|

|

Post by zuolun on Jun 23, 2014 9:32:13 GMT 7

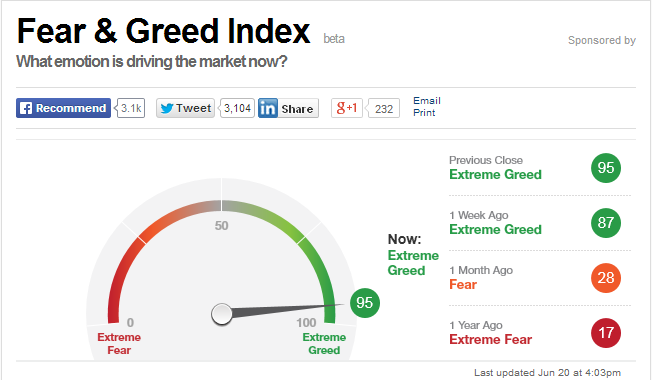

Zuolun, don't get me wrong. While partying, I am not shy to take profits along the way.  oldman, Stock prices already hit the Extreme Greed or near 100, now is the ripe time for a steep correction.  The STI moves in lockstep with the Fear & Greed Index:1. When the Fear & Greed Index was @ 91 or Extreme Greed on 17 May 2013; the STI had a steep correction starting from 23 May 2013. 2. When the Fear & Greed Index was @ 19 or Extreme Fear on 27 Aug 2013; the STI had a dead cat bounce starting from 29 Aug 2013.   |

|

|

|

SGX

Jul 12, 2014 19:58:42 GMT 7

oldman likes this

Post by zuolun on Jul 12, 2014 19:58:42 GMT 7

SGX says securities trading extends fall in June — 3 July 2014 Singapore Exchange (SGX) reported today that for the month of June, the total value of securities traded was $20.5 billion. This is a 37% drop year-on-year and down 12% month-on-month. ETF turnover was down 57% year-on-year at S$2.3 billion and lower 3% month-on-month. Bond listings increased to a total of 45 new bonds, raising about $20.8 billion, which is more than a 200% increase as compared to a year ago and about 23% up month-on-month. The biggest bond listing was PT Pertamina (Persero)’s US$1.5 billion 30-year bond. Foreign issuers account for 76% and foreign currency accounts for 82% of new listings. Outstanding bonds listed on SGX are 1,742, which is 19% higher year-on-year and 2% up month-on-month. Derivatives volume was 8.6 million contracts, down 20% year-on-year but a 6% increase month-on-month. Total open interest as at end of June was approximately 3.2 million contracts, close to the same volume as the year before, but down 9% month-on-month. Derivatives daily average volume (DDAV) was down 25% to 419,428 contracts year-on-year, but up 5% month-on-month. Singapore exchange struggles to grow as rivals thrive — 30 Apr 2014 SGX — Symmetrical Triangle FormationCrucial support @ S$6.70, strong resistance @ S$7.19, the long-term horizontal support-turned-resistance.  SGX (weekly) — Descending Triangle Formation SGX (weekly) — Descending Triangle Formation SGX (Mar 2008 to Oct 2013) — Longterm horizontal support @ S$7.19 SGX (Mar 2008 to Oct 2013) — Longterm horizontal support @ S$7.19

