|

|

Post by zuolun on Dec 29, 2013 15:37:37 GMT 7

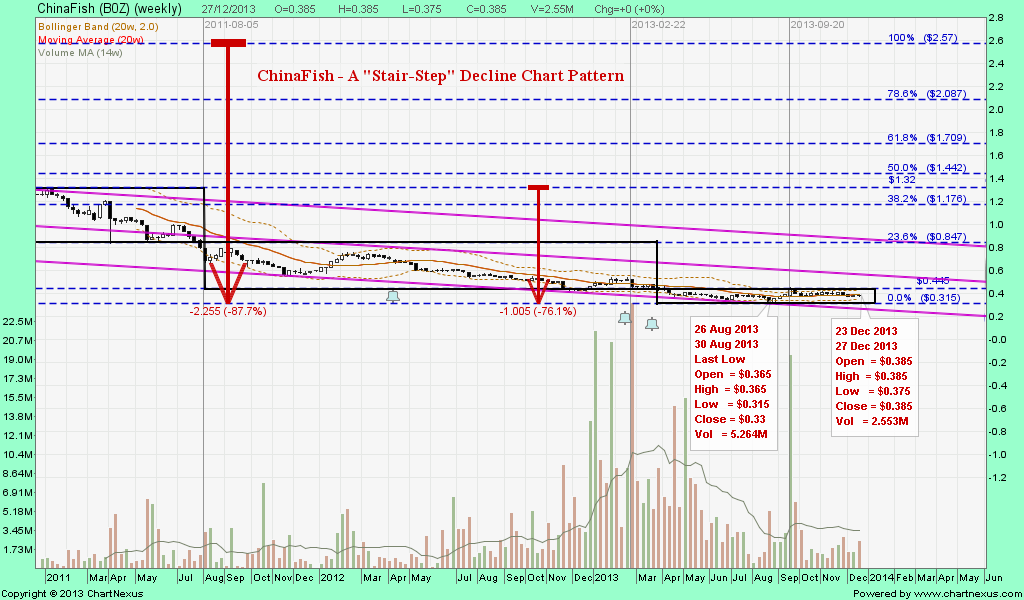

ChinaFish — Symmetrical triangle breakout ChinaFish (weekly) — A "Stair-Step" Decline Chart Pattern ChinaFish (weekly) — A "Stair-Step" Decline Chart Pattern

ChinaFish (monthly) — Jan 2006 to Sep 2012 ChinaFish (monthly) — Jan 2006 to Sep 2012

|

|

|

|

Post by stockpicker on Jan 7, 2014 9:45:33 GMT 7

It is just interesting to note how many picked this China Fish (CF) just to find that it is not moving higher especially when they have recently acquired Copenica, a Peru fishing firm which is more than twice its size for something more than S$1bil. Furthermore, many are of the view that World's fishing grounds are diminishing and the fish, fish meals and oil price have to go up sooner and later. Yes, the fish meal prices etc have gone up but sad to say, not the price of China Fish.. why?

Whether CF can go up later is anybody's guess but from financial analysis view point, CF has more than double its Long Term Debt from $600mil to $1.3 biln this 4th quarter. It has reported a demure quarterly profit of only $18 mil, even less than last quarter. Its net EBITDA debt ratio has gone up from acceptable 3.51 to now 10.88, which is more than double the acceptable ratio of 4.5 for going concern. Furthermore, their current ratio has dropped from 2.3 to now 1.0 which shows that they are terribly short of operating fund.. unless more profits can be reported which should improve these financial figures otherwise, we should see the price of CF having trouble maintaining the present figure..bearing in mind that Copenica was losing money before it was acquired by CF for some reasons although all investors are now hoping that the recent increase in the quota of Peru's anchovy fish will bring CF the joy... will it? Lets watch..

