|

|

Post by zuolun on Jan 15, 2014 8:18:10 GMT 7

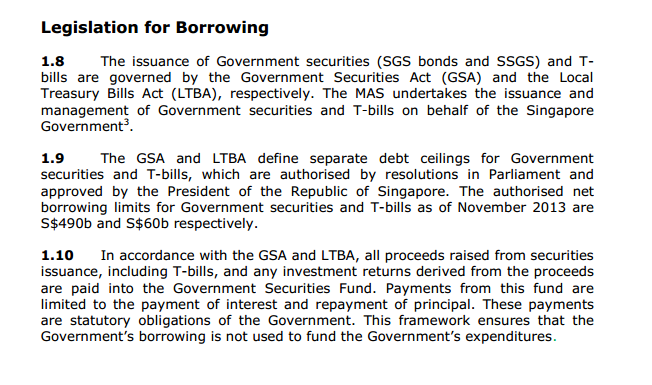

oldman, The article did not mention the issuance of government securities to S$490 billion. One of the issues that concerns many Singaporeans is that we are really unsure how much assets our Government truly owns. We know that the Singapore government borrows money internally to invest in these assets. As at Mar 2013, the Singapore government borrowed $396 billion (out of which $249 billion came from our CPF savings). When we talk about government reserves, we should subtract these borrowings from the total assets. As we are in the midst of a bull market, the assets will appear very healthy indeed. Good thing about the Singapore government loan is that there is little risk of recall as the bulk of it is from the CPF. Even if the market falters badly in a bear market, life still goes on. Hence, from this perspective, I too agree that Singapore is very different from Iceland. What is worrisome is the property bubble in Singapore. Many people's wealth are tied to properties. A collapse of the property bubble will have significant impact to our economy. In the last financial crisis, Singapore was relatively spared as the entry of foreigners helped our economy recover quicker. However, in the next financial crisis, I don't think we will get off so lightly..... app.mof.gov.sg/data/cmsresource/Public%20Debt%20Report%202013.pdfwww.gov.sg/government/web/content/govsg/classic/factually/Factually-310812-IsitfiscallysustainableforSingaporetohavesuchahighlevelofdebten.wikipedia.org/wiki/List_of_countries_by_public_debtoldman, "When we talk about government reserves, we should subtract these borrowings from the total assets"... haha...you can literally read my mind.  Official Foreign Reserves as at 7 Jan 2014As at Nov 2013, the authorised net borrowing limits for Government securities and T-bills are S$490b and S$60b respectively: Official Foreign Reserves as at 7 Jan 2014As at Nov 2013, the authorised net borrowing limits for Government securities and T-bills are S$490b and S$60b respectively: |

|

|

|

Post by oldman on Jan 15, 2014 9:00:09 GMT 7

zuolun, this reminds me of many of the articles in our local papers. Whenever it features a person, it highlights the assets of the person without mentioning anything about their liabilities. So, a person can own several houses and look financially wealthy. What makes me laugh even louder is that some can even list their insurance policies as assets. Yes, sounds great if you have $2 mil worth of insurance policies..... without mentioning that this may only have costed you a hundred dollars of premium a month.... and this money will never be yours unless you continue paying higher and higher premiums until you die.... it is then too late to count this as your asset!

|

|

|

|

Post by zuolun on Jan 15, 2014 10:03:27 GMT 7

|

|

|

|

Post by oldman on Jan 15, 2014 10:36:02 GMT 7

Yes, as Warren Buffett so aptly puts it: Only when the tide goes out do you discover who's been swimming naked. I think we are going to see lots of naked people soon. |

