|

|

Post by zuolun on Dec 8, 2014 11:39:00 GMT 7

|

|

|

|

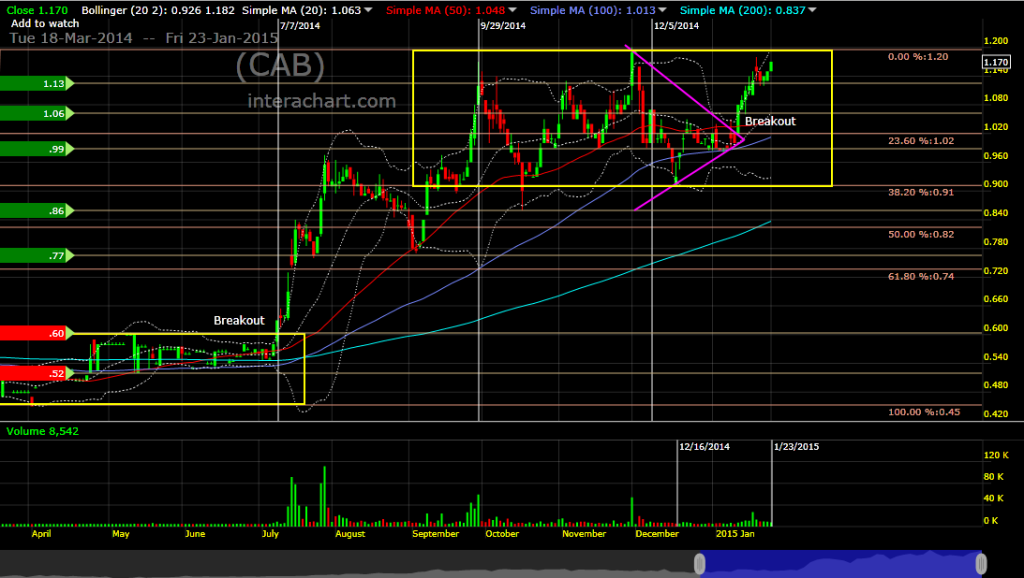

Post by zuolun on Jan 26, 2015 6:34:37 GMT 7

CAB — Trading in an upward sloping channel, Interim TP RM 1.20, Next TP RM 1.34CAB closed with a white marubozu @ RM1.17 (+0.02, +1.7%) with 850 lots done on 23 Jan 2015. Immediate support @ RM1.13, immediate resistance @ RM1.20.

