"There's a sucker born every minute."Naibu’s disappearing-director scandal reminds us why we need friends on the board ~ 24 Feb 2015

Chinese sportswear brand Naibu loses contact with executives ~ 19 Feb 2015

Naibu, the most undervalued stock in the market? ~ 7 Mar 2014

Why I am shorting Naibu ~ 17 Jan 2014

Naibu Global Stock May Drop Like a Stone ~ 18 Sep 2013

Naibu ready to cut a dash ~ 30 May 2013

Naibu: Fundamentally undervalued ~ 24 Nov 2012

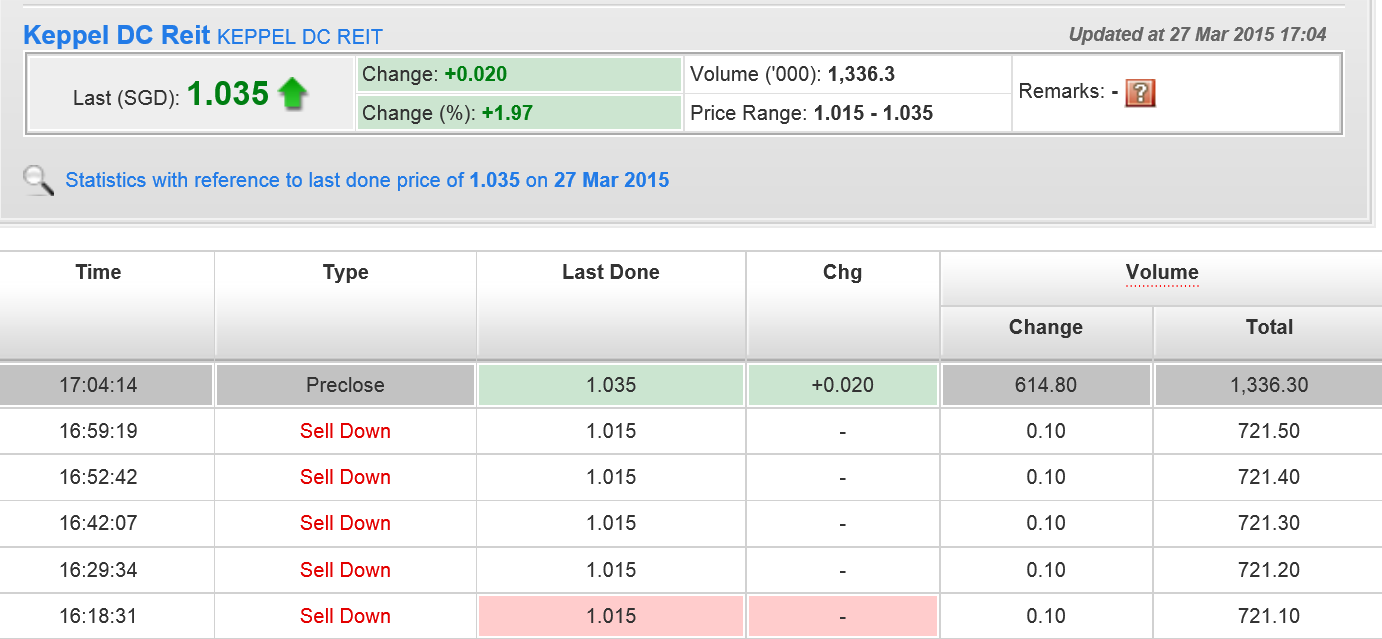

From the first trading in Apr 2012

From the first trading in Apr 2012 to the suspension on 9 Jan 2015, Naibu's share price has collapsed 90%.

奈步广告:奈步秋冬走秀Naibu's commercial video 奈步(中国)有限公司 Naibu

奈步广告:奈步秋冬走秀Naibu's commercial video 奈步(中国)有限公司 Naibu ~

A Chinese manufacturer and supplier of branded sportswear China’s intangible assets at home in AimThere is a reason why the junior market has been dubbed ATM

China’s intangible assets at home in AimThere is a reason why the junior market has been dubbed ATMBy Matthew Vincent

20 Feb 2015

If you are transporting 50,000 truckloads of timber across China, it can be hard to see the wood for the trees. If you are trying to audit 68 sq km of Chinese orange groves, you can easily find yourself a few fruit short of a still life. But how, exactly, do you lose track of 2,810 shops full of fluorescent trainers and dayglo “leisure wear”, spread across 21 provinces and three municipalities?

