|

|

Post by zuolun on Apr 12, 2014 15:50:10 GMT 7

|

|

|

|

Post by zuolun on Apr 12, 2014 16:16:49 GMT 7

|

|

|

|

Post by zuolun on Aug 22, 2014 15:56:42 GMT 7

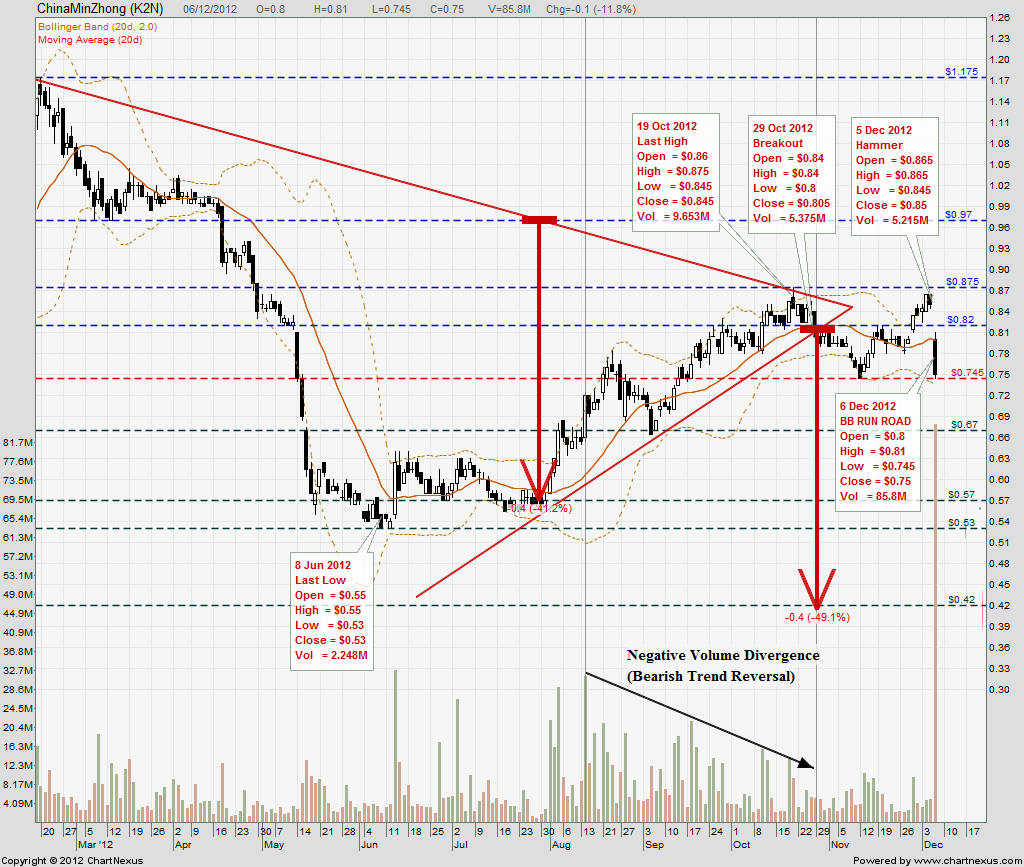

烂船还有三斤丁。 Junk ships still have scrap metals for recycling; Parkson to dispose KL Festival City Mall for RM349 million — 19 Aug 2014 Groupthink: Since the beginning of 2014, almost all the stock analysts in Malaysia issued SELL call on Parkson except Public Bank.  “机会总在绝望中诞生,在质疑中成长,在希望中成熟,在疯狂中死亡。” — 邓普顿 “机会总在绝望中诞生,在质疑中成长,在希望中成熟,在疯狂中死亡。” — 邓普顿John Templeton said “The time of maximum pessimism is the best time to buy and the time of maximum optimism is the best time to sell". "It makes sense that when most investors are bullish, asset valuations would be high, because everyone has already bought. The opposite is also true. When most investors are bearish, asset valuations are low, because everyone has already sold."

|

|

|

|

Post by zuolun on Nov 28, 2014 16:04:06 GMT 7

Ezion closed @ S$1.325 (-0.08, -5.7%) with 36,585,000 shares done on 28 Nov 2014. Most of the in-house stock analysts rated BUY on Ezion from 2 Jun to 12 Nov 2014 except Credit Suisse, Gerald Wong the only odd one who rated SELL 'Underperform' on Ezion TP S$1.80 on 9 July 2014, based on its last traded share price @ S$2.10 on 7 July 2014, then.  Why buy back Teras Conquest 4 within two years of selling it? Why buy back Teras Conquest 4 within two years of selling it? — 30 Aug 2014 Why is AusGroup Ltd paying S$55m to acquire net liabilities from Ezion? — 30 Aug 2014 M'sian billionaire Quek firms to buy 100m Ezion shares @ S$1.94 per share — 17 April 2014 Ezion's chart showed that major BBs initial run road's timing coincided with these 2 stock analysts' strong opposing views in mid-July 2014:

- DMG/OSK, LEE Yue Jer: Clearing the air on unwarranted negativity; upgrading to Top Buy