|

|

|

|

Post by oldman on Jan 7, 2014 15:39:57 GMT 7

|

|

|

|

Post by stockpicker on Jan 7, 2014 17:15:14 GMT 7

Say what we like, this CF went up 6.4% or 2.5 cts today on decent volume. It is always hard to catch what the BBs wanted. The buy up was quite heavy in the morning trades and the sell down was also heavy in the afternoon trade. Are they gaming? Anyway, CF played a "fishing game" by issuing unlisted warrants to CAP III-A Limited @ 0.52 for a sum of S$40million which CAP III can only convert to share at 0.52 . So, everyone was speculating that someone like CAP III will want to push CF price to more than 0.52..

|

|

|

|

Post by stockpicker on Jan 13, 2014 22:49:01 GMT 7

Take a look at China Fish today and saw a bearish engulfing candlestick formed. This is not a good sign particularly when the price cannot clear the last high on 25 Sept after a price pushed up by heavy volume just to see that the volume is exhausted. China Fish is likely to dismount if it cannot regain its position by crossing over the resistance.  |

|

|

|

Post by stockpicker on Jan 28, 2014 18:55:31 GMT 7

China Fish(CF) has cleared hurdle and closed up today @ 0.455, threatening to go higher. But it is interesting to know whether it could reached the target price of 0.52 that many people has speculated.

The 0.52 was the price that CF stipulated a must-reach-price before CAPIII-A can convert 90 mil warrants to ordinary shares. CapIII-A got the 90 mil warrants for the price of a song which is US$1/-. This appears to be a trick to induce CapIII-A not to sell existing but buy CF shares at 0.52. CF played the same trick in 2010, offering a 3rd party with 26 mil warrants for US$1/- which can only be converted to share @ 2.1 when the prevailing price was 0.8. The price never reach that high and the warrants expired in 2013.

Many speculated that this time would be different because of the lower price to reach. But we mustn't forget that this time,

CF has acquired Copeninca and choked up another $1bil of long term debt. It can be a "time bomb" which can explode anytime if not properly handled. If one were to do a FA, it will not be hard to find that the debt of $1bil will appear to be too hard for CF to swallow especially when Copeninca was losing money before CF took over, although CF managed to turn Copeninca round within a short 5 months period which is quite remarkable.

A scenario would be for the price to reach 0.52 and CAPIII-A, instead of converting warrants to share, starts selling its existing shares in hand. The other scenario is for the price never to reach 0.52. Many are speculating to be the former and this hope is presently driving the CF's price higher.