That is the question being asked this week in London, after the non-executive directors of Naibu, a Chinese sportswear company quoted on the Alternative Investment Market, admitted they had lost all contact with the company’s chairman and executive director and had no information on its operations, or its “current financial position”.

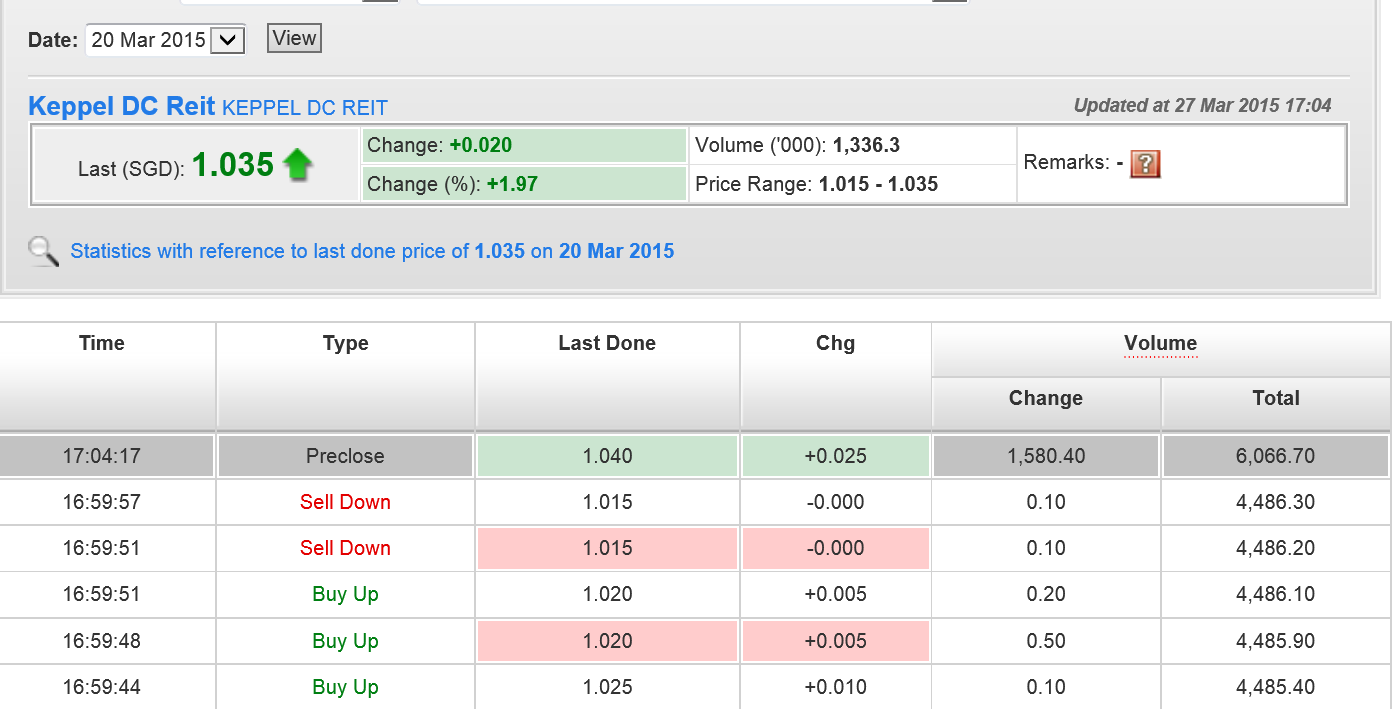

Shareholders are well aware of theirs, however: from their first trading in 2012 to their suspension last month, Naibu’s shares have lost 90 per cent.

Other instances of misplaced China bullishness perhaps seem more understandable. In 1995, timber group Sino-Forest floated in Toronto, rose to a market value of $6bn and gained US fund manager John Paulson as lead shareholder before collapsing amid allegations that its logs were illusory. Fruit producer Asian Citrus came to the London Stock Exchange in 2005 and grew its share price sevenfold in five years — before losing 90 per cent of its value on claims that it had over-counted its oranges.

One Chinese company, shoemaker Ultrasonic, even offers hope to Naibu investors. After listing in Frankfurt in 2011, its shares fell 79 per cent in a day last year, on news that its chief executive, and much of its cash, had vanished. They recovered when he turned up a few weeks later claiming he had simply lost his mobile phone.

However, every new misstep by a Chinese company calls into question the functioning of western exchanges, the role of non-execs, and the integrity of corporate advisers.

