Urgent action needed to restore confidence to Singapore market

Urgent action needed to restore confidence to Singapore marketBy NS Nallakaruppan

3 October 2015

I read with interest your BT article

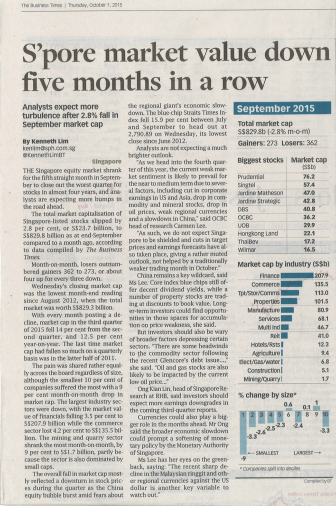

“Singapore market value down five months in a row” on Oct 1, 2015. It is worrying that despite all the IPO capital raising from 2012 to 2015, the Sept 30, 2015 closing market cap “was the lowest month-end reading since August 2012, when the total market was worth S$829.3 billion”.

There was also an earlier article headlined

“Singapore firms’ IPO proceeds fall to lowest since 2009” (BT, Sept 22) which stated that capital raising for the first nine months of 2015 stood at US$91.7 million, which is also a 95.6 per cent slump compared to the first nine months of last year.

All this worrying news clearly shows that our Singapore market is in a dire state. It is not only a cyclical issue but a real structural problem.

We, from the broking community, had written a letter with 1,225 signatories, dated Jan 15, 2015, to our Deputy Prime Minister then-Finance Minister Tharman Shanmugaratnam about the state of our moribund market and made an earnest plea to rebuild much-needed confidence. We had made several recommendations which we truly believed would have brought back vibrancy to our markets. Sadly, most of our recommendations have not been implemented and our markets have gone from bad to worse since then.

Subsequent to our letter, we have had a couple of meetings with MAS but sadly, nothing much concrete has come out so far. One of the issues we highlighted several times was the Minimum Trading Price policy, which has destroyed a lot of investors’ wealth and undermined gravely the markets’ confidence.

If a policy has failed, we must have the courage to admit it and take corrective action. If we continue with these types of flawed policies, we will end up in a situation like the one we are in now. Also, more importantly, we need policy makers who must have at least some years of market experience who can then really understand what the market really needs. Theoretical knowledge is not sufficient.

Our market is now akin to being in an intensive care unit. We need urgent attention and care, otherwise we will be history.

The investors and broking community were looking forward to the new SGX CEO and hoping that it would be the dawn of a new and promising era for our markets. Three months have come and gone and the hope is fading rapidly and reinforcing the notion that nothing much of significance will be undertaken.

Granted, it is only three months but looking at the state of our markets, we should be cognisant that we do not have the luxury of time. Many investors have given up hope. Now, even the broking community is fast losing confidence.

I have been in the industry for 21 years and haven’t seen our markets in such a pathetic state for such a prolonged period. As a Singaporean, I feel really sad that we have left our markets in such a sorry state and that nothing much has been done for such a long time. Our SMEs are having a tough time raising capital through our markets. Our investment banking community is also suffering and our economy is drastically affected.

We, the investors and the broking community, need to have a serious pow-wow session with our new Finance Minister, Heng Swee Keat, and come up with real practical solutions to rebuild the much-needed confidence of our markets.

I sincerely hope Mr Heng, together with the investors and the broking community, will re-establish the Singapore market as a top Asian gateway which Singaporeans will be proud of.

Singapore broker exodus seen quickening: Southeast Asia ~ 12 Mar 2014

Challenges of the Singapore stock-broking industryBy Edward Meow

9 Jun 2015

Recently, The Economist highlights an important trend that all in the financial services industry must take note if they expect to be around in even five years - the use of technology in the industry. In the local stock broking context, the invasion of borderless internet trading platforms would count as one. Besides the technology threat, there are also other challenges our local stock broking industry faces. I will surmise each of them as below:

