|

|

Post by odie on Sept 15, 2014 12:31:12 GMT 7

haha,

bro zuolun,

if reach that low

hoot ah

LOL

|

|

|

|

Post by zuolun on Sept 15, 2014 12:38:35 GMT 7

haha, bro zuolun, if reach that low hoot ah LOL odie, Genting's longterm horizontal support @ S$1.15 is broken convincingly with extremely high volume means the mid-cheng kay (Fund managers) also run road liao...  |

|

|

|

Post by odie on Sept 15, 2014 14:04:43 GMT 7

thanks for advice zuolun bro

i will stay clear

i told my friends to wait for 110

but they were impatient and one jumped in at 118 and another is queuing at 112

LOL

|

|

|

|

Post by zuolun on Sept 15, 2014 14:15:42 GMT 7

thanks for advice zuolun bro i will stay clear i told my friends to wait for 110 but they were impatient and one jumped in at 118 and another is queuing at 112 LOL odie, Once the cheng kay run road signal is confirmed, aggressive punters will piggyback on the ringleader to short big time, not long...unity is strength!  I always glance at naked charts (the top portion) 1st and ignore the indicators (the bottom portion) but Genting's lagging indicators, especially the CMF clearly showed that the major cheng kay + the mid-cheng kay one-by-one run road since Nov 2013; nobody wants to be a stabilising manager liao...  Genting SP closing at day's low @ S$1.17 with high volume done at 33.3m shares on 12 Sep 2014 showed that the strong selling pressure had accelerated as the CMF indicator has been extremely bearish since Nov 2013.Genting SP Chart Pattern: - Riding on Corrective A-B-C Wave; it never rains but it pours.

- In technical analysis, a stock that has made a new low is a prime target for short, not long.

|

|

|

|

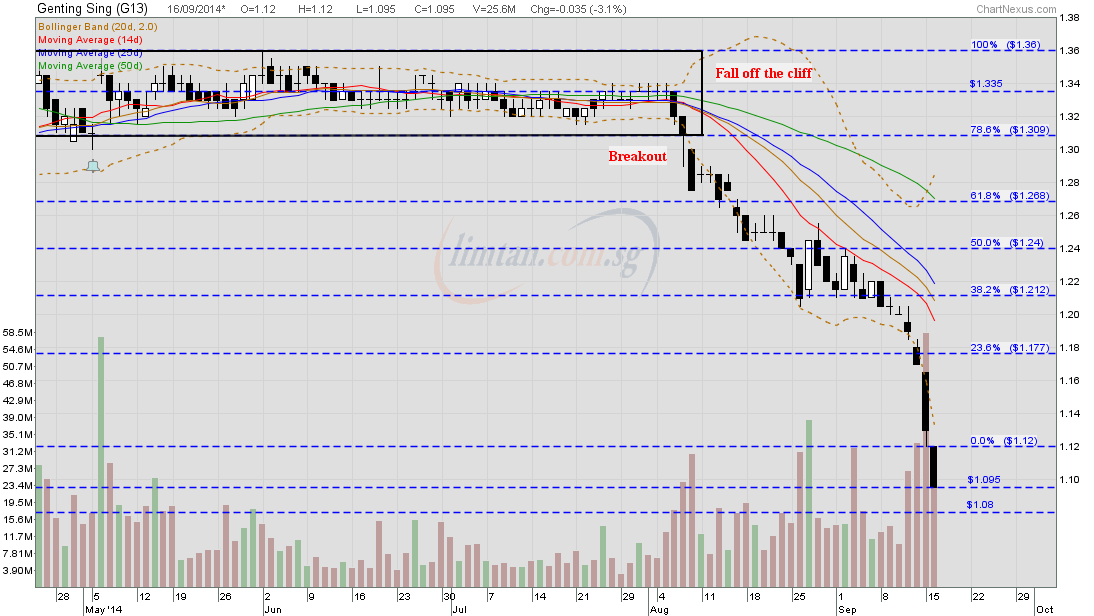

Post by zuolun on Sept 16, 2014 9:03:06 GMT 7

Genting SP — Bearish Bollinger Bands BreakoutGenting SP had a long black marubozu @ S$1.095 (-0.035, -3.1%) on 16 Sep 2014 at 10am. Immediate support @ S$1.08, immediate resistance @ S$1.12.

