|

|

Post by zuolun on Dec 22, 2014 7:33:50 GMT 7

|

|

|

|

Post by zuolun on Dec 22, 2014 8:12:23 GMT 7

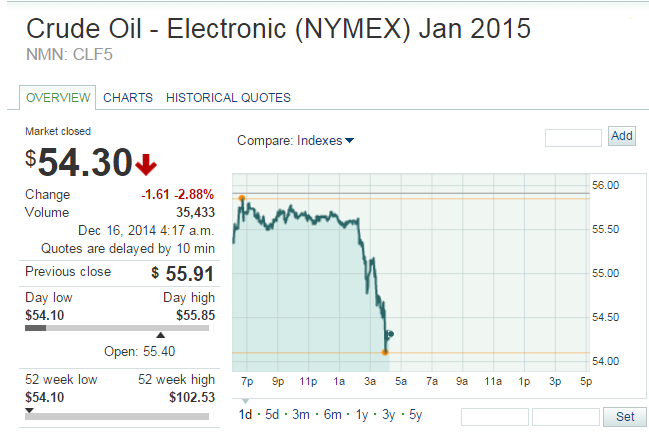

Russian roulette: Taxpayers could be on the hook for trillions in oil derivatives — 20 Dec 2014 SIA hedged fuel at an average of US$116 a barrel of jet fuel — 5 Dec 2014 Crude oil and its derivatives — 30 May 2012 b]How a big bet on oil went bust[/b][/a] — 29 Mar 2010 Oil derivatives are financial instruments using oil, usually crude, as an underlying asset. The derivative has no inherent value and is only a contract for an oil-related activity, but people can trade, sell, and buy derivatives to access the value of the oil used as the basis of the contract. Such contracts have been a part of financial markets since the 1800s and provide producers of various products with a number of useful tools for conducting business. Companies can use oil derivatives to distribute and reduce risk, as well as to address issues like not wanting to store oil for extended periods of time. The most basic oil derivative is a futures contract. When people prepare the contract, one party agrees to buy a set amount of oil at a given price on a date in the future. Another form is an options contract, where people have the option to make a purchase on a particular date, and they can then decide whether they want to exercise it. Oil derivatives allow people to manage risk; for example, a futures contract can help people avoid temporary volatility in oil pricing and get oil at a guaranteed price. Options can provide for hedging, creating an opportunity to buy below market price or sell above it, depending on the structure of the contract.

|

|