1. Competition from non-SGX member internet trading platforms Our local stock-broking houses were slow in reacting to the threats posed by such foreign internet trading platforms who are not SGX members. Not only are these foreign internet platforms packed with features that our local stock-broking houses do not have, they also charge lower commission rates. It is only in the last few years that member stock-broking houses are spending money on improving their trading platform capabilities, whereas these competitive internet trading platforms had capabilities like stop-loss, trailing stop-loss etc, a decade ago. Furthermore, users can also trade soft & hard commodities, indices, forex, CFD, options - all on one platform. If they have to choose, our younger tech-savyy investors will likely choose such a more capable trading platform. Advisory trading (phone calling your stock-broker) will be used by the older generation who are less tech-savvy, and those who are too busy to key in their own trades. Over time, if our member stock broking houses do not "catch-up" on improving their trading platform to be on par, or even surpass that of these competitive trading platforms, we will all (both member stock-broking houses and their remisiers) lose out. The only solution has to be a holistic one involving all stakeholders of the industry - the SGX, the Government and the investors, both institutional and retail.

So, what should be the position of SGX, MAS and SIAS with regards to such non-SGX member internet trading platforms? It is a difficult position that SGX has, in that it cannot be seen to be stifling Singapore as a financial centre. With the current internet-age, it would indeed be a challenge and near impossible for SGX to keep out such internet trading platforms. The most effective way would be for SGX to work together with member broking houses to introduce trading platforms with better capabilities, and with more products like stock options & indices, and perhaps even commodities and forex. This will make their trading platforms more interesting to local investors and not lose out to the foreign competition. With trading platforms of better capabilities, member broking houses can, and should, compete for international business from other countries, just like what these alternative internet trading platforms are doing in Singapore. This will then ensure the survival of, especially, the local stock broking houses.

Regardless of the fact that we want to make Singapore a vibrant regional financial hub, it is important for MAS to ensure sufficient policing so that our Singaporean investors do not fall into any scams by rogue internet trading platforms. For the retail investors, SIAS needs to move beyond its role as champion to do some due diligence and intelligence work to sieve out and warn retail investors of any potential rogue internet trading platforms.

2. Singapore stock market vs Foreign stock marketIf you are trading in the US market, you would have noticed the flurry of activity in this market. There is no denying that the dynamism of foreign markets, like the US, or HK (which has the hinterland support of China), surpasses our Singapore market. With due respect to the Singapore companies listed on SGX, it is sad to say that none of these companies show the promise of innovation that US companies can. Singapore companies only grow organically or geographically, but none like the types of Apple or Microsoft, or recently Tesla, where their stock prices can grow multi-fold due to the value-added of their product innovation. Take Apple for example. During May/June 2007, it was about USD80. It then grew to nearly USD700 in June 2014. In June 2014, it exercised a stock-split of 1 into 7, which brought it to just above USD90. It has now gone up to about USD129. That is a 9 fold increase over a period of 8 years. Clients finding the Singapore market less exciting, are gradually moving to foreign markets, but unfortunately, with more of them slowly shifting to the use of the more capable foreign internet trading platforms mentioned above.

SGX cannot depend on the local stock investing community to attract premium companies to list in Singapore as this community is too small to have any impact. It has to find ways to make the Singapore listed companies accessible to a bigger population of investors worldwide, and not just within Singapore. With a bigger net cast, hopefully there will be more vibrancy, and therefore will attract better quality corporate listings. Otherwise, we will end up in a vicious cycle of low vibrancy, and therefore lower quality corporate listing, and vice-versa. The current initiative by SGX to link up with Taiwan, Japan, and rumoured talks of link up with the Chinese Exchanges, should hopefully move us in this positive direction.

3. Competition of brokerage fees from foreign marketsBrokerage fees in USA are generally lower than ours, and in some cases are fixed ($) on a per trade basis. This encourages big volume trading unlike percentage (%) based brokerage that is the norm in Singapore, where the higher the volume traded, higher is the brokerage cost. But of course, Singapore being a smaller market, it would be unwise for us to follow a fixed value ($) brokerage system as this will lead to lower revenue for the local broking fraternity. Nonetheless, the US brokerage system will certainly attract Singapore investors away from our local market which is seen as less dynamic and with less potential "multi-bagger" stocks. This shift is further aided by the borderless foreign internet trading platforms, together with their lower commission rate. Such a self-perpetuating situation will become worse, unless we break the vicious cycle of low vibrancy as stated in point 2 above. However, our top priority now should not be to implement a similar type of brokerage system as the USA. Only after we are able to attract more transaction volume into our Stock Echange should we then be able to consider fixed value ($) brokerage system.

