: $581 mil compared to $556 mil Profit: $30.6 mil compared to $69.8 mil PPE of $1.5 bil Cash of $173 mil compared to $546 mil (payment of $392.7 mil for 17 trains) Loans of $626 mil compared to $609 mil Trade payables of $272 mil compared to $577 mil ( payment of $392.7 mil for 17 trains) Interest on loans: $16.3 mil Dividend of 1ct compared to 1.5cts |

|

|

|

Post by zuolun on Dec 30, 2013 12:02:45 GMT 7

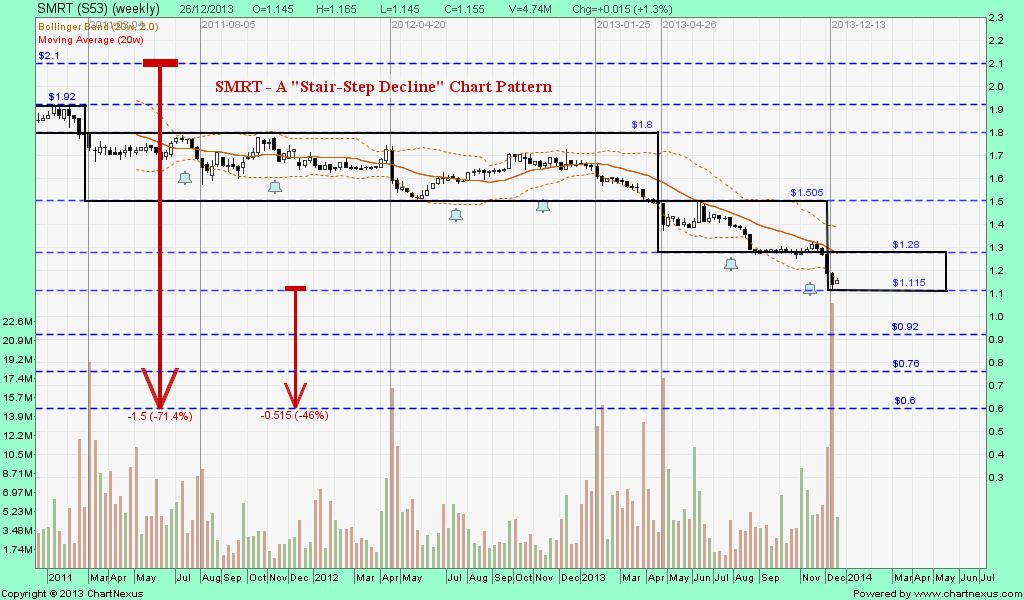

SMRT — The Elliott Wave Chart Pattern SMRT — The Elliott Wave Chart Pattern |

|

|

|

Post by zuolun on Dec 30, 2013 13:08:34 GMT 7

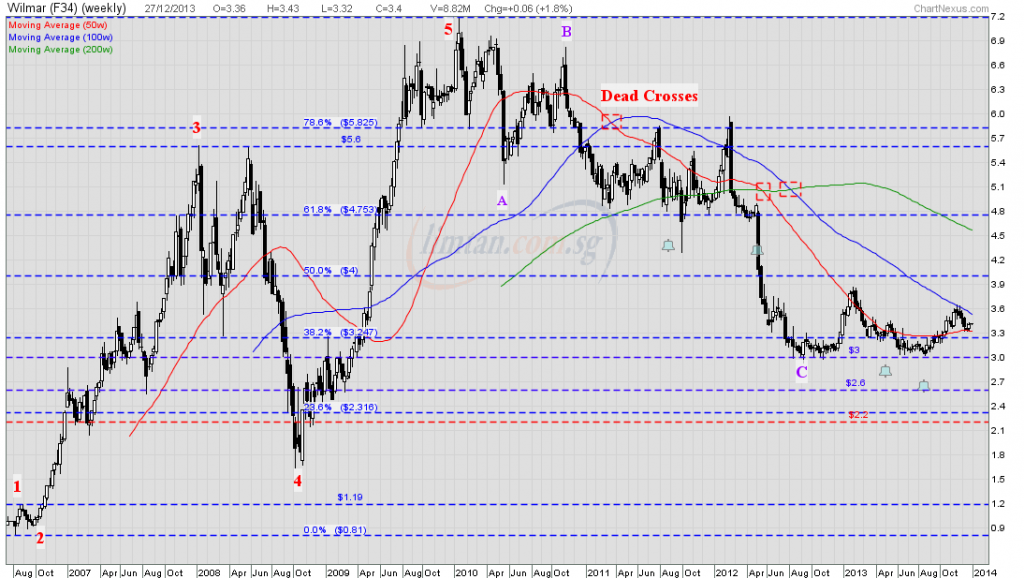

It is my nature to look at stocks that have fallen from grace. Numbers here are still not attractive enough. Not easy for them to increase their fare structure sufficiently when the public perception is that the trains and buses are still crowded and reliability remains an issue. Likely that capital expenditure will still need to be increased over the years to resolve the reliability issue. I don't see any tipping point apart from the gov taking back full control of the coy. Even then, I doubt the premium will be much. Hence, rather stay on the sidelines. At $1.15, SMRT is capitalised at $1.75 bil. Half year profits is just $30.6 mil. Pity those who invested in SMRT based on dividend yields as in FY2012, the total dividends was 7.45cts per share. With the interim dividend cut from 1.5cts to 1ct, the total dividend for FY2014 is now more likely to be 2cts. Dividends should always be seen as a subset of profits. If profits cannot be maintained, dividends too are unlikely to be maintained. Also, for me, I much prefer investing in companies that reduce its debt burden first before paying dividends. Zuolun, I agree that if it drops back to 60cts, I may take a second look. Looking at the HY results ended 30 Sept 2013: Rev: $581 mil compared to $556 mil Profit: $30.6 mil compared to $69.8 mil PPE of $1.5 bil Cash of $173 mil compared to $546 mil (payment of $392.7 mil for 17 trains) Loans of $626 mil compared to $609 mil Trade payables of $272 mil compared to $577 mil ( payment of $392.7 mil for 17 trains) Interest on loans: $16.3 mil Dividend of 1ct compared to 1.5cts oldman, Thanks for your invaluable FA input on SMRT. FA + TA = FATA = 发达 = prosper  Both SMRT and Wilmar chart patterns show extremely bearish longterm sustainable downtrend. As their share prices have been trading below all the 3 dead crosses; SMRT's TP S$0.60 and Wilmar's TP S$2.20 are interim target projections. Wilmar Vs SMRT |

|

|

|

SMRT

Dec 30, 2013 13:21:54 GMT 7

odie likes this

Post by oldman on Dec 30, 2013 13:21:54 GMT 7

I like your FA + TA = FATA !

Maybe too much TA = TA TA .... bye...

Too much FA = FAt ..... still good... ha ha.

|

|

|

|

Post by zuolun on Dec 30, 2013 16:26:09 GMT 7

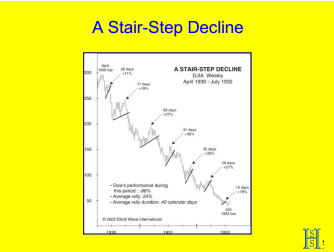