What does it say about London’s Aim that it enabled Naibu’s owners to float just 9 per cent of their shares, gain a £68m valuation for the company and — in the case of two of the top three original shareholders — offload entire stakes, amounting to 30 per cent of the group? Little wonder one FT hack suggests the market be renamed ATM. Sino-Forest’s senior executives found Canada’s market as bountiful: listing and offloading $83m of shares before their company collapsed.

What exactly were the non-execs doing? Under the Aim rules, Naibu’s did not have to adopt the UK Corporate Governance Code, but they were required “to aspire to achieve the key elements”. Yet, in spite of claiming 30 years’ experience of the City, they seemed to do little for their £60,000-a-year part-time salaries beyond setting up an Aim compliance committee — and perhaps hanging on the telephone, in vain, to Fujian province.

And what of the role of corporate advisers? Naibu’s nominated adviser, before it relinquished its licence, filled the company’s Aim admission document with claims that it was China’s 10th-largest sportswear brand — in a survey commissioned by Naibu itself — in a booming market. For its diligence, it took an initial fee of £30,000, a further fee of £170,000, and commission at the rate of 5 per cent of the aggregate sums raised. One of the other pearls of wisdom in its document was the etymology of the brand name: “Nai means tenacity, persistence and endurance. Bu reflects method or way.”

Its non-executives will need plenty of the former as they keep pressing redial.

------------------------------------------------------------------------------------------------------------------------------------------

The dangers of share tips – Naibu ~ 21 Sep 2014

Naibu game changerInvestors Chronicle

15 Sep 2014

It's not often you have the chance to buy shares in a company trading below cash on its balance sheet and at a third of its book value. It’s even rarer to find a company offering a near 10 per cent dividend yield and where net earnings for just one financial year equate to almost all of its market value. However, this is the tantalising investment opportunity in the shares of Naibu Global International (NBU), a Chinese maker and supplier of branded sportswear and shoes.

Offering a branded range of 530 items through more than 3,100 stores that are operated by 25 distributors in the second, third and fourth tier cities in China, Naibu primarily targets the disposable income of young consumers. Primarily, these are aged between 12 and 35.

Naibu is proving incredibly successful at it, too, as revenues in the first half of last year rose by a fifth to £95m to drive pre-tax profits up by 16 per cent to a record £21.5m. These figures have been converted from Naibu's reporting currency of the Chinese renminbi into sterling at the current rate of £1:10.0Rmb. And the momentum was maintained into the second half as a pre-close trading statement last week revealed that revenues surged 15 per cent to an all-time high of £193m for the year as a whole. On this basis, analysts at broking house Daniel Stewart predict pre-tax profits will have risen by 9 per cent to £39.3m in 2013 which net of a 26 per cent tax charge means that EPS should be around 55.7p. In other words, the shares are trading on a PE ratio of 1.1!

And it's not as if Naibu has any financial worries to justify such a bargain basement valuation. In fact, net cash at the end of June was £40m, or 10 per cent more than the company's current market valuation. Moreover, with profits rising and cash flow generation from operating activities robust, the company paid out an interim dividend of 2p a share in December having already paid out a final of 4p a share in September. This means the payout of 6p a share is covered more than nine times by EPS of 55.7p to produce a dividend yield of over 10 per cent.

For this year, expect a further ramp up in output as Naibu is bang on track to move into a new production facility at Quangang by the end of February, which will expand production capacity from eight to 10 lines. Chairman Lin Huoyan is certainly confident his company can continue to grow this year and so is Daniel Stewart; the broker is pencilling in a further 11 per cent rise in pre-tax profits and EPS to £43m and 62p, respectively. On this basis, expect a dividend of 6.5p a share this year.

The valuation is also extreme when you use my balance sheet approach. Current assets of £129m exceed total liabilities of £20m more than six times over which means that Naibu's market value of £33.9m is covered more than three times by assets on the balance after deducting all liabilities.

On a bargain ratio of 3.22, offering a 10 per cent dividend yield, trading on a forward PE ratio of one and with net cash on its balance sheet exceeding its market capitalisation by £6m, Naibu is an automatic entry into this year's Bargain Shares Portfolio.

MAS should had added SGX listed S-Chip such as FerroChina, China Paper, China Sun, Sino Techfibre......long before they gone burst.

MAS should had added SGX listed S-Chip such as FerroChina, China Paper, China Sun, Sino Techfibre......long before they gone burst.