|

|

|

|

SGX

Jul 17, 2014 9:44:20 GMT 7

oldman likes this

Post by zuolun on Jul 17, 2014 9:44:20 GMT 7

|

|

|

|

SGX

Aug 2, 2014 6:55:58 GMT 7

oldman likes this

Post by zuolun on Aug 2, 2014 6:55:58 GMT 7

|

|

|

|

Post by zuolun on Aug 3, 2014 6:55:03 GMT 7

Big changes afoot for SGX share trading2 Aug 2014 SINGAPORE — A minimum price of 20 cents for mainboard counters, reduced lot sizes and the end of contra trades are some of the major changes that will take place over the next two years in the way shares are traded on the Singapore Exchange. The wide range of initiatives was laid out by the Monetary Authority of Singapore (MAS) and Singapore Exchange (SGX) yesterday, following a three-month public consultation process that ended on May 2. The move to strengthen the securities market and promote better trading practices comes in the wake of the dramatic fall in share prices of three mainboard-listed stocks last October, which wiped out a combined S$8 billion in their market value over three days. The proposed measures, to be implemented starting at the end of this year, will help further enhance the robustness and resilience of Singapore’s securities market and instil greater investor confidence in its marketplace, said Mr Lee Boon Ngiap, assistant managing director for capital markets at MAS. Stocks listed on the mainboard will be required to have a minimum trading price of 20 cents come March next year, in a move that will affect about 200 companies whose share prices currently fall below the threshold. They will be given a 12-month transition period to “undertake corporate actions” to meet the new requirement, such as through share consolidation. “This is to address risks of low-priced securities being more susceptible to excessive speculation and potential market manipulation,” the MAS and SGX said in their joint statement. And to promote financial prudence, investors will be required to post a minimum 5 per cent of collateral before trading in stocks. The measure, targeted for implementation in mid-2016, puts an end to uncollateralised contra trading as it is currently practised. However, institutional investors, trades settled through delivery-versus-payment mode, and funds from the Central Provident Fund and Supplementary Retirement Scheme will be exempted from this requirement. Mr David Gerald, president and chief executive of the Securities Investors Association Singapore (SIAS), said the measure will encourage investors to trade within their means. “Many investors are used to trading without collateral, but that encourages gambling habits and sometimes over-gearing. I would expect a few to stay away when this is implemented, but over time when the market gets used to this practice, they will come back.” In addition, to improve retail investors’ access to a broader range of listed securities, particularly the higher-priced blue chips, SGX will reduce the board lot size from the current 1,000 shares to 100 shares next January, a move that the SIAS also lauded. “This is a very encouraging move because, right now, small investors can’t participate and build a portfolio involving blue chips. So by allowing them to buy 100 shares at a time, it helps them to build a portfolio of good shares, shares that will perform and are able to give good dividends,” Mr Gerald said. From the middle of 2016, short sellers will be required to notify the MAS of their net short positions based on the lower of 0.05 per cent or S$1 million worth of shares in a listed entity. The aggregated short positions will be published weekly in a move that Mr Gerald said will help investors to make informed trading decisions. Other initiatives announced by the MAS and SGX yesterday include improving the transparency of intervention measures. The Securities Association of Singapore will develop industry guidelines for its members to address concerns resulting from differing practices of trading restriction announcements, with expected implementation by the end of this year. Independent advisory, disciplinary and appeals committees for listings will also be set up by early next year, the MAS and SGX said. They will expand the range of regulatory sanctions for listing rule breaches to include powers to impose fines on issuers, restrict the activities that issuers may undertake, as well as to make offers of composition for minor, administrative or technical breaches.

|

|

|

|

SGX

Aug 5, 2014 19:33:24 GMT 7

odie likes this

Post by zuolun on Aug 5, 2014 19:33:24 GMT 7

Remisiers worry new trading rules will hit market liquidity

Investors' fears that tough regulations may hammer penny stocks could have caused yesterday's market fall

By Jonathan Kwok

5 Aug 2014

REMISIERS are blaming the new share trading rules announced last Friday for sparking yesterday's plunge in penny stocks.

Fears that the tough new regulations will hammer penny stocks and send already-thin trading volumes down even further sent investors fleeing.

The sell-off left the FTSE ST Small Cap Index down 1.07 per cent while the FTSE ST Fledgling Index lost 1.13 per cent. The indices track smaller-sized mainboard companies.

The blood-letting spread to the Catalist board, with the FTSE ST Catalist Index down 2 per cent even though listings there will not be affected by a new requirement for stocks to have minimum prices.

Although the general market was down, the relatively larger stocks held up much better. Mid-cap shares lost 0.46 per cent and the blue-chip Straits Times Index fell 0.78 per cent.

The gloomy sentiment stems from the raft of changes announced on Friday aimed at reducing the risks associated with highly speculative trading .

"Contra trading" - a system present only in Singapore and Malaysia where investors can trade first and pay later without posting any collateral - will end from mid-2016.

Investors will then have to post at least 5 per cent collateral on unsettled positions by the end of a trading session. The collateral can be in cash, stock or bank guarantee. Investors will be able to "tag" the shares in their Central Depository (CDP) account as collateral.

And mainboard-listed firms will have to have a minimum trading price of 20 cents from March next year although there will be a 12-month transitional period. An estimated 200 firms may be affected.

There will be a further period for companies to meet the requirements, and those who fail to take remedial action may be delisted from the mainboard.

Several penny stocks crashed in price last October in a meltdown blamed largely on highly speculative trading.

And while the new rules from the Monetary Authority of Singapore and Singapore Exchange are aimed at such dealing, investors saw that overall trading in penny shares will probably be affected and duly sent prices plunging yesterday.

"Contra trading is a necessary evil for our market to have a fair amount of volume," said remisier Gary Goh. "Nobody wants to trade in a market that's not vibrant."

Remisier Alvin Yong said the market falls yesterday could possibly have been linked to fears that the rules will hit penny stock trading. He added that investors may find that providing collateral will be difficult and leave trading altogether.