|

|

|

Post by zuolun on Jan 15, 2014 10:43:09 GMT 7

Yes, as Warren Buffett so aptly puts it: Only when the tide goes out do you discover who's been swimming naked. I think we are going to see lots of naked people soon. — Oct 2003 The Casualties: Many of the first category can be found among companies that filed for protection under Section 176 of the Companies Act by mid-July 1998. Most notable was Time Engineering, a subsidiary of Renong, the largest Malay-owned conglomerate in Malaysia. The Chinese-owned or controlled companies that filed for protection include shipbuilder Westmont Industries, financial services firm MBf, appliance maker Kuala Lumpur Industries, property developer Wembley Industries, and stockbroker Uniphoenix. Other firms had their debts taken over by Danaharta Nasional. As of December 2000, 32 out of 76 companies placed under Danaharta special administrators were identifiably Chinese-owned. Several of these had been high profile in the pre-crisis period: Malaysia Electric Corporation, Jupiter Securities, Sin Heng Chan (Malaya), Instantgreen Corporation, Seng Hup Corporation, Timbermaster Industries, Woo Hing Brothers (Malaya), Bescorp Industries, Sri Hartamas, Rahman Hydraulic, and Kuala Lumpur Industries Holdings. Most of the companies or individuals who fell into immediate and serious trouble were those with heavy debt. In the pre-crisis period, a number of businessmen had taken huge loans to acquire properties or listed companies. Pledging shares of their own firms, some of which had price-earnings (PE) ratios of 18, to acquire companies with PE ratios of 6, seemed an intelligent way to expand and diversify. In a period when loans were easy to obtain, some investors then used the acquired shares to make further acquisitions. These corporate raiders bought up sizeable numbers of shares of targeted companies with the aim of driving up share prices before disposing of them at a huge profit. Two businessmen known for ambitious acquisitions and takeovers who later came to grief are Soh Chee Wen and Joseph Chong Chek Ah. Soh began with the takeover of a company called Autoways Holdings. He subsequently acquired, among others, the stockbrokerage firms Uniphoenix and Halim Securities and the manufacturer Perstima (involved in the production and sale of electrolytic tin plate for the canning industry), which he later sold off. But Soh became heavily indebted and his companies were eventually placed under Danaharta Nasional’s special administrator. Like the businesses acquired by Soh Chee Wen, some of those bought by Joseph Chong were considered healthy, such as the publicly-listed Wing Tiek Holdings and Westmont Industries. Other of Chong’s companies included Westmont Land, later re-named Techno Asia Holdings, and Prima Mould Manufacturing. Chong took over Sabah Shipyard and proceeded to acquire the National Steel Corporation of the Philippines. But in mid-1997, talk began of major financial problems at Westmont Industries. According to a report in The Edge (16 November 1998), an investigative audit revised Westmont’s accounts to indicate a huge loss instead of profits for the 1996 financial year. The crisis greatly aggravated Chong’s problems. As of December 1997, Westmont’s losses amounted to RM651.4 million and liabilities totaled RM883.7 million, including short-term and other debt of more than RM400 million. Westmont became the first of 30 publicly-listed companies to file for protection under Section 176. Chong’s Wing Tiek Holdings, which had accumulated losses of RM200 million, was also forced to restructure. Chong is no longer associated with the two companies. Perhaps the most spectacular corporate fall due in part to overexpansion and the crisis was that of Lim Thian Kiat (better known as T.K. Lim) of Multi-Purpose Holdings. Multi-Purpose Holdings was once linked to the Malaysian Chinese Association (MCA), a senior member of the ruling Barisan Nasional (BN) coalition. Lim’s family had used its own company, Kamunting, to gain control of MPH during the 1986 recession, however, after the firm went on a massive acquisition binge and subsequently suffered heavy losses. Lim belonged to the new generation of young and ambitious corporate players, and under his control Multi-Purpose Holdings expanded further. Lim also had political connections and was reportedly close to Anwar Ibrahim, Malaysia’s Deputy Prime Minister between 1993 and 1998. The heavily-diversified Multi-Purpose Holdings group included Multi-Purpose Bank, Malayan Plantations, property developer Bandar Raya Developments, and the gaming firm Magnum Corporation. By 1997, Multi-Purpose Holdings had incurred debts amounting to RM2.2 billion, and Lim’s Hong Kong investments were also said to have suffered heavily from falling property values. |

