|

|

Post by zuolun on Nov 10, 2013 20:28:20 GMT 7

Sheng Siong — The Elliott Wave PatternSheng Siong is on the corrective Wave-A down; crucial support @ S$0.62.

|

|

|

|

Post by zuolun on Dec 1, 2013 12:42:32 GMT 7

|

|

|

|

Post by zuolun on Dec 2, 2013 16:51:53 GMT 7

Sheng Siong — The Elliott Wave PatternSheng Siong is on the corrective Wave-A down; crucial support @ S$0.62.

|

|

|

|

Post by zuolun on Dec 7, 2013 15:47:40 GMT 7

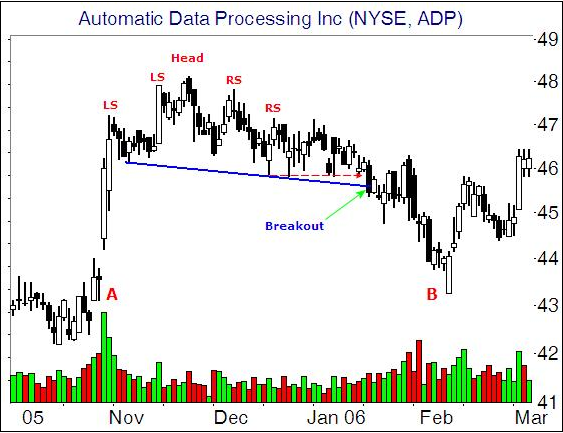

pertama.freeforums.net/post/1511Sheng Siong — H&S breakout; interim TP S$0.56Immediate support S$0.575, immediate resistance S$0.62, the support-turned-resistance level.  Sheng Siong (weekly) chart as at 29 Nov 2013 Sheng Siong (weekly) chart as at 29 Nov 2013

|

|

|

|

Post by zuolun on Dec 13, 2013 14:21:47 GMT 7

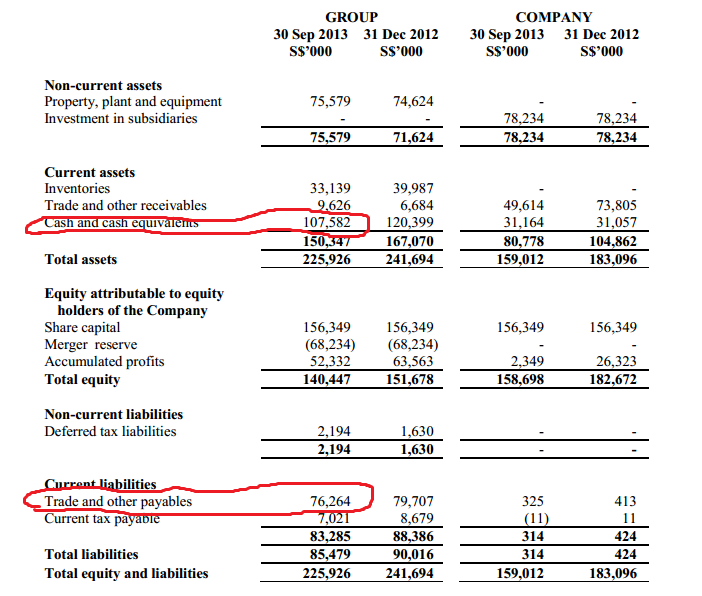

Sheng Siong – More Than A Modern Homemaker’s Friend — 11 Dec 2013 Sheng Siong's Net Profit Figures:Q1'12 -> Rev : 160 mil Net Profit -> 16.8 mil Q2'12 -> Rev : 146 mil Net Profit -> 7.0 mil Q3'12 -> Rev : 170 mil net Profit -> 9.8 mil Q4'12 -> Rev : 161 mil Net Profit -> 7.9 mil Q1'13 -> Rev : 179 mil Net Profit -> 10.5 mil Q2'13 -> Rev : 159 mil Net Profit -> 8.5 mil Note: 1. The biggest problem/issue of Sheng Siong is that, the 4 big bosses are drawing big fat million dollar salaries totalling S$7m. (For 2011 and 2012, both years, 4 directors got bet. $1.5m to $1.75m, bosses take the golden eggs, the leftover then goes to shareholders.) 2. Operating cost pressure on the rise -> Foreign Worker Levies

|

|

|

|

Post by zuolun on Dec 16, 2013 16:25:21 GMT 7

Sheng Siong — A "stair-step decline" chart pattern Sheng Siong has an easy to recognise "stair-step decline" chart pattern. The share price moves down slow and steady day by day without strong support due to lack of buying interest.