|

|

|

|

Post by stockpicker on Feb 3, 2014 14:53:58 GMT 7

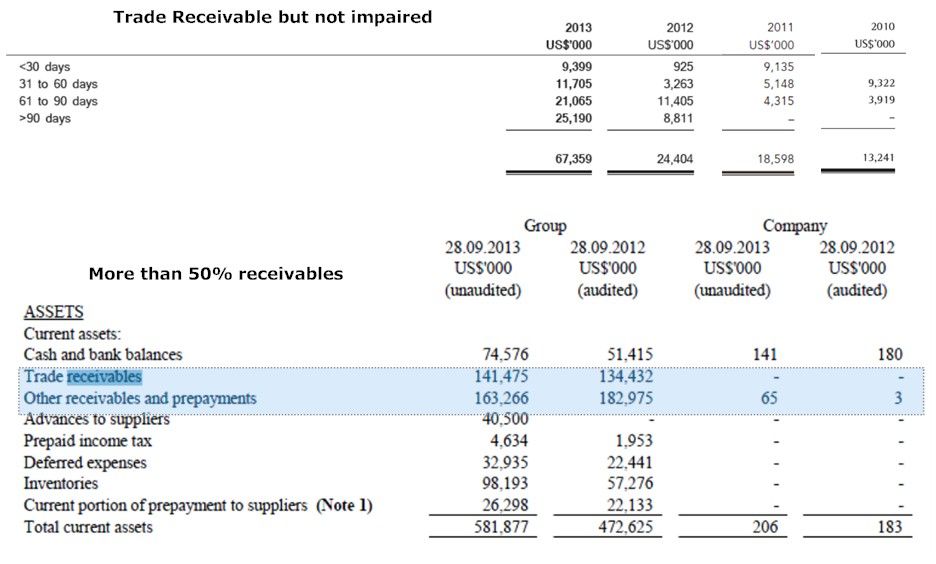

One would need to have a lot of courage to buy up CF although speculators were trying to say that it would reach 0.52 because of the "trick" of the free warrant issued to CAP-III. Check through the financial data, understand that CF, not only have a fat loan, has trouble getting to receive its payment as its receivable kept piling up over the years as shown in the attached. Its receivable is already more than 50% of the total asset and the >90 day receivable has increased from 13 mil in 2010 to now 69 mil. They are hoping that the newly acquired Copenica will bring better finance.. will it? Copeninca was losing money before CF took over..  |

|

|

|

Post by oldman on Feb 3, 2014 15:30:21 GMT 7

If I read the document on the warrants correctly, there is no risk to the investor as the 96,153,846 warrants were issued at a cost of $1! Even though the exercise price may be high at 52cts, it is really of no relevance given that their downside is just the nominal value of $1. What a wonderful arrangement for CAP III-A Limited. When one side wins big, usually another side loses big as well ..... investors are best to know which side they are on.  infopub.sgx.com/FileOpen/CFGL-Proposed_Issuance_Warrants-051213.ashx?App=Announcement&FileID=266965 infopub.sgx.com/FileOpen/CFGL-Proposed_Issuance_Warrants-051213.ashx?App=Announcement&FileID=266965 |

|

|

|

Post by stockpicker on Feb 3, 2014 17:15:05 GMT 7

Think many retail investors know why they are buying. Just like what they've said most of the time, they are the best, they know when to hold the share and when to dump. the greedy ones will want to hold the share until it reaches 0.52 then dump. They think they won't be the last one caught. Just not sure how many greedy ones are there.

|

|

|

|

Post by stockpicker on Feb 22, 2014 17:57:52 GMT 7

There was a question in one local forum asking what wrong with CF's $1bln debt acquired recently to take over Copeninca, a Peruvian fishing giant. He said SingTel recently finanlising another loan of about $1.8bln but he quickly added that it may not be a good comparison. Indeed, he was correct.

When one has a steady income, it is fine to borrow more to buy more houses provided the income can repay the loan within a certain period. For companies, this is around 4.5 to 5 years; as for individuals, it is much higher because the interest is much lower for buying houses which is almost risk free. SingTel presently has a total debt of about SGD16 biln and the debt to EBITDA is about 3.4, borrowing another USD$1.8 biln would just bring it below 4.0 which is acceptable. As for CF, before acquiring Copeninca, its debt to EBITDA was already around 4 to 4.5, prompting Moody, S&P and one other agency to downgrade its debt rating. After acquiring Copeninca and swallowed up another SGD$ 1 bln debt, the debt to EBITDA is more than 10 which is alarmingly high. Unless CF can fetch future earnings which is around 3 times the present; otherwise, the business will be a going concern.