- Credit Suisse, Gerald Wong: A service rig is not a liftboat; Underperform TP S$1.80

This is the response from DMG/OSK Research Analyst LEE Yue Jer, after Credit Suisse Research initiated coverage of Ezion with an Underperformance rating and a price target of S$1.80. Ezion Holdings - Clearing the air on unwarranted negativity DMG/OSK upgrading to Top Buy15 July 2014 Analyst' s Response Here' s something I don' t do very often, but I've been convinced that the air needs to be cleared. Basically, a friendly competitor put out a sell initiation on Ezion yesterday (9 July, Wednesday) causing the share price to take a dive. However, a fund manager told me that Ezion' s management has called the report " factually inaccurate" , and I' m just going to point out some rather glaring issues. 1) A liftboat/service rig is NOT a drilling rigThe report states that new jackup rigs coming to the market could drive down dayrates and utilisation rates of " older assets" , and compares Ezion' s converted service rigs to these old assets. However, these are separate markets - a old jackup drilling rig commands USD100k/day dayrates, whereas Ezion' s service rigs generally get USD40-60k/day. In fact, I' d argue that lower prices for old drilling rigs is a GOOD thing for Ezion - they can pick up jackup platforms for conversions to service rigs at even more attractive prices. Remember that a jackup rig is for drilling, whereas liftboats/service rigs are generally for maintenance and accommodation services. So, comparing drilling rigs to service rigs is an apples-to-oranges comparison. 2) Ezion has begun calling all its units " service rigs"Even the newbuild ones! (This sort of demolishes the entire sell thesis, actually) Units 30 and 31 in their fleet, for Petronas and a " Southeast Asian" client, are actually newbuilds but Ezion has named the units " service rigs" . Management has confirmed that going forward, this is company policy and future units in their fleet will be referred to as " service rigs" . I' ve actually suggested to management to rename them all " service platforms" , to break the unintentional mental link with drilling rigs, but let' s see whether they take this up. 3) The working life of a converted service rig and a new liftboat should conservatively be 10 and 25 years respectively, inline with Ezion' s depreciation policyExperience shows that they can be used for even longer - Ezion has one service rig (Unit 16, Atlantic Esbjerg) which was converted 10 years ago and is still in operation to Maersk in the North Sea. Hercules Offshore has 3 liftboats, the Bonefish, Gemfish and Tapertail, which were built in 1978-79 (making them 35-36 years old today) and are still operational. Thus, the DCF model which was built using 5/15 year working lives for these assets is far too conservative, and has slashed the assets' working life by at least 50%. 4) More competition is to be welcomedCurrently, liftboats are only slowly making headway into the Asia Pacific market because of a lack of competition. For audit and governance purposes, oil majors require a proper tender process for each asset chartered in, and this is currently impossible without competitors. Additional players in the market would allow this process to be conducted, leading to wider acceptance of service rigs. Also, if the report is right in estimating that liftboat demand could grow by 80 units in the Asia Pacific, this actually indicates that demand is growing so fast that the market can absorb another two large players (Ezion currently has a fleet of 34 units including those on JV). Ezion' s first-mover advantage will stand it in good stead over the next few years, given the low market penetration of liftboats and the rising demand from an increasing number of fixed platforms in the region. 5) Mathematical inconsistencies 1: The report used a 15-year life for liftboats assuming 100% utilisation, and equated that to " an 83% utilisation over a useful life of 25 years" , and implies that this is a reasonable utilisation rate. Two issues - this assumption actually equates to 60% utilisation over 25 years. Second, Ezion' s units are generally fixed on 3 to 8 year contracts. A reasonable utilisation rate over the entire 30-year lifespan should actually fall in the range of 90-97%. 6) Mathematical inconsistencies 2: The report calculated a Valuation of USD992m for the service rigs. Note that Ezion has 15 service rigs on their book and 5 on 50% JV. So let' s call it 17.5 units' worth. Dividing USD992m by 17.5 units, the valuation of an average service rig is USD56.7m. However, let' s recall that most of Ezion' s service rigs actually COST USD60m to purchase and refurbish. Their valuation estimate somehow comes out to below the asset acquisition cost! If this were true I don' t think Ezion would be in business! Take a step backThe downside risk is now less than 10%. In the worst case scenario, if asset lives are halved, the company is worth SGD1.80 per share. The upside is more than 50% to my TP, and more than 40% to consensus TP. The risk-reward ratio is extremely favorable and the stock has pulled back 23% from the peak. The company is telling investors about the factual inconsistencies in the report, and doing some second order thinking, we can anticipate a reversal in sentiment once the air is cleared. It' s time to get in now while the market is panicking and asking questions after the selling. Source : DMG/OSK Research Analyst : LEE Yue Jer, CFA Ezion Holdings - A service rig is not a liftboat; Credit Suisse initiate coverage of Ezion with an UNDERPERFORM rating and a target price of S$1.80 — 9 July 2014  |

|

|

|

Post by zuolun on Feb 7, 2015 0:10:35 GMT 7

|

|