|

|

|

Post by zuolun on Jan 15, 2014 11:42:24 GMT 7

|

|

|

|

Post by oldman on Jan 16, 2014 16:16:18 GMT 7

|

|

|

|

Post by stockpicker on Jan 16, 2014 16:27:27 GMT 7

The foreigners look at our property bubbles and started to agree that we are set for Icelandic style problem.. globaleconomicanalysis.blogspot.sg/2014/01/singapore-set-for-icelandic-style.html?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed:+MishsGlobalEconomicTrendAnalysis+(Mish's+Global+Economic+Trend+Analysis) In a way, they are not totally wrong as property bubble can easily lead to credit crisis when housing prices collapse, leaving the banks holding all the unwanted property assets.. this was how US's economy got into such credit crisis and the US Government has to bail them out. The question is whether our banks are over-stretched, giving out housing loans to customers who barely able to pay back the interest. Just have a quick look at the fundamentals of the local banks and found that they are not altogether equal in terms of Long Term Debts/Net Asset ratios. one of the 3 big banks has Long Term Debts over 3 times the Net Assets which is somewhat worrisome. BTW, the author of the icelandic report, Mr. Colombo, tried to rebut MAS's reply by saying that "It's Not A Bubble Until It's Officially Denied". It appears that the author offered nothing new except this time, saying that Singapore banks are heavily invested in China and SEA and would go down if these economies were in trouble. www.forbes.com/sites/jessecolombo/2014/01/16/its-not-a-bubble-until-its-officially-denied-singapore-edition/2/One interesting point is that the author related Singapore's low interest environment to US Fed's low interest policy and correlated that Singapore's bubble would not burst so soon.. not until US stops its low interest rate policy in 2017..BTW, it is very likely that Singapore's bubbles will burst only after US's bubbles have bursted before 2017.. LOL |

|

|

|

Post by oldman on Jan 16, 2014 16:59:59 GMT 7

|

|

|

|

Post by candy188 on Jan 16, 2014 17:37:12 GMT 7

Long Term Debt to Net Assets is an interesting ratio to utilise.  Long term Debt to Total Asset Ratio is the commonly used solvency ratio Long term Debt to Total Asset Ratio is the commonly used solvency ratio utilised to gauge whether the company assets is financed by debt lasting more than 1 year. The foreigners look at our property bubbles and started to agree that we are set for Icelandic style problem.. globaleconomicanalysis.blogspot.sg/2014/01/singapore-set-for-icelandic-style.html?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed:+MishsGlobalEconomicTrendAnalysis+(Mish's+Global+Economic+Trend+Analysis) In a way, they are not totally wrong as property bubble can easily lead to credit crisis when housing prices collapse, leaving the banks holding all the unwanted property assets.. this was how US's economy got into such credit crisis and the US Government has to bail them out.  The question is whether our banks are over-stretched, giving out housing loans to customers who barely able to pay back the interest. The question is whether our banks are over-stretched, giving out housing loans to customers who barely able to pay back the interest.

Just have a quick look at the fundamentals of the local banks and found that they are not altogether equal in terms of Long Term Debts/Net Asset ratios. one of the 3 big banks has Long Term Debts over 3 times the Net Assets which is somewhat worrisome.

BTW, the author of the icelandic report, Mr. Colombo, tried to rebut MAS's reply by saying that "It's Not A Bubble Until It's Officially Denied". It appears that the author offered nothing new except this time, saying that Singapore banks are heavily invested in China and SEA and would go down if these economies were in trouble.www.forbes.com/sites/jessecolombo/2014/01/16/its-not-a-bubble-until-its-officially-denied-singapore-edition/2/ One interesting point is that the author related Singapore's low interest environment to US Fed's low interest policy and correlated that Singapore's bubble would not burst so soon.. not until US stops its low interest rate policy in 2017..BTW, it is very likely that Singapore's bubbles will burst only after US's bubbles have burst before 2017.. LOL