4. Unhealthy competition between local broking housesWhile in the past, the fixed 1% brokerage fee was seen as unduly high, the current, supposedly, market dynamics of competitive brokerage fees is certainly unhealthy for the industry. Local broking houses and remisiers undercut each other. In the end, everybody loses. Revenue for the brokerage houses and remisiers is reduced. Demanding small clients may not get the service they want if the motivation of a remisier is to balance the time he has to spend on such clients versus the returns. The competition is not only between the broking houses, but sometimes also amongst remisiers of the same broking house. This can happen during roadshows, where a client may not reveal immediately that they already have a broker with the same broking house. In order to gain business, the remisier at the roadshow may unwittingly promise a lower commission, thus causing much unhappiness with the client who may think that his/her current broker has not been honest. Most clients expect their brokers to give them the lowest commission rate out-right, not knowing that they may have to meet certain volume criteria before such a low rate can be granted. For the local broking industry to survive, this kind of unhealthy competition has to stop. All stakeholders have to sit down and thrash out a scheme of fixed brokerage rate (%) that is fair to both investors and the stock-brokers. This should certainly not be seen as price-fixing as there are precedents in other cases/industries.

5. ConclusionThe Singapore stock broking industry is certainly facing many challenges. I would not venture to say that the industry has to innovate or reinvent itself, but rather it is downright very practical things that has to be done by the various responsible parties. Instead of working independently within their narrow scope of self-interest, all concerned parties have to work in consultation and in synergy of each other. If all parties are not united in the objective of improving the situation, the ultimate loser will be the Singapore stock-broking industry and its prominence in Asia, or even in S.E. Asia. China (together with Hong Kong) is already coming up very fast. Indonesia, with a domestic base of 260 million people, can outdo us in S.E. Asia if they put their act together better than us.

SGX has to push and take the lead in all the actions below:

i) Member (especially the local ones) stock broking houses has to invest on improving on the capabilities of their internet trading platforms to ensure that the tech-savvy younger generation investors do not move away to the more attractive non-SGX member foreign internet trading platforms. With their improved trading platforms, the local broking houses should then explore the possibility of attracting overseas investors to trade in the SIngapore stock market.

ii) SGX should explore to include more products that can be traded via the member broking houses' trading platform, e.g. stock options, indices, and possibly commodities futures and forex.

iii) SGX has to work hard on improving the vibrancy of our Singapore stock market through links with other regional and foreign stock exchanges. SGX and the member stock broking houses should also work towards making it easy and simple for overseas investors to trade in our Singapore stocks.

iv) All stakeholders should sit down to thrash out a fixed brokerage (%) scheme which would be fair to both investors and stock-brokers, and which would prevent the unhealthy undercutting. The value-add of remisiers has to be recognised as they not only act as "no basic salary" sales-force, but also bear complete risk of the clients that they acquired. Although there are efforts by some broking houses to introduce cash-deposit trading, a lot of clients still prefer to keep money in their own hands. The contra-players would also not see the advantage of depositing their money with the broking houses. In large countries like China or the USA, it may perhaps make sense to have cash-deposit trading as the population mobility is high, and the risk of bad-debts from open-credit trading in a large continent will be too high, but not in Singapore. The undercutting of commission resulted in very thin commission that has to be shared 60:40 between broking house and remisier respectively. This does not commensurate with the financial resources that the broking house needs for rentals, backroom support, trading platform improvements etc.It also does not commensurate with the high risk that remisiers have to bear in terms of bad-debts. We should unite to gain back our share lost to external forces, but sadly it seems that we are competing even more amongst ourselves for the slowly shrinking piece of cake taken away by such external forces.

NB: The opinion expressed here is the personal opinion of the author, and any mistake made is solely that of the author, and not that of the SRS or its Ex-Co.