|

|

|

|

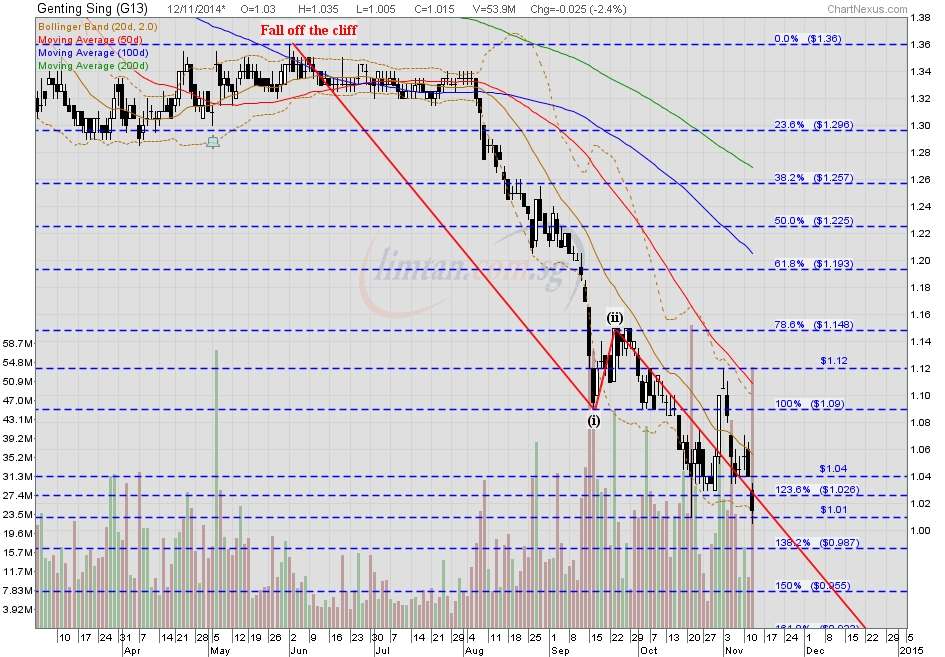

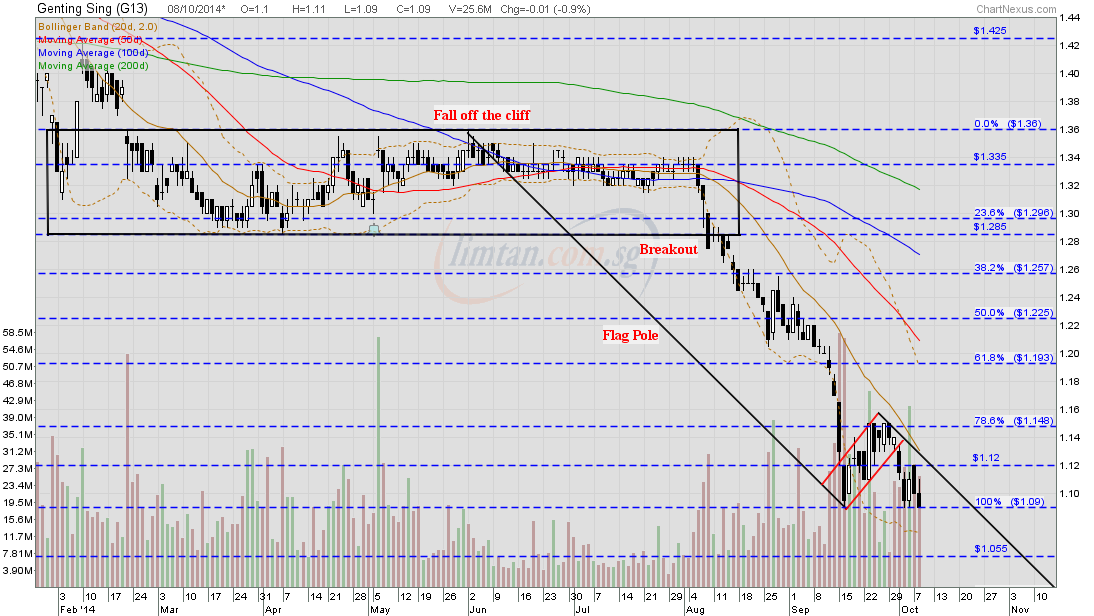

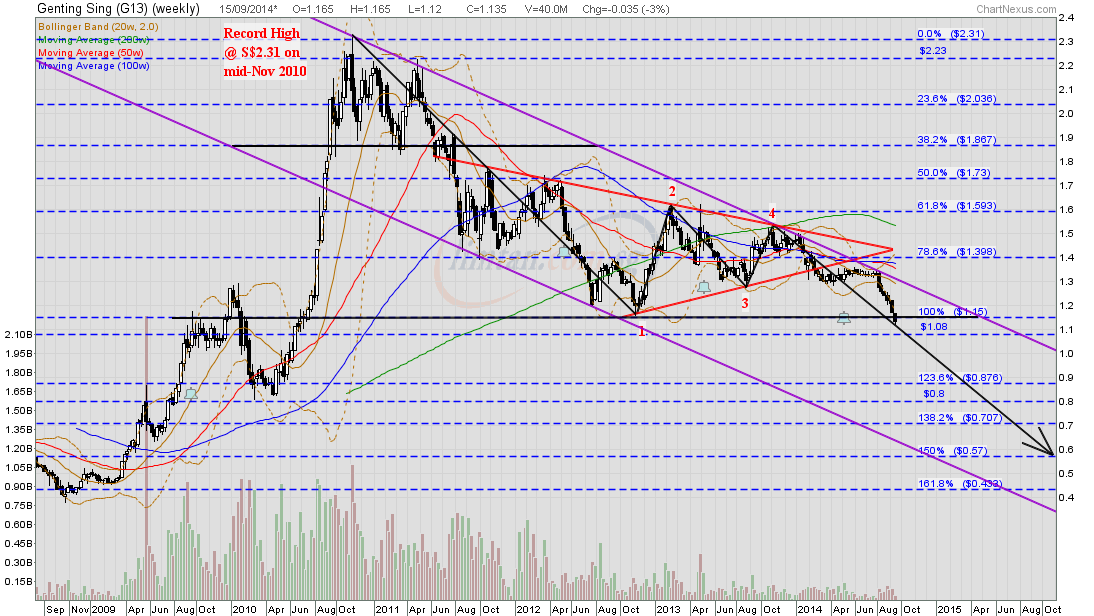

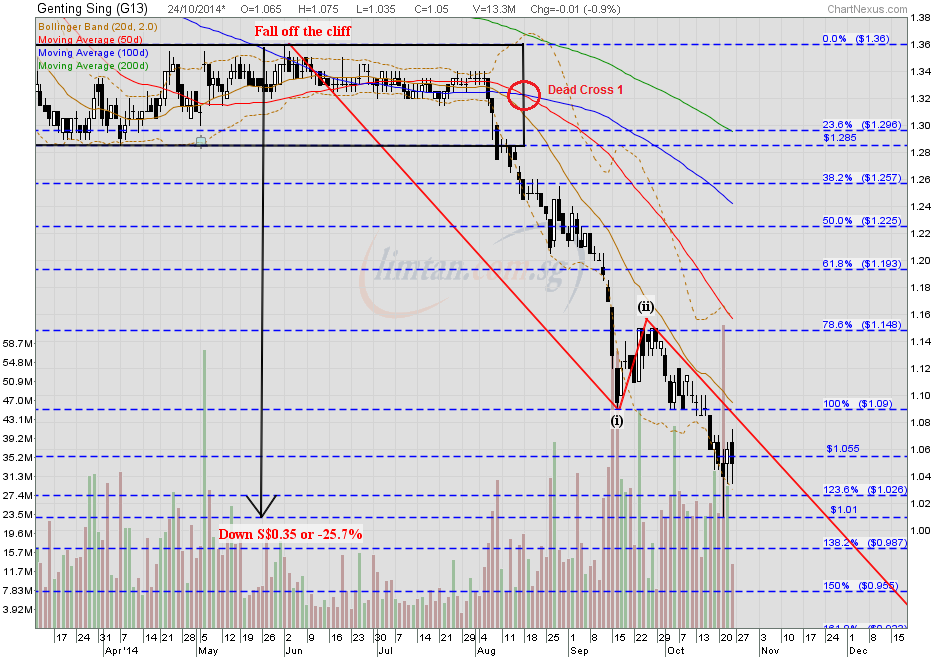

Post by zuolun on Oct 8, 2014 16:47:37 GMT 7

Genting SP — Bear Flag Breakout, major bearish trend reversal with 5-Wave down, TP S$0.80Genting SP closed with an inverted hammer @ S$1.09 (-0.01, -0.9%) with 25.6m shares done on 8 Oct 2014. Immediate support @ S$1.055, immediate resistance @ S$1.12.  Genting SP (weekly Mid-Nov 2010 to 15 Sep 2014) — Bearish Descending Triangle Breakout, neckline @ S$1.15, interim TP S$0.80 Genting SP (weekly Mid-Nov 2010 to 15 Sep 2014) — Bearish Descending Triangle Breakout, neckline @ S$1.15, interim TP S$0.80