That will certainly be bad news for a market that has seen daily average turnover drop to $1.1 billion for the past year, from the $1.4 billion average over the past five years.

Mr Goh said: "If people have the intention to run away from their losses, (the 5 per cent collateral requirement) wouldn't help much."

There was also unhappiness that smaller investors will not be exempt from the collateral requirement, despite earlier suggestions that they should be.

Mr Jimmy Ho, president of the Society of Remisiers, said trades under $50,000 should have been exempted.

The 20-cent price requirement for mainboard shares is on the high side, he added. The minimum price "shouldn't exceed 10 cents", he said.

But Mr Ho said that the linkage from brokerages to investors' CDP accounts is a good move that shows operational flexibility.

The changes will bring Singapore more in line with global norms. People who buy shares on borrowed money need to put up some form of collateral in Hong Kong and New York.

|

|

|

|

SGX

Aug 31, 2014 17:33:18 GMT 7

oldman likes this

Post by zuolun on Aug 31, 2014 17:33:18 GMT 7

|

|

|

|

SGX

Sept 2, 2014 17:41:57 GMT 7

odie and pain like this

Post by zuolun on Sept 2, 2014 17:41:57 GMT 7

Long slog for SGX to get rid of 'penny stock image'BY GOH ENG YEOW 01 Sep 2014 It may take another 4½ years before curtain falls on sub-penny stock tradesIF ANYONE needs reminding just how tough it is to change some of the anachronistic practices prevailing in the stock market, note that it took the Singapore Exchange more than two years to cut the trading of shares from lots of 1,000 shares to 100 shares after first mooting the idea. If that was a slog, then ridding the market of the cheap and cheerful "Mickey Mouse" image that it projects by having ultra-penny shares among top actively traded stocks each trading day will take even longer. No doubt, the guidelines have been set in place with a requirement that mainboard-listed companies must have a minimum trading price of 20 cents. But implementation will only start from March next year with mainboard-listed firms given a 12-month transition period to consolidate their shares if they fail to make the mark. After that, they are given a further "cure period" of three years to take remedial action to meet the minimum 20-cent requirement before they face the pain of delisting. That means that it may take another 4½ years before the curtains are finally drawn on the trading of sub-penny stocks. Even then, this will not completely get rid of the ultra-penny stock image the SGX is saddled with as the minimum trading price requirement will not be extended to Catalist-listed companies, which make up about 20 per cent of all listed companies here. There is even talk that mainboard-listed companies that fail to make the 20-cent minimum trading requirement even after the 4½-year gestation period may be given the choice to move to the Catalist board, which does not have any minimum trading price requirement. And because the minimum trading price regime takes far longer to implement than the move to cut the trading lot size to 100 shares - that happens next January - there is the prospect of some penny stocks becoming even more affordable in the meantime. That is because the minimum outlay for them gets reduced from $10 per 1,000 board lot size to just $1 for a 100-unit board-size, since stocks can be traded to as low as 0.1 cent now. So it is a little puzzling to find readers flagging their concerns over the wisdom of having the minimum trading price raised to 20 cents because they feel that this may crimp the speculative trading element that provides much of the market's liquidity. But as retired stockbroker Narayana Narayana observed in a recent letter, reducing the outlay to as little as $1 per 100-unit lot may even put the share market in competition with gambling alternatives such as 4-D or Toto, if the sole objective of a punter is to try to make as much money in as short a time as possible, lady luck permitting. Still, before we get carried away by the debate over the impact from cutting the trading lot size to 100 shares and raising the minimum trading price to 20 cents, we should examine the driving forces behind the adoption of these measures in the first place. Reader Vincent Khoo noted quite reasonably that reducing the board lot size is not about encouraging a "gambling" or "punting" mentality among retail investors. Rather, it is about making pricey blue chips more affordable to them. When this is carried out in tandem with raising the minimum share price to 20 cents, it may minimise the difficulties a small investor encounters in selling his shares, especially if he ends up holding an odd number after his ultra-penny shares have been consolidated. Of course, there is no guarantee that buying blue chips will make money for investors even though they are considered to be "safer" than small-capitalised counters. It is also debatable whether cutting the lot size to 100 shares will succeed in encouraging retail investors to raise their exposure to blue chips just because the outlay becomes smaller. But the record speaks for itself. Even though ultra-penny stocks regularly dominate the top actives list, the 30 blue chips that make up the Straits Times Index account for over half of the daily turnover on each trading day. So there is never a question as to whether a retail investor will encounter any difficulty in getting in and out of blue chips, unlike the many penny counters that lay dormant for months - sometimes years - only to come alive when a sudden surge in market activity shakes them out of their slumber. They promptly go back to sleep again when the excitement dies down. And if the past is any guide, blue chips do make good investments if an investor hangs on to them for the long term. In the past 10 years, six of the 30 STI components - including Jardine Cycle & Carriage and Sembcorp Marine - have given an average annualised return of over 20 per cent to their shareholders. Another 13 - including OCBC Bank and SingTel - offered more than 10 per cent returns a year. Whether the SGX's latest initiative to promote a wider shareholding culture will succeed remains to be seen. But at least it is offering Singaporeans one more venue to park their nest egg by putting blue chips more easily within their reach. Top volume today with 612 mil shares traded. However at 0.1ct each, the market value of all the trades done on this counter today just amounts to $612,000. No wonder some call our market a Micky mouse market. Interesting though to keep an eye on the market action as it has been moving between 0.1ct and 0.2cts for around 2 years. I am only watching from the sidelines as I am certainly not keen to play such games. Folks who take a bet at 0.1ct are just hoping that a greater fool will buy from them at 0.2cts. Like they say...if you have been in a poker game for a while, and you still don't know who the patsy is, you're the patsy. Do note that Digiland has 42.9 bil shares in issue, as at 30 June 2014. oldman, When the foreign BBs run road in dove and STI peaked @ 3464 points in end-May 2013, it was repeatedly reported that majority of remisiers did not have much business and their income is less than S$1,000 per month, then and now. And SGX also reported that its M-O-M trading volume had plunged drastically. This had directly proven the absence of mass participation from the general public; especially the retail players (on-line and broker-assist). Coupled with the major groups of proprietary day traders/stockists and many gullible retail players who were killed for good in the BAL saga last Oct 2013, only the house, the local fund managers and the brokerage in-house traders are busy playing among themselves in the SGX stock market, day-in-day-out. These whole groups of professional and experienced players are salaried employees who're exempted from paying commissions and their job is mainly churning and hedging their positions in the underlying blue-chip stocks with SiMSCI Futures. It's the same scenario with the US markets; active participants are mainly Central Bankers. All the US Indices can shoot to the roof, without strong supporting volume.  The S'pore stock market is now "A mahjong game within the family!" ==> 关起门来一家亲!  Without participation from the foreign BBs, active players are local FMs + plenty of "bayi" (brokerage firms' house/proprietary traders) + retail players.