|

|

|

|

Post by zuolun on Mar 1, 2015 10:57:49 GMT 7

|

|

|

|

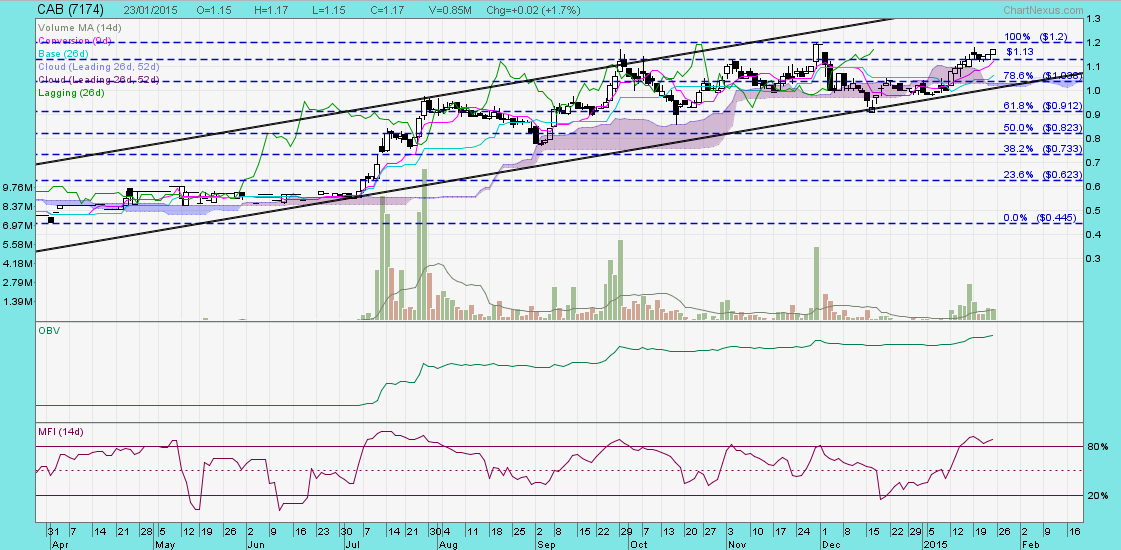

Post by zuolun on Mar 4, 2015 7:25:00 GMT 7

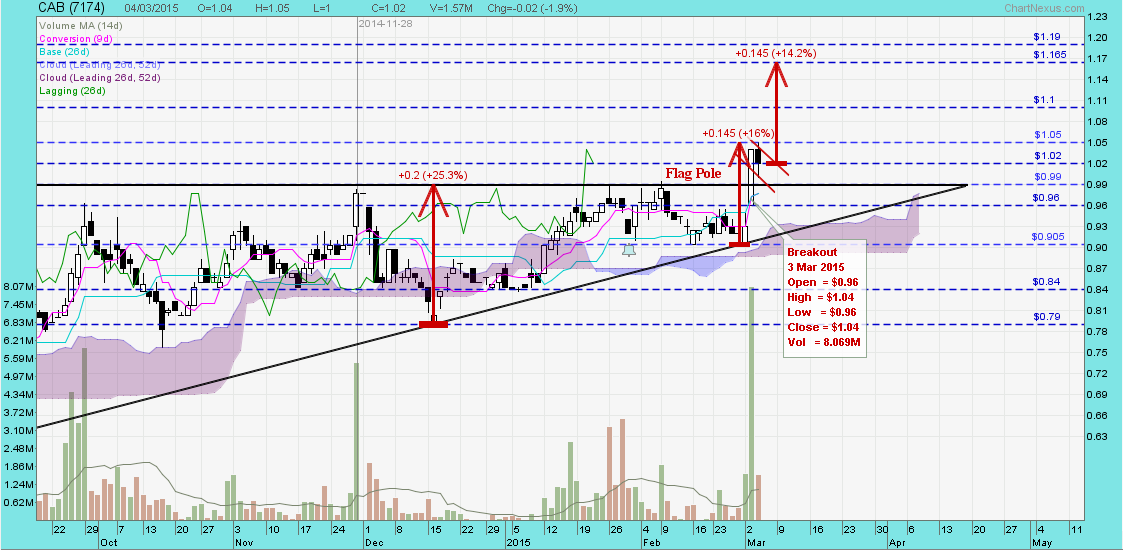

CAB is an example of an uptrend stock with a very unique chart pattern ~ 狼齿或犬齿形态 (Dog Teeth/Wolf Pattern) (Re Vibrant's chart pattern dated 23 Jan 2013.)CAB — Trading in an upward sloping channel, Interim TP RM 1.17, Next TP RM 1.23CAB closed with a long white marubozu @ RM1.04 (+0.11, +11.8%) with extremely high volume done at 8.07m shares on 3 Mar 2015. Immediate support @ RM0.99, immediate resistance @ RM1.10.  Adding CAB into the thematic and growth portfolios Adding CAB into the thematic and growth portfolios ~ 3 Mar 2015 CAB净利前景看俏 料保留现金不派息 ~ 3 Mar 2015 積極擴充前景佳 CAB機構地庫價值待釋放 ~ 3 Mar 2015 凭单专栏:回报率高达116% 卖母股转持CAB-WA ~ 23 Feb 2015  CAB Cakaran Corporation - Fattening Up CAB Cakaran Corporation - Fattening UpBy Kenanga Research 3 Mar 2015 · Another interesting poultry stock to watch. After we featured poultry player PW Consolidated Bhd (Trading Buy; FV: RM1.58) in mid-Jan which drew some buying interesting, today we introduce yet another poultry stock, which is also based in Mainland Penang, CAB Cakaran Corp Bhd (CAB). Unlike PW which operates its broiler farming business only in the north, CAB has farms throughout the Peninsular. It has a larger capacity of 3.6m birds/month currently and RM670m annual turnover compared to PW’s 2m birds/month capacity and RM250m annual turnover. In addition, CAB has transformed in the past 2-3 years, gaining in terms of stock price as well as improved earnings profiles since the second generation took over the helm. · An integrated poultry producer. Currently, CAB has 10 breeder farms and 117 broiler farms throughout the Peninsular Malaysia. These farms are grouped under the integrated poultry farming and processing unit contributes three-quarters to the group’s revenue. As livestock earnings could be erratic, CAB is also involved in downstream business particularly the value-added food products like cooked chicken and this segment contributes c.6% of group’s topline with profit margin almost double that of the livestock business. Under its supermarket division, CAB currently operates eight outlets under the brandname of Jaya Garing mainly in East Coast. Despite making up less than 20% group’s revenue, earnings contribution from this segment is still insignificant at the moment. The last business segment is marine products which contributed less than 1% of the group’s turnover. · From Malaysia