|

|

|

|

Post by zuolun on Oct 24, 2014 16:01:43 GMT 7

Genting SP's Perpetual Bonds issued in 2012Genting SP — A "Waterfall Decline" with 5-Wave down, Interim TP S$0.80Genting SP had a spinning top @ S$1.05 (-0.01, -0.9%) with 13.3m shares done on 24 Oct at 4.50pm. Immediate support @ S$0.985, immediate resistance @ S$1.09.

|

|

|

|

Post by zuolun on Nov 12, 2014 14:55:09 GMT 7

|

|

|

|

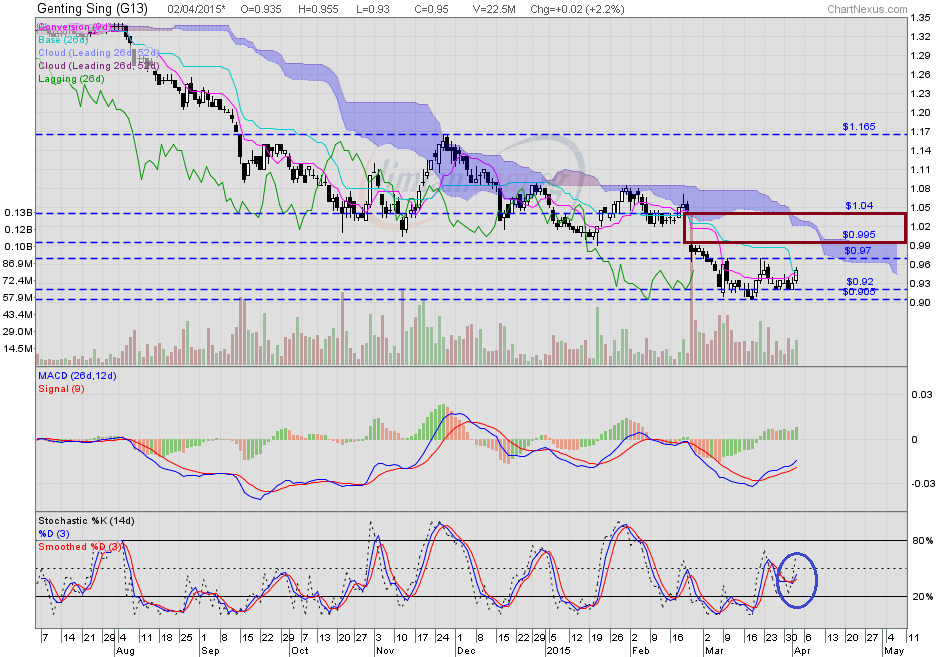

Post by odie on Feb 25, 2015 8:35:40 GMT 7

UPDATE 1-Genting Singapore's profit falls as premium segment drags

Tue Feb 24, 2015 5:34am EST

* Gaming revenue falls 9 pct to S$461.3 mln

* Adj EBITDA misses analyst estimates (Adds comments, details on new hotel)

Feb 24 (Reuters) - Casino operator Genting Singapore Plc said it was focusing its marketing efforts on the mass market segment after net profit fell 30 percent in the fourth quarter, hurt by poor performance in its business from high rollers.

Genting's net profit fell to S$118.9 million ($87 million) for the December quarter, from S$170 million a year earlier. Gaming revenue fell 9 pct to S$461.3 million.

Genting's core earnings, or adjusted earnings before interest, tax, depreciation and amortisation (EBITDA), fell 24 percent to S$190.2 million in the fourth quarter, below an average estimate of S$338 million in a Reuters survey of four analysts.

Genting's Resorts World Sentosa and Las Vegas Sands' Marina Bay Sands resort have been vying for a shrinking group of high-rolling players, who are deterred by China's corruption crackdown and economic slowdown.