|

|

|

|

Post by zuolun on Sept 7, 2014 9:22:43 GMT 7

|

|

|

|

SGX

Oct 8, 2014 15:23:28 GMT 7

oldman likes this

Post by zuolun on Oct 8, 2014 15:23:28 GMT 7

|

|

|

|

Post by zuolun on Oct 16, 2014 5:44:35 GMT 7

|

|

|

|

Post by zuolun on Oct 23, 2014 12:44:12 GMT 7

|

|

|

|

Post by zuolun on Oct 30, 2014 7:56:36 GMT 7

|

|

|

|

Post by zuolun on Nov 6, 2014 15:12:28 GMT 7

|

|

|

|

SGX

Nov 7, 2014 5:32:33 GMT 7

oldman likes this

Post by odie on Nov 7, 2014 5:32:33 GMT 7

Major disruption to SGX trading Published on Nov 5, 2014 4:43 PM The Singapore Exchange (SGX) has suffered a major disruption to its trading system. The trouble started at 2.51pm. -- PHOTO: BLOOMBERG By Grace Leong SINGAPORE - The Singapore Exchange (SGX) has suffered a major disruption to its trading system. The trouble started at 2.51pm. "Connection between SGX's members and our securities and derivatives markets is currently unavailable. SGX is investigating the issue and will keep the markets updated," SGX said in an alert on its website. But one remisier said SGX just issued an e-mail to his brokerage that the market would resume trading at 4.30pm today. SGX did not respond immediately to queries. "The whole market is at a standstill at the moment," another market participant said. "I'm still able to key in orders but it won't reach SGX server, which means, we can't trade. Even offshore brokers won't be able to trade because they have no market access." Remisier Alvin Yong, said: "Brokerages aren't likely to be too happy about this because they are losing commissions. SGX may lose some clearing fees as well. This is a slight blow to its aspiration to be a world class exchange. They shouldn't have have to call for an industry standstill to trading." One broker said the extent of the problem became evident only slowly. "Initially, we thought it was just us. We alerted the backroom and when they investigated, realised other brokerages didn't have access to the markets as well. "But we feel better because other brokerages are having the same problem, which means, everybody can't trade. But we will lose commission fees because our fees rely on volume as well," the broker said. gleong@sph.com.sg - See more at: www.straitstimes.com/news/business/companies/story/major-disruption-sgx-trading-20141105#sthash.m3Q1wSVi.dpuf |

|