to the Lion City. With the acquisition of 51% stake worth SGD7.4m in Tong Huat Poultry Processing Factory Pte Ltd (TH), which was announced in last October, CAB will gain immediate presence in Singapore as TH is one of the seven licensed slaughter houses there with market share of 15%. Upon completion of the acquisition which is expected in April, TH would add another capacity of 550k-600k birds/month to CAB capacity. In addition, CAB will spend RM10m-RM20m capex this year to expand its breeder farms in Juru, Penang and Padang Meha, Kedah. With the acquisition and expansion plans, CAB is able to achieve 5m birds/month capacity by year-end. · Value unlocking for land assets. CAB has been acquiring parcels of lands mainly in Mainland Penang, such as Bukit Mertajam and Batu Kawan, more than 20 years ago with the purpose for farming expansion. However, with the rapid development in Mainland Penang, today these lands are no longer suitable for farming activities as there are close to housing estates, which may cause environmental issue. As such, CAB is now considering ways to unlock these lands value either through sale of land or to embark on property development via JV. In its latest FY14 Annual Report, a total of RM64.8m worth of investment properties were reported of which half are vacant land while the rest are being leased out. · Strong earnings expected. Last Friday, CAB reported a net loss of RM3.2m in 1Q15 from net profit of RM1.2m in 1Q14, due mainly to the integrated poultry farming and processing unit turning to losses as ASP dropped to RM3.64/kg for broilers from RM4.30/kg previously. The lower ASP in 1Q15 was mainly due to the mega flood in the East Coast which caused oversupply of broilers. However, this is a one-off event as currently the broiler price is back to RM5.00/kg with breakeven level of c.RM4.00/kg. We project a net profit of RM13.8m in FY15, from FY14’s RM11.2m, on the assumption of 4m birds/month capacity while a bigger jump in FY16 to RM20.2m with 5m birds/month capacity. Adjusting to CY basis, CY15 net profit is projected at RM18.9m. · New Trading Buy with FV of RM1.29/share. Although earnings are set to be better, no DPS is expected at least for FY15 given its expansion plan. However, this is a growth stock which looks beyond dividend income. As CAB is bigger than PW, we believe CAB should be valued at CY15 9x PER (10% discount to the FBMSC’s 10x) as opposed to PW’s 8x (20% discount to the FBMSC valuation). Thus, CAB is valued at RM1.29/share and we advocate a Trading Buy rating on the stock. |