|

|

|

|

Post by zuolun on Jan 16, 2014 22:53:32 GMT 7

|

|

|

|

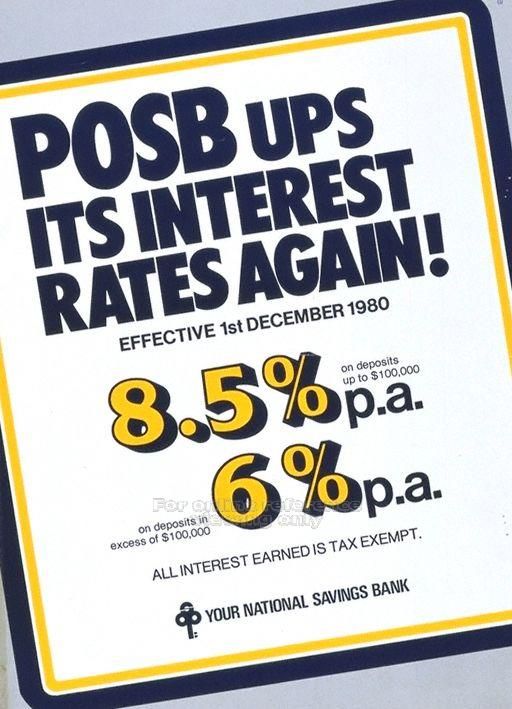

Post by oldman on Jan 17, 2014 3:32:45 GMT 7

Wow, what an interest rate! Never knew that! With such an interest rate, I would have kept my money in the bank! My simple mind tells me that the easiest way to defuse a bubble is simply to slowly increase the interest rate.... after all, the root of the problem is the interest rate. But I doubt any government is daring enough to go against the herd..... |

|

|

|

Post by zuolun on Jan 17, 2014 8:37:22 GMT 7

Wow, what an interest rate! Never knew that! With such an interest rate, I would have kept my money in the bank! My simple mind tells me that the easiest way to defuse a bubble is simply to slowly increase the interest rate.... after all, the root of the problem is the interest rate. But I doubt any government is daring enough to go against the herd..... oldman, It's amazing that you could read my mind again!  Yes, the root cause is long-term extremely low interest rate! |

|

|

|

Post by oldman on Jan 30, 2014 8:33:20 GMT 7

With the US tapering in progress, we have to brace ourselves for higher interest rates in 2014. The period of easy money may be coming to an end. Individual countries will do whatever in their powers to stabilise their currencies and a quick way is to increase their interest rates.

This will then affect the property markets. Businesses will find the going tougher. Those who expanded too quickly on borrowed money will feel the heat. Best to take more profits along the way.

I don't think the markets will come crashing down but I think 2014 will not be a good year for the stock and property market as companies face the issue of increasing interest rates and subdued demand worldwide. We are getting closer to the midnight hour.

|

|

|

|

Post by zuolun on Jan 30, 2014 9:03:55 GMT 7

With the US tapering in progress, we have to brace ourselves for higher interest rates in 2014. The period of easy money may be coming to an end. Individual countries will do whatever in their powers to stabilise their currencies and a quick way is to increase their interest rates. This will then affect the property markets. Businesses will find the going tougher. Those who expanded too quickly on borrowed money will feel the heat. Best to take more profits along the way. I don't think the markets will come crashing down but I think 2014 will not be a good year for the stock and property market as companies face the issue of increasing interest rates and subdued demand worldwide. We are getting closer to the midnight hour. oldman, Properties and bank stocks are the 2 major pillars of the S'pore economy and also the last line of defense of the STI @ 2775 points. 隔岸观火,静观其变。Everything is well prepared; stand on the sideline, wait patiently to profit from the panic.  This is the best forum which I could pick up many new things and learn fast! This is the best forum which I could pick up many new things and learn fast!

Chart is similar to a compass if one knows how to use it correctly

When the stock markets of other Asian markets plunged big time in end-May to end-Jun 2013, they reflected the mass capitulation by Foreign Funds. As the S$/US$ has appreciated by 15% since 2009 and S'pore had underperformed other ASEAN countries in term of % GDP growth 2012, Foreign Funds were mostly absent at end-Dec 2012. So the impact of capitulation by Foreign Funds on the STI was not great as compared to other Asian markets. Thus, the tight trading range bet. 3167 - 3328 points in the 1H2013 suggested that the STI has been supported mainly by local Fund managers since the beginning of 2013. These local Fund managers only support the 2 major pillars of the S'pore economy; the properties and bank stocks. But properties and bank stocks are sensitive to sharp interest rates spikes which will negatively affect their qtrly earnings — that's a fundamental and inverse change. So if you're the local Fund managers with portfolios heavy on S'pore properties and bank stocks, would you consider increasing or paring down the 2 main categories of stocks at current prices which had corrected at the most 10%? Southeast Asia Bears Brunt of Market Chaos — 20 Jun 2013 |

|

Yes, the root cause is long-term extremely low interest rate!

Yes, the root cause is long-term extremely low interest rate!