I like your FA + TA = FATA ! Maybe too much TA = TA TA .... bye... Too much FA = FAt ..... still good... ha ha. oldman, If you understand Cantonese; the chartist cites an example of the Rounding Bottom on Gold's yearly chart, which took many years to break-up of the "bowl". The Rounding Tops of Wilmar and SMRT move in inverse direction, which will also take many years to break-down of the inverse "bowl" or "mushroom head". Wilmar and SMRT's yearly chart clearly show a perfect Rounding Top = MOD (Mushroom Of Death). This type of "mushroom head" chart pattern has unique characteristics, i.e. the extremely strong longterm downtrend is sustainable. As both stocks already had their last burst of fire, it would be an uphill task for longterm investors to defy Newton's Law of Gravity, in the long run. |

|

|

|

Post by me200 on Jan 12, 2014 9:31:53 GMT 7

|

|

|

|

Post by me200 on Jan 16, 2014 18:28:45 GMT 7

|

|

|

|

SMRT

Jan 16, 2014 21:25:29 GMT 7

Post by candy188 on Jan 16, 2014 21:25:29 GMT 7

Hi me200, Just curious, how did you derive the "estimated gain of >$50m in train and bus service"?  Would that constitute a buy for SMRT now?  |

|

|

|

Post by stockpicker on Jan 17, 2014 6:02:46 GMT 7

If trains going up in price can improve the service, I would rather go for it. Our MRT train services are not as fast as before after they have put more trains on the track to shorten train waiting time. The journey from Jurong East to Changi Airport used to take about 50 minutes, now would easily take 1 hour 15 minutes and this is during off-peak hours.

In this video, this guy was comparing our train to those in Hong Kong

One thing I cannot help but notice that when we put up cctv cameras, we put up tons of them. My brother-in-law who worked in a Malaysian bank said the SMRT's cctv system is more elaborate than those in the bank's vault. On the other hand, there is only one old and small TV screen in every platform to tell train arrival. One would always have to bring a binocular to tell the time.

|

|

|

|

Post by candy188 on Jan 17, 2014 9:41:10 GMT 7

Extending FREE travel for children below 7 years old on public transport should have been implemented in Singapore long ago.  By tying the public transport fare to height limit of 0.9m is ridiculous as those who have outgrown at an earlier age are at a disadvantageous position.  Children up to 0.9m in height and accompanied by a fare-paying commuter may travel free. ===> However, pre-schoolers ABOVE 0.9m, BELOW 7 years old and not in Primary School may apply for a Child Concession card. www.smrt.com.sg/RiderGuide/Tickets/AdultStoredValueConcessionCards.aspx My girl was already 0.9m when she was approaching 3 years old (she is 1.15m now), so are the kids who are well fed nowadays . My girl was already 0.9m when she was approaching 3 years old (she is 1.15m now), so are the kids who are well fed nowadays .