|

|

|

Post by sptl123 on Mar 4, 2015 8:33:38 GMT 7

Bro Zuolun, It is very good to see this up-trend stock. Hope you could post more of such up-trend stocks for us to study/ learn & appreciate and may be getting a little pocket money too  . CAB is an example of an uptrend stock with a very unique chart pattern ~ 狼齿或犬齿形态 (Dog Teeth/Wolf Pattern) (Re Vibrant's chart pattern dated 23 Jan 2013.)CAB — Trading in an upward sloping channel, Interim TP RM 1.17, Next TP RM 1.23CAB closed with a long white marubozu @ RM1.04 (+0.11, +11.8%) with extremely high volume done at 8.07m shares on 3 Mar 2015. Immediate support @ RM0.99, immediate resistance @ RM1.10. Adding CAB into the thematic and growth portfolios ~ 3 Mar 2015 CAB净利前景看俏 料保留现金不派息 ~ 3 Mar 2015 積極擴充前景佳 CAB機構地庫價值待釋放 ~ 3 Mar 2015 凭单专栏:回报率高达116% 卖母股转持CAB-WA ~ 23 Feb 2015 CAB Cakaran Corporation - Fattening UpBy Kenanga Research 3 Mar 2015 · Another interesting poultry stock to watch. After we featured poultry player PW Consolidated Bhd (Trading Buy; FV: RM1.58) in mid-Jan which drew some buying interesting, today we introduce yet another poultry stock, which is also based in Mainland Penang, CAB Cakaran Corp Bhd (CAB). Unlike PW which operates its broiler farming business only in the north, CAB has farms throughout the Peninsular. It has a larger capacity of 3.6m birds/month currently and RM670m annual turnover compared to PW’s 2m birds/month capacity and RM250m annual turnover. In addition, CAB has transformed in the past 2-3 years, gaining in terms of stock price as well as improved earnings profiles since the second generation took over the helm. · An integrated poultry producer. Currently, CAB has 10 breeder farms and 117 broiler farms throughout the Peninsular Malaysia. These farms are grouped under the integrated poultry farming and processing unit contributes three-quarters to the group’s revenue. As livestock earnings could be erratic, CAB is also involved in downstream business particularly the value-added food products like cooked chicken and this segment contributes c.6% of group’s topline with profit margin almost double that of the livestock business. Under its supermarket division, CAB currently operates eight outlets under the brandname of Jaya Garing mainly in East Coast. Despite making up less than 20% group’s revenue, earnings contribution from this segment is still insignificant at the moment. The last business segment is marine products which contributed less than 1% of the group’s turnover. · From Malaysia to the Lion City. With the acquisition of 51% stake worth SGD7.4m in Tong Huat Poultry Processing Factory Pte Ltd (TH), which was announced in last October, CAB will gain immediate presence in Singapore as TH is one of the seven licensed slaughter houses there with market share of 15%. Upon completion of the acquisition which is expected in April, TH would add another capacity of 550k-600k birds/month to CAB capacity. In addition, CAB will spend RM10m-RM20m capex this year to expand its breeder farms in Juru, Penang and Padang Meha, Kedah. With the acquisition and expansion plans, CAB is able to achieve 5m birds/month capacity by year-end. · Value unlocking for land assets. CAB has been acquiring parcels of lands mainly in Mainland Penang, such as Bukit Mertajam and Batu Kawan, more than 20 years ago with the purpose for farming expansion. However, with the rapid development in Mainland Penang, today these lands are no longer suitable for farming activities as there are close to housing estates, which may cause environmental issue. As such, CAB is now considering ways to unlock these lands value either through sale of land or to embark on property development via JV. In its latest FY14 Annual Report, a total of RM64.8m worth of investment properties were reported of which half are vacant land while the rest are being leased out. · Strong earnings expected. Last Friday, CAB reported a net loss of RM3.2m in 1Q15 from net profit of RM1.2m in 1Q14, due mainly to the integrated poultry farming and processing unit turning to losses as ASP dropped to RM3.64/kg for broilers from RM4.30/kg previously. The lower ASP in 1Q15 was mainly due to the mega flood in the East Coast which caused oversupply of broilers. However, this is a one-off event as currently the broiler price is back to RM5.00/kg with breakeven level of c.RM4.00/kg. We project a net profit of RM13.8m in FY15, from FY14’s RM11.2m, on the assumption of 4m birds/month capacity while a bigger jump in FY16 to RM20.2m with 5m birds/month capacity. Adjusting to CY basis, CY15 net profit is projected at RM18.9m. · New Trading Buy with FV of RM1.29/share. Although earnings are set to be better, no DPS is expected at least for FY15 given its expansion plan. However, this is a growth stock which looks beyond dividend income. As CAB is bigger than PW, we believe CAB should be valued at CY15 9x PER (10% discount to the FBMSC’s 10x) as opposed to PW’s 8x (20% discount to the FBMSC valuation). Thus, CAB is valued at RM1.29/share and we advocate a Trading Buy rating on the stock. |