"In recent months, the macro-economic ecosystem has been altered to an extent that the gaming industry has to adjust to a new norm," Genting Singapore said in a statement.

"RWS has been reorganising its gaming programmes to focus marketing initiatives towards the foreign premium mass and mass market segments."

The company said its premium-player market segment was hurt by significantly below-average win percentage, meaning players won more than expected, and rolling volume.

The company said it was scheduled to open its new 550-room, hotel in Jurong Singapore in May, which will help drive more visits to the casino. The hotel is expected to add much-needed room capacity and improve visitors from the Malaysian market. ($1 = 1.3614 Singapore dollars) (Reporting by Aradhana Aravindan; Editing by Gopakumar Warrier)

|

|

|

|

Post by odie on Feb 25, 2015 8:37:13 GMT 7

Genting Singapore Q4 profit falls 30 pct

SINGAPORE Tue Feb 24, 2015 4:52am EST

Feb 24 (Reuters) - Casino operator Genting Singapore Plc's net profit fell 30 percent in the fourth quarter as gaming revenue declined, hurt by poor performance in its premium segment.

Genting reported a net profit of S$118.9 million ($87 million) for the quarter ended December, compared with S$170 million a year earlier. Gaming revenue fell 9 pct to S$461.3 million.

Genting's core earnings, or adjusted earnings before interest, tax, depreciation and amortisation (EBITDA), fell 24 percent to S$190.2 million in the fourth quarter, below an average estimate of S$338 million in a Reuters survey of four analysts. ($1 = 1.3614 Singapore dollars) (Reporting by Aradhana Aravindan; Editing by Anand Basu)

|

|

|

|

Post by zuolun on Feb 25, 2015 9:14:04 GMT 7

|

|

|

|

Post by odie on Feb 25, 2015 13:14:41 GMT 7

thanks zuolun bro for advice cheaper to just go and hoot toto $12m this friday LOL  |

|

|

|

Post by zuolun on Feb 26, 2015 15:03:16 GMT 7

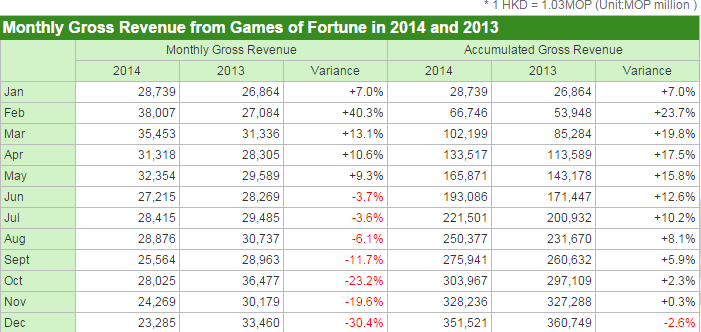

Macquarie's review on Genting: Underperform TP S$0.95 ~ 24 Feb 2015 "More downgrades to follow; No catalysts in sight; Not the right time to bottom pick." Nothing to see here in Genting SPGenting - Shifting focus to mass, CIMB rated ADD TP S$1.20 ~ 25 Feb 2015 GENS’s FY14 adjusted EBITDA of S$1.16bn was below expectations at 88%/89% of our/consensus full-year forecasts. The underperformance came from: 1) lower-than-expected VIP hold rate of 2.2% (vs. our forecast of 3.2%), 2) lower rolling chip volume, as it was more careful in extending credit to VIPs, and 3) higher bad debt expense. We cut our FY15-16 EPS forecasts by 1-8% in expectation of lower rolling chip volumes and higher bad debt charges. Our DCF-based target price falls to S$1.20 as a result. GENS remains an Add, with overseas expansion as the key re-rating catalyst, while the opening of Genting Hotel Jurong in mid-2015 will provide downside protection to mass GGR at GENS’s Resorts World Sentosa (RWS). VIP disappointed, likely to get worse before getting better 4Q14 adjusted EBITDA fell 25% qoq to S$190.2m, largely due to lower VIP gross gaming revenue (GGR) and higher bad debt charges. The VIP hold rate of 2.2% was below the theoretical average of 2.85% and our estimate of 3.2%. Rolling chip volume of c.S$15bn in 4Q fell short of expectations as RWS was more cautious in extending credit to VIPs. As a result, its market share fell 6% pts qoq to 54%. Bad debt charges doubled to S$82m, which management explained was a result of delayed repayment for credit granted to customers 9-12 months ago. The VIP business is expected to remain challenging in 2015, with bad debt provisions staying high over the next 2-3 quarters. Shifting focus to mass, with the help of its Jurong hotel The mass segment fared better, as RWS’s market share of mass GGR fell only 1% pt to 43% in 4Q, although its competitor MBS is building a stronghold in the mass gaming market. In the past, RWS’s strength was in the VIP segment but it is now shifting focus to draw more mass and premium mass visitation from Southeast Asia to offset the fall in VIP volumes. GENS is ramping up marketing efforts and hopes to attract more mass visitation in 2H15, with the Genting Hotel Jurong that will add 550 rooms when it is fully opened in Jun. Overseas opportunities remain the key catalyst Management remains optimistic about opportunities in Jeju and Japan. The positive developments include receiving construction approval for Resorts World Jeju and its ground-breaking ceremony on 12 Feb 15. Furthermore, GENS has exited most of its portfolio investments in FY14 to prepare for the two big projects in Jeju and Japan, which yielded net inflow of S$443m. GENS ended FY14 with net cash of S$2.0bn to pursue expansion opportunities.