|

|

|

|

Post by stockpicker on Feb 28, 2014 8:36:13 GMT 7

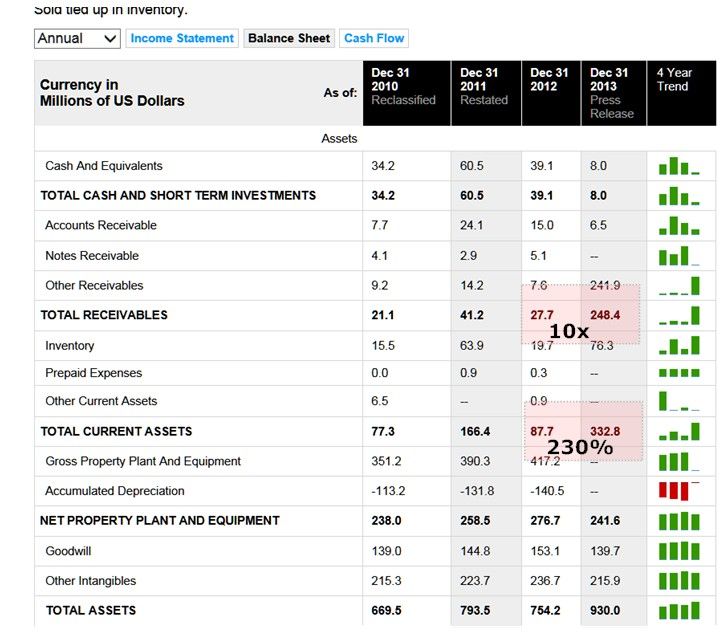

Going through Copeninca's financial reports, found something interesting as shown. It has a glaring 10x lift in other receivable from 27mil in 2012 to 248m in 2013 and that boosted the current assets by 230% from 87mil to 332mil, making the accounts looked slightly better than China Fish. This however, could not hide some accounting tests that show the company's finance is not as healthy as it looked. As the receivable is classified under "other receivable", so it may be something that is not directly related to business. It may a pledge that "drop from the sky". It may also be bad debts that are being recalled under the new management. The Copeninca website is not working properly, there was no way to check. It is good to be careful... investing.businessweek.com/research/stocks/financials/financials.asp?ticker=COP:NO&dataset=balanceSheet&period=A¤cy=native(please add http:// infront of the above text because the forum does not accept the URL  |