|

|

|

Post by zuolun on Mar 4, 2015 14:29:52 GMT 7

Bro Zuolun, It is very good to see this up-trend stock. Hope you could post more of such up-trend stocks for us to study/ learn & appreciate and may be getting a little pocket money too . , Based on the CAB's EW chart pattern dated 5 Dec 2014, prior to the ex-warrant, the stock is biased to the upside. I'm vested in CAB (mothershare in-the-money) and had received the 1-for-2 bonus issue of warrant, WA200208 (babyshare in-the-money). 凭单专栏:回报率高达116% 卖母股转持CAB-WA CAB Cakaran (weekly) — Ascending Broadening Wedge chart pattern, biased to the upside  |

|

|

|

Post by zuolun on Mar 5, 2015 16:39:02 GMT 7

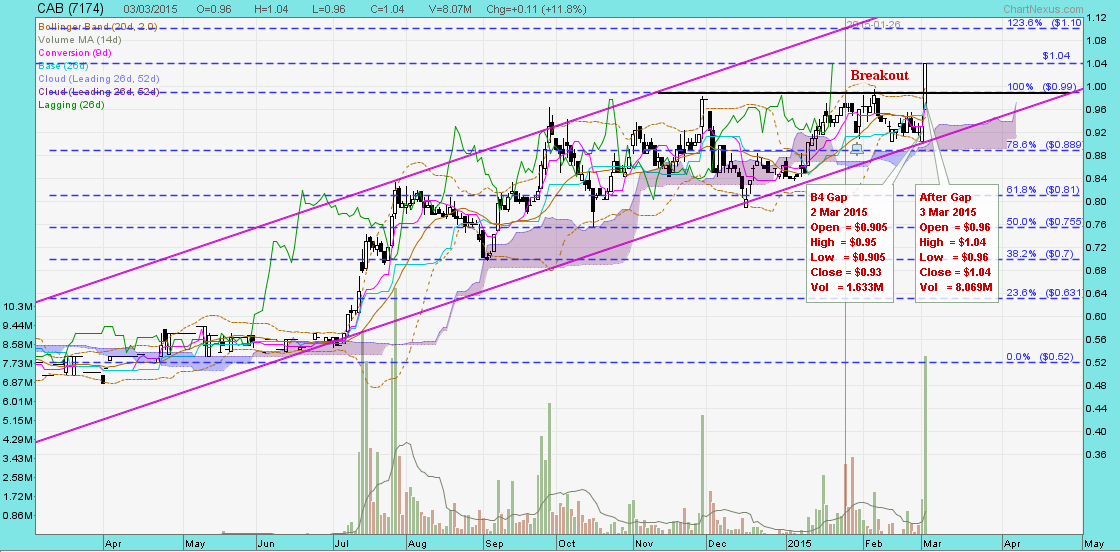

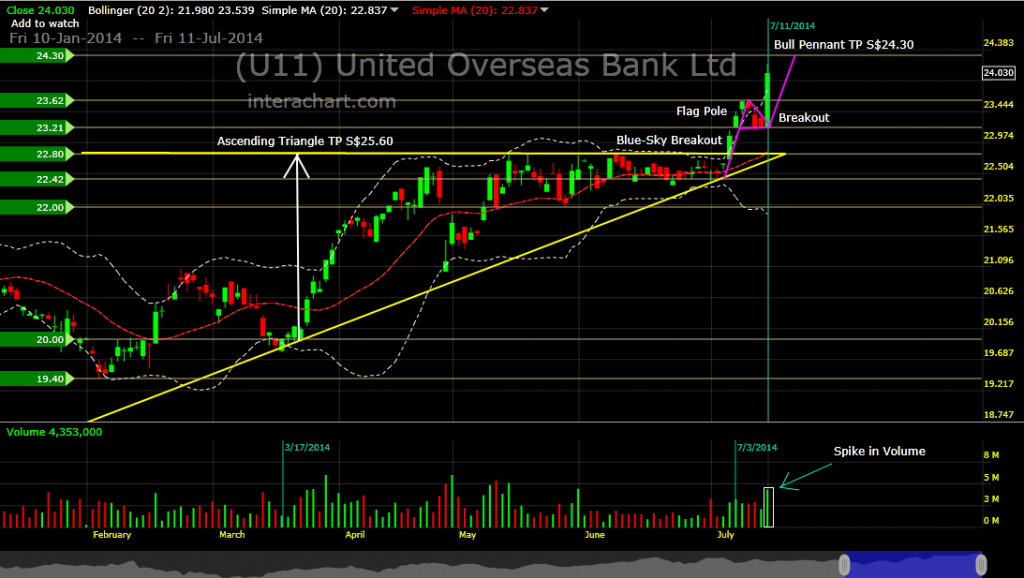

sptl123, CAB's bullish setup is similar to UOB's chart pattern dated 3 July 2014. The price action and volume suggest a consolidation, i.e. range trading bet. RM1.00 to 1.05 is +ve. The key resistance-turned-support @ RM0.99 now serves as a floor, immediate support @ RM0.96, strong support @ RM0.905, immediate resistance @ RM1.10. If RM1.05 is broken convincingly with extremely high volume (> 2X of 8m shares), the potential bull flag breakout will be fast and furious. Alternatively, a break below @ RM0.96 suggests a falsebreak on 3 Mar 2015, i.e. the bull flag formation is invalid. CAB closed unchanged @ RM1.02 with 501,700 shares done on 5 Mar 2015.   