Contrast this to a more acceptable height limit in China subway: Contrast this to a more acceptable height limit in China subway:

====> Children with the height Under 120cm can enjoy FREE rail travel and don't need to pay to travel by the train.www.chinatrainguide.com/beijing-railway-station/Kids Travel FREE on London Transport

London's public transport system is a great option for families, as children travel free or at discounted fares in most cases.  Children aged five to 10 can Travel FREE at any time by Tube, DLR and London Overground as long as they travel with an adult who has a valid ticket (up to four children can travel free with one adult) Children aged five to 10 can Travel FREE at any time by Tube, DLR and London Overground as long as they travel with an adult who has a valid ticket (up to four children can travel free with one adult) or have a 5-10 Zip Oyster photocard. They can travel without a photocard and unaccompanied on trams and buses. www.visitlondon.com/traveller-information/getting-around-london/kids-travel-free-on-london-transportPublic transport fare review: Public Transport Council announces fare increase of 4 to 6 centsTan Dawn Wei | The Straits Times | Thursday, Jan 16, 2014  Ensuring Fare Affordability Ensuring Fare Affordability

The PTC, in deciding on the 3.2 per cent fare increase for the 2013 Fare Exercise, noted that this is significantly lower than the 4 per cent-5 per cent wage increase in 2013 , and hence is keeping to the objective of ensuring that fares would remain generally affordable for commuters. Helping Commuters with Fare Concessions

The PTC decided to implement the following concession enhancements from April 6, 2014 to mitigate the impact of the fare increase on commuters: i. Free travel for children Below 7 years of age , before they enter primary school;

ride.asiaone.com/news/general/story/public-transport-fare-review-public-transport-council-announces-fare-increase-32?page=0%2C1

|

|

|

|

SMRT

Jan 17, 2014 10:12:40 GMT 7

Post by zuolun on Jan 17, 2014 10:12:40 GMT 7

Check out pictures of the disruption sent by some on the ground:Walking beside the railway track走在铁路旁 — 蔡幸娟

走過鐵路旁 我背著吉他 蘆花低頭笑呀 青蛙抬頭望 一句一句和呀

一聲一聲唱 蝸牛慢吞吞呀 漫步夕陽下

走在鐵路旁 我背著吉他 老牛對我望呀 和風來作伴 一步一步走呀

一聲一聲唱炊煙多瀟灑呀 陪我走回家

走過鐵路旁 我彈著吉他 蘆花低頭笑呀 青蛙抬頭望 一句一句和呀

一聲一聲唱 蝸牛慢吞吞呀 漫步夕陽下

走在鐵路旁 我背著吉他 老牛對我望呀 和風來作伴一步一步走呀

一聲一聲唱 炊煙多瀟灑呀 陪我走回家

走在鐵路旁 我彈著吉他 老牛對我望呀 和風來作伴 一步一步走呀

一聲一聲唱 炊煙多瀟灑呀 陪我走回家

炊煙多瀟灑呀 陪我走回家 炊煙多瀟灑呀 陪我走回家

|

|

|

|

SMRT

Jan 17, 2014 13:12:27 GMT 7

Post by candy188 on Jan 17, 2014 13:12:27 GMT 7

Hi Oldman, appreciate further guidance on my analysis.

Personally, I think SMRT possess higher upside potential from last traded price of $1.19, considering the drastic slide from historical high of $2.31 in July 2010.

Whereas, the last historical high of ComfortDelgro was $2.38 in April 2007, this may suggest little upside potential from last traded price of $1.945.In terms of FA, both transport companies possess strong underlying business fundamentals, except that the PE of SMRT is higher than ComfortDelgroComfortDelgro - ROE of 12.4%, PE of 17, Dividend yield of 3.2%, Debt to Equity of 0.35, Total cash of $694.6 million for year 2013

SMRT - ROE of 10.8%, PE of 21.7, Dividend yield of 2.1%, Debt to Equity of 0.79, total cash of $546.3 million for year 2013

Land Transport Sector: Fare increase of 3.2% for buses and trains Land Transport Sector: Fare increase of 3.2% for buses and trains