|

|

|

|

Post by zuolun on Mar 5, 2015 13:29:30 GMT 7

Corporate News

4 Mar 2015

In a bid to expand its cruise business worldwide, Genting Hong Kong plans to acquire luxury cruise line Crystal Cruises for US$550 million from Japanese shipping firm Nippon Yusen Kaisha (NYK). "The acquisition will enable the group to take advantage of the growing global demand in the luxury brand market and maximise its revenue and profitability," said Genting Hong Kong in a statement. On completion of the takeover, Crystal Cruises will become an indirect wholly owned subsidiary of Genting Hong Kong, a leisure, entertainment and hospitality group which operates the Star Cruise shipping line and has interests in Norwegian Cruise Line (NCL) and Resorts World Manila.

Genting Singapore's Resorts World Sentosa plans to raise S$2.27 billion of bank loans, Bloomberg reported, citing sources familiar with the deal. The five-year syndicated deal will be split into a S$1.75 billion amortising term loan, a S$500 million revolving facility, and a S$20 million bank guarantee

facility.

|

|

|

|

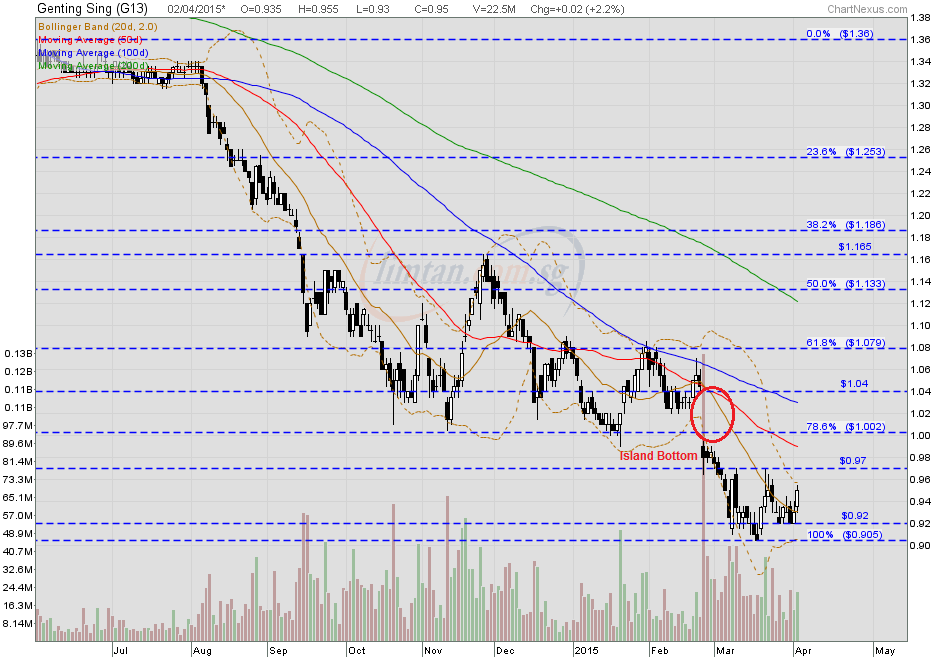

Post by zuolun on Apr 12, 2015 7:47:02 GMT 7

|

|