CAB ~ Potential bull flag formation, Interim TP RM 1.17, Next TP RM 1.23 CAB ~ Potential bull flag formation, Interim TP RM 1.17, Next TP RM 1.23

|

|

|

|

Post by zuolun on Mar 10, 2015 9:28:46 GMT 7

CAB hit high of RM1.14 and traded @ RM1.11 (+0.03, +2.78%) with 2.82m shares done on 10 Mar 2015 at 10.25am. CAB — Trading in an upward sloping channel, Interim TP RM 1.17, Next TP RM 1.23 |

|

|

|

Post by sptl123 on Mar 10, 2015 9:40:08 GMT 7

Thank you Bro Zuolun for this yet another uptrend stock. Followed, Vested and in-the-money too  CAB hit high of RM1.14 and traded @ RM1.11 (+0.03, +2.78%) with 2.82m shares done on 10 Mar 2015 at 10.25am. CAB — Trading in an upward sloping channel, Interim TP RM 1.17, Next TP RM 1.23 |

|

|

|

Post by zuolun on Mar 10, 2015 10:48:39 GMT 7

Thank you Bro Zuolun for this yet another uptrend stock. Followed, Vested and in-the-money too I never recommend what stocks to long or short in this forum, if you follow me, it's your decision, your money; no one points a gun at you to buy or sell.   |