|

|

|

Post by stockpicker on Mar 3, 2014 6:59:04 GMT 7

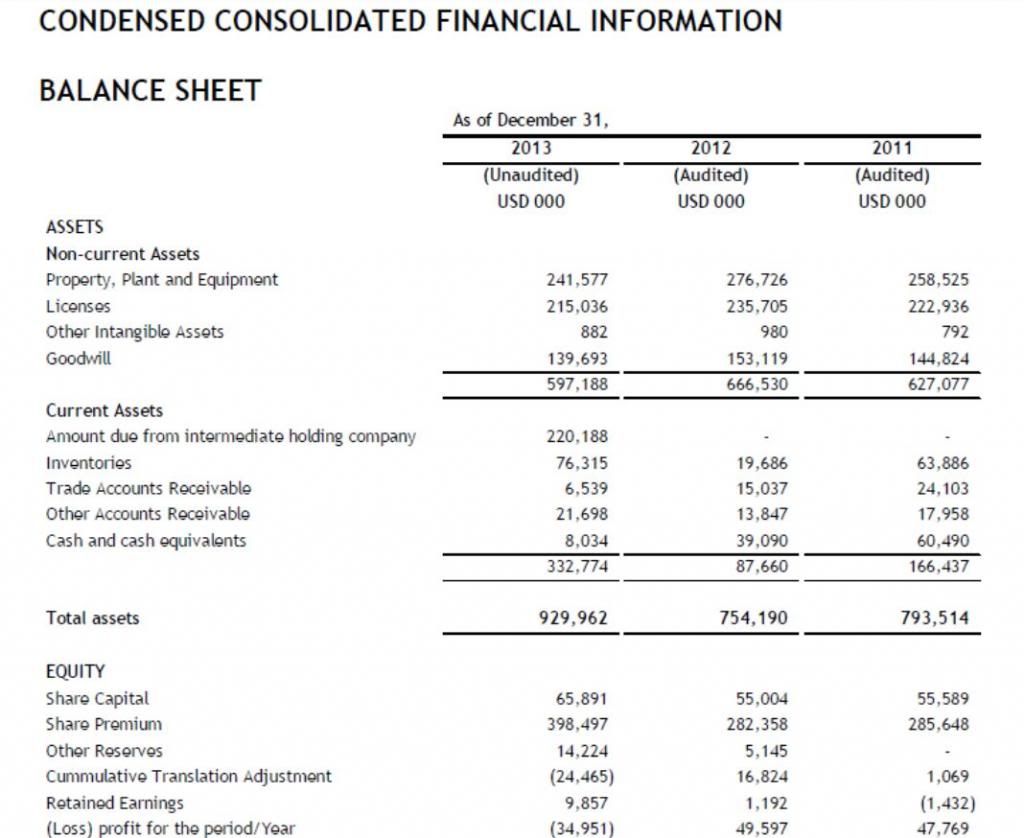

Found out that the outstanding amount of USD$220 mil out of the USD$248 receivable was the "amount due from immediate holdings companies". Not quite sure why this was not reflected in past years' balance sheets. It may be a juggling of funds for tax avoidance previously but Copeninca has been losing money except for year 2011 and 2012. It would be good to monitor if it is just juggling of funds.  |

|

|

|

Post by stockpicker on Mar 3, 2014 7:41:41 GMT 7

It is just amazing to see how greed works. China Fish was due for a correction when it failed to clear 0.44, forming a bearish engulfing on 13 Jan. A strong hand pushed the price up on 15 & 16 Jan with sounding confidence that it was heading for 0.52, the target price for conversion of the CapIII's warrants. However, the excitement stopped, fell short of closing at the upper trendline; thereafter, the price dropped towards ex-date and now below the lower trendline. There appears to be some fears that works along with greed. Going ahead will be tough for CF unless it can recover and clear above the trendline..Going below 0.375 will be dangerous.  |

|

|

|

Post by stockpicker on Apr 22, 2014 11:12:07 GMT 7

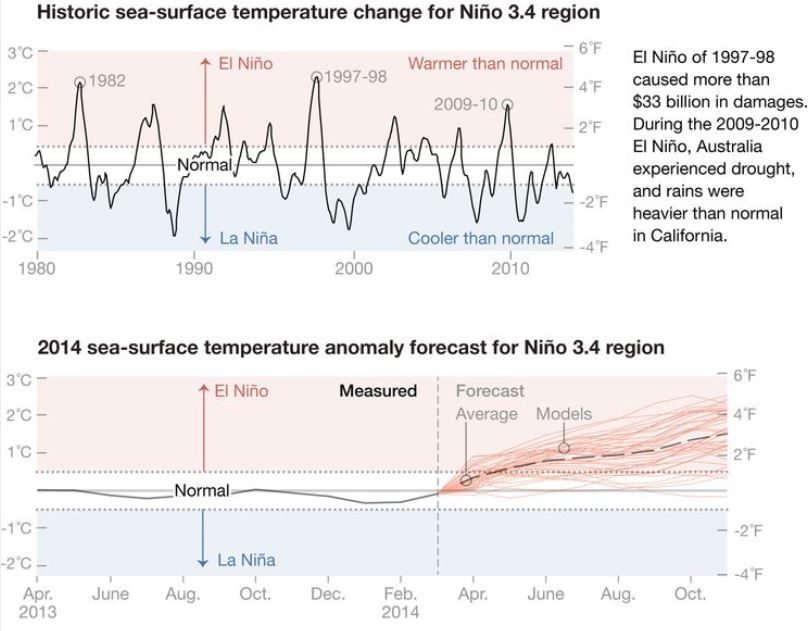

It doesn't matter if the company is facing a great threat so long as someone in the chair came up and said "2014 will be a great year and we can achieve this and achieve that..bla bla bla", the share price of the company will keep going up and up.. Fish catch depends very much on weather. When there is El-nino, the fish catch may be reduced by up to 60% as the fishes will go to other cooler grounds. Last year, the Fishery companies in Peru including Copeinca that was recently acquired by China Fishery, lose money and they all blamed El-nino. But if we check the National Geographic site, there was actually no El-nino in 2013 but there was El-nino predicted in 2014. Is this China Fishery counter attractive as painted? It is therefore good for valued investors not to listen to listen to hearsay but do the homework. news.nationalgeographic.com/news/2014/04/140412-el-nino-weather-forecast-science-climate-change-la-nina/ |