OCBC Research, 17 Jan 2014Singapore’s Public Transport Council (PTC) announced last evening that it has granted an overall fare adjustment of 3.2%, which will come into effect on 6 Apr 2014. Although this is lower than the combined 2012 and 2013 fare caps of 6.6%, but the 3.4% balance will be rolled over to 2015 for consideration of a future fare adjustment. This increase falls within our expectations, as we had highlighted in our Transport Sector Strategy report (dated 21 Nov 2013) that we expected a positive fare adjustment of around 3-3.5%. The PTC estimates that the net increase in revenue for SBS Transit and SMRT are approximately S$28.8m and S$13.2m a year, respectively, after taking into account both public transport operators’ (PTO) contribution to the Public Transport Fund (PTF). We believe this low single-digit fare increase will result in a positive boost to the PTOs’ earnings as the bulk of this net increment (after PTF contribution) will flow down to their profit before tax since their cost base remains similar and ridership is unlikely to be impacted. We keep our estimates intact for now as this fare adjustment exercise came in within our expectations.  Our preferred pick in the sector is ComfortDelgro [BUY; FV: S$2.20] over SMRT [HOLD; FV: S$1.30] due to the former’s better growth potential both locally and abroad, and less uncertainties over its opex outlook. Our preferred pick in the sector is ComfortDelgro [BUY; FV: S$2.20] over SMRT [HOLD; FV: S$1.30] due to the former’s better growth potential both locally and abroad, and less uncertainties over its opex outlook. (Wong Teck Ching Andy)

|

|

|

|

Post by oldman on Jan 17, 2014 15:31:17 GMT 7

Candy188, fundamental investors like me will only look at the fundamentals of the company. We do not consider the historical highs in our fundamental analysis. For me, I use technical charting to determine entry and exit points. After I have bought a share, I use the historical highs to help me determine my sell price. Similarly, I use the historical lows to pick up shares. But historical highs and lows are not used in my fundamental analysis. A struggling infrastructure company like SMRT needs lots of capital expenditure to put the things right. This is likely to take years to sort out and may drain lots of money. I don't think this is the right time to even look at its fundamentals. I rather look for a more stable company with stable profits. Of course, if you are a TA practitioner, you may be tempted to play the rebound..... Hi Oldman, appreciate further guidance on my analysis.

Personally, I think SMRT possess higher upside potential from last traded price of $1.19, considering the drastic slide from historical high of $2.31 in July 2010.

Whereas, the last historical high of ComfortDelgro was $2.38 in April 2007, this may suggest little upside potential from last traded price of $1.945.In terms of FA, both transport companies possess strong underlying business fundamentals, except that the PE of SMRT is higher than ComfortDelgroComfortDelgro - ROE of 12.4%, PE of 17, Dividend yield of 3.2%, Debt to Equity of 0.35, Total cash of $694.6 million for year 2013

SMRT - ROE of 10.8%, PE of 21.7, Dividend yield of 2.1%, Debt to Equity of 0.79, total cash of $546.3 million for year 2013

|

|

|

|

SMRT

Jan 17, 2014 15:56:55 GMT 7

oldman likes this

Post by candy188 on Jan 17, 2014 15:56:55 GMT 7

Hi Oldman, Thank you for your generous sharing on how you utilise historical highs and and lows to gauge the entry and exit points.  Candy188, fundamental investors like me will Only Look at the FUNDAMENTALS of the company.

We do not consider the historical highs in our fundamental analysis. For me, I use technical charting to determine entry and exit points.

After I have bought a share,

(1) I use the historical HIGHS to help me determine my SELL price.  (2) Similarly, I use the historical LOWS to Pick up shares. (2) Similarly, I use the historical LOWS to Pick up shares.

But historical highs and lows are NOT Used in my fundamental analysis. ==> A struggling infrastructure company like SMRT needs lots of capital expenditure to put the things right. This is likely to take years to sort out and may drain lots of money. I don't think this is the right time to even look at its fundamentals. I rather look for a more stable company with stable profits. Of course, if you are a TA practitioner, you may be tempted to play the rebound..... Hi Oldman, appreciate further guidance on my analysis.

Personally, I think SMRT possess higher upside potential from last traded price of $1.19, considering the drastic slide from historical high of $2.31 in July 2010.

Whereas, the last historical high of ComfortDelgro was $2.38 in April 2007, this may suggest little upside potential from last traded price of $1.945.In terms of FA, both transport companies possess strong underlying business fundamentals, except that the PE of SMRT is higher than ComfortDelgroComfortDelgro - ROE of 12.4%, PE of 17, Dividend yield of 3.2%, Debt to Equity of 0.35, Total cash of $694.6 million for year 2013

SMRT - ROE of 10.8%, PE of 21.7, Dividend yield of 2.1%, Debt to Equity of 0.79, total cash of $546.3 million for year 2013

|

|

.....

.....