|

|

|

Post by zuolun on Mar 10, 2015 14:46:22 GMT 7

Boon from lower commodity prices ~ 7 Mar 2015 CAB Cakaran Corp Bhd: Major shareholder's holdings at 54% CAB Cakaran is about to make its entry into Singapore. Last October, it entered into a heads of agreement to acquire a 51% stake in Tong Huat Poultry Processing Factory Pte Ltd for RM19.2mil. Tong Huat is one of seven licensed chicken slaughtering houses in Singapore. The proposed acquisition would be completed by the second quarter of this year, and would add some S$1.02mil (RM2.75mil) to CAB Cakaran’s full-year bottom-line in financial year 2016. The additional RM2.75mil would be a 24.66% increase in CAB Cakaran’s 2014 earnings. The company recorded a net profit of RM11.17mil for its financial year ended Sept 30, 2014. “The poultry stocks have always traded at single-digit price earnings because of the earnings volatility. This is mainly due to the volatility both in the feedstock as well as the market price of eggs and chicken,” explains one consumer analyst. Sixty-five per cent of a poultry company’s production cost is made up of the feed cost - which is soybean meal and corn. CAB Cakaran is one of the biggest poultry companies in Malaysia. It is one of the rare companies that saw its share price double in 2014. On a year-to-date basis, the stock is up 30.6%, taking into account the bonus issue of warrants. The company will start to give out dividends next year. It is presently trading at a historical PE ratio of 10 times and at a price-to-book value (P/BV) of 0.87 times. Both CAB Cakaran and PW Consolidated are based in the north, although CAB Cakaran has farms throughout the Peninsula. CAB Cakaran has a capacity of 3.6 million birds per month currently and an annual turnover of RM670mil. The company is looking to increase its capacity to five million birds a month by year-end. It has 10 breeder farms and 117 broiler farms in Peninsular Malaysia. It is also involved in the downstream business, particularly value-added food products like cooked chicken.

|

|

|

|

Post by zuolun on Mar 11, 2015 5:28:18 GMT 7

|

|

|

|

Post by zuolun on Mar 16, 2015 14:52:58 GMT 7

CAB traded @ RM1.11 (+0.03, +2.78%) with 1.9m shares done on 16 Mar 2015 at 3.30pm. CAB — Trading in an upward sloping channel, Interim TP RM 1.17, Next TP RM 1.23  |

|

|

|

Post by zuolun on Mar 17, 2015 9:49:11 GMT 7

CAB hit low of RM1.09 and traded @ RM1.13 (+0.04, +3.67%) with 1.51m shares done on 17 Mar 2015 at 10.45am.   价钱的移动是庄弄的,还是投资者弄的你更要懂得看,搞错对象就会操错方向,方向错了,就没了...Technical Analysis on CAB and Yanlord — Price action and volumeCAB's long white candle (breakup with high volume) signaled a big mad crowd running into a house where someone inside is distributing gold bars, FOC. Yanlord's long black candle (breakdown with high volume) signaled a big mad crowd running out of a house which is on fire.  |

|

|

|

Post by zuolun on Mar 21, 2015 11:12:55 GMT 7

sptl123, - CAB-WA200208 closed -ve on 20 Mar 2015.

- Lock-in some profit fast should the mother share break the support @ RM1.10 as price may pull back, further down.