|

|

|

Post by stockpicker on May 1, 2014 12:13:06 GMT 7

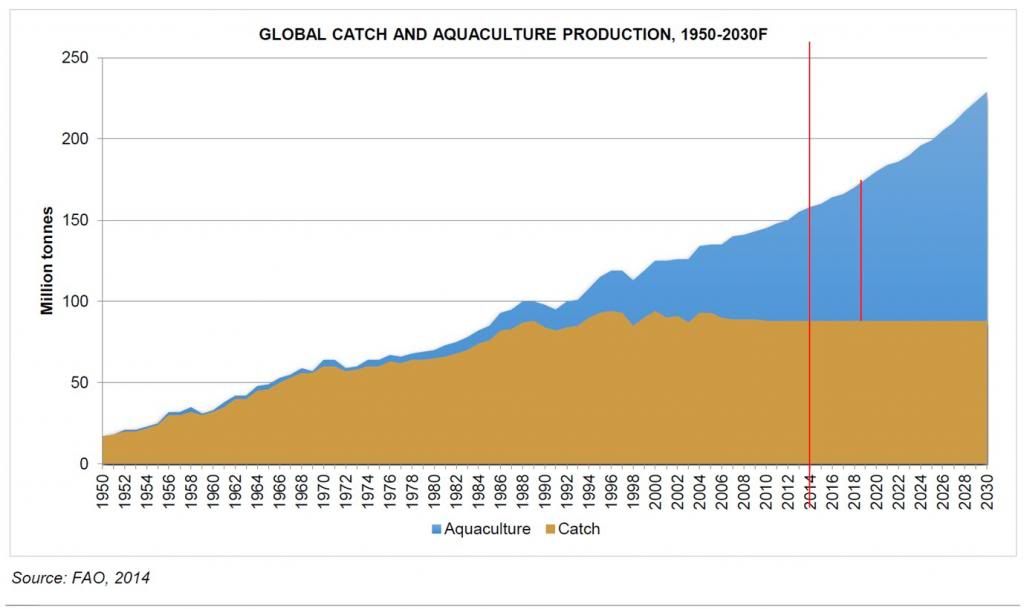

Someone was having the view that CF is a future gem that will shine as the fish prices will increase becos of lesser and lesser catching grounds available. Unfortunately, they have forgotten that there are alternatives which is aquacultural fish farms. These farms are turning out more and more fish produces each year and will overtake the wild catch production by 2018. There was an argument that some fish such as tuna cannot be reared successfully in captivity and must depend on wild catch. Little do they know that the aquacultural fish farms can always mimic the sea environment and there is no species that cannot be reared in captivity. It is a matter of whether it is cost effective to do so. But if the wild catch fish price is going up, there is no guarantee that there wouldn't be no replacement stock from the aquacultural farms. Then there was another argument saying that aquacultural fish farm would need fish meals which is produced from wild catch fishes. It is just not sure why fish meals cannot be made using other substitutes such as animal feeds and meats. I once reared a pool of 10 Japanese carps for more than 10 years and fed them only with normal breads, scrimps and egg mixtures, sometimes, just mixed with left over biscuits as the normal carp or fish food were too expensive. There was also one more argument saying that China will need a lot of fish and Peru can supply them. but they do not know that China is also having a thriving fishing industry and their aquacultural farm produce are more than 6 times of what Peru can produce. Going forward, it is foreseen that unless CF can innovate and go for aquacultural fish farm also, there is a good possibility that CF and the like would be phased out sooner or later just like the natural pearl companies and harvesters. Natural pearls used to be the only ornamental pearls available and now it has been taking over by cultured pearl which has 95% of the World's pearl production.   |

|