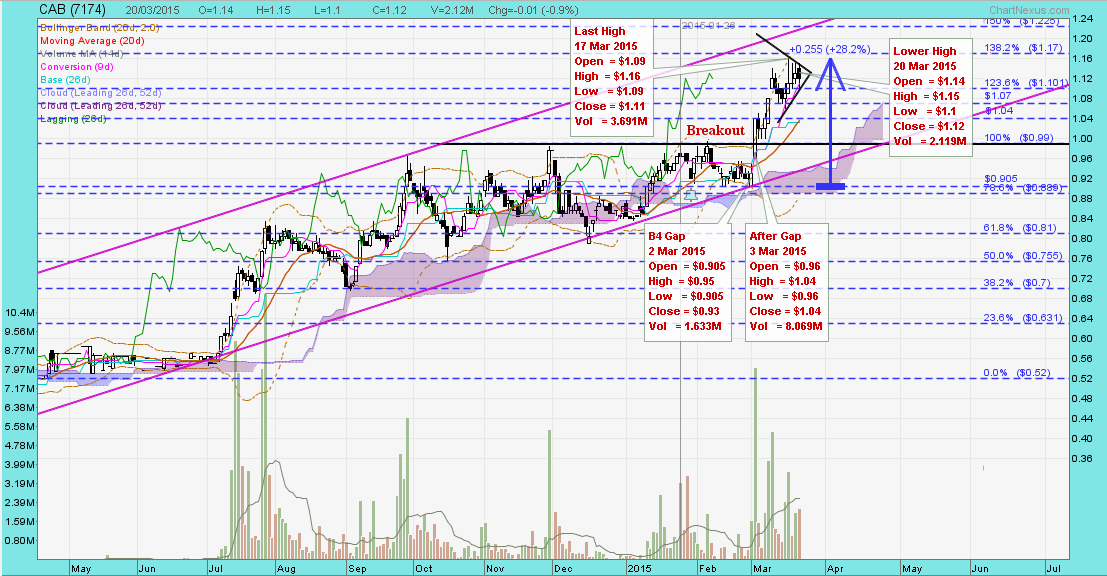

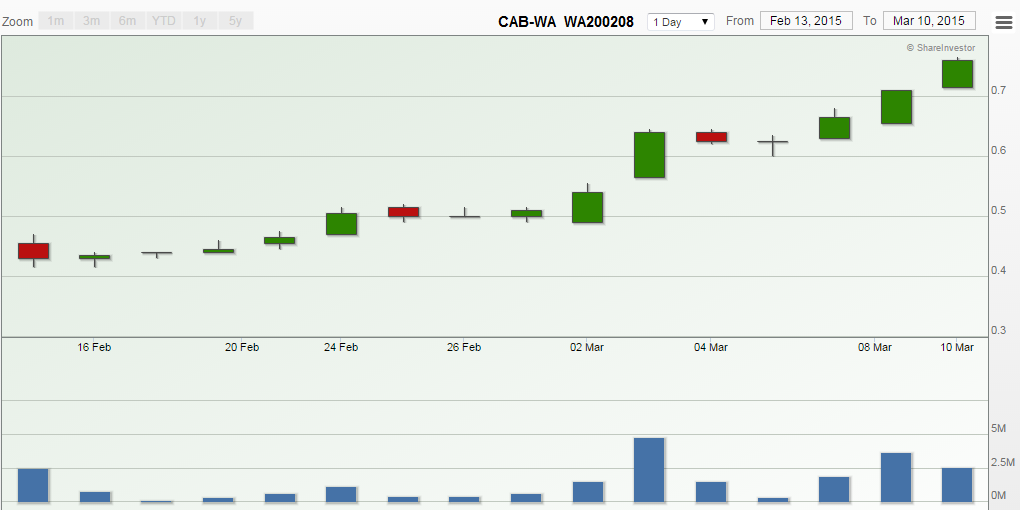

CAB ~ Symmetrical Triangle formationCAB hit high of RM1.15 and closed with a spinning top @ RM1.12 (-0.01, 0.9%) with 2.12m shares done on 20 Mar 2015. Immediate support @ RM1.10, immediate resistance @ RM1.17.  Cab-WA200208 Cab-WA200208 hit high of RM0.855 and closed with a long black marubozu @ RM0.785 (-0.055, -6.55%) with 2.03m shares done on 20 Mar 2015. Cab-WA200208 exercise price @ RM0.55 per warrant ~ 27 Feb 2015  CAB hit high of RM1.14 and closed @ RM1.12 (+0.04, +3.7%) with 5.35m shares done on 10 Mar 2015. Cab-WA200208 hit high of RM0.765 and closed @ RM0.76 (+0.05, +7.4%) with 2.54m shares done on 10 Mar 2015.

|

|

.

.