|

|

|

|

Post by odie on Dec 16, 2013 16:52:22 GMT 7

zuolun bro,

thanks

the directors are drawing too high a salary

|

|

|

|

Post by zuolun on Dec 16, 2013 17:57:29 GMT 7

zuolun bro, thanks the directors are drawing too high a salary odie, Sheng Siong's directors and management staffs were extremely smart to structure its IPO shares and package it as a dividend-yield stock to attract strong support from five (5) international institutional investors then. The best selling point of Sheng Siong till to date is that, the company is cash-rich with no debts. However, most retail investors who bought Sheng Siong's share (at the last burst of fire) for its regular dividends payment now lose big money as the share price has been dropping non-stop after it had peaked @ S$0.725 on 1 Aug 2013. Besides starshine who had vested in Sheng Siong and cut-loss, I've another stubborn friend who bought Sheng Siong @ S$0.67 and kept on averaging down at S$0.65, S$0.60 and S$0.575 and currently holding total of 350 lots.   |

|

|

|

Post by zuolun on Dec 16, 2013 18:46:32 GMT 7

|

|

|

|

Post by odie on Dec 16, 2013 18:51:35 GMT 7

zuolun bro, thanks the directors are drawing too high a salary odie, Sheng Siong's directors and management staffs were extremely smart to structure its IPO shares and package it as a dividend-yield stock to attract strong support from five (5) international institutional investors then. The best selling point of Sheng Siong till to date is that, the company is cash-rich with no debts. However, most retail investors who bought Sheng Siong's share (at the last burst of fire) for its regular dividends payment now lose big money as the share price has been dropping non-stop after it had peaked @ S$0.725 on 1 Aug 2013. Besides starshine who had vested in Sheng Siong and cut-loss, I've another stubborn friend who bought Sheng Siong @ S$0.67 and kept on averaging down at S$0.65, S$0.60 and S$0.575 and currently holding total of 350 lots. yup, zuolun bro it is very sad that they don't realise the net profit after tax is after deducting for directors' remuneration |

|

|

|

Post by zuolun on Dec 21, 2013 9:58:14 GMT 7

|

|

|

|

Post by zuolun on Dec 21, 2013 12:02:21 GMT 7

Sheng Siong – More Than A Modern Homemaker’s Friend — 11 Dec 2013 Sheng Siong's Net Profit Figures:Q1'12 -> Rev : 160 mil Net Profit -> 16.8 mil Q2'12 -> Rev : 146 mil Net Profit -> 7.0 mil Q3'12 -> Rev : 170 mil net Profit -> 9.8 mil Q4'12 -> Rev : 161 mil Net Profit -> 7.9 mil Q1'13 -> Rev : 179 mil Net Profit -> 10.5 mil Q2'13 -> Rev : 159 mil Net Profit -> 8.5 mil Note: 1. The biggest problem/issue of Sheng Siong is that, the 4 big bosses are drawing big fat million dollar salaries totalling S$7m. (For 2011 and 2012, both years, 4 directors got bet. $1.5m to $1.75m, bosses take the golden eggs, the leftover then goes to shareholders.) 2. Operating cost pressure on the rise -> Foreign Worker Levies By Rosesyrup 02 Aug 2013 The reason that Sheng Shiong (SS) has such large scale of operation right now is that it managed to find and exploit the gap between NTUC and One-Dollar shops. Throughout the years, SS had been mindful of its cost and was able to transfer the cost saving to its customers. The cost saving capability thus becomes SS's competitive advantage that enable it to rout stronger competitors like Shop N Save. However, in recent SS appeared to have lost sight of the engine it depends on to propell its growth. In this report, I will attempt to explain what SS should not have and should have done, which might threaten its fundmental. Should Not Have Done

- 24 Hours Operation: In the bid to remain " competitive" , SS followed NTUC's strategy of operating 24hours stores. However, this would prove to be a deadly mistake. With the little passenger traffic, low products' contribution margin, high overhead cost (due to SS large store front) and high labor cost (SS is a labor intensive firm), the cost of operating in the night can hardly justify the revenue. The only reason why 7 Eleven could run such 24 hours operation is due to its much smaller store, high contribution margin (The same products cost a lot more in 7 Eleven), and low labor cost (store manned by one staff). Moving back to SS, the losses from night operation has got much deeper implication. The huge losses from serving small amount of customers in the night will now be transferred to the majority of customers who do not make use of the night service through higher product prices. This reduced SS's competitiveness. SS would be better off by giving NTUC the night market which is loss making.

- E-Grocery: E-Grocery has been pretty successful in large countries like US where population is scatter across the land. The story is quite different for Singapore which has uniquely small landscape and numerous high rise flats, nearly every family has access to a supermarket which is just a stone throw away from their block. This makes E-Grocery hardly necessary. Furthermore, the higher products' price in E-Grocery is targeted at a higher end customers who are very different from SS's current penny pinching customers. However, do note that I am not trying to imply that SS should not go into E-Grocery at all. It is just that the time isn't ripe. SS could have better invest its capital on fine tuning many parts of its operation- which will be discussed in the SHOULD HAVE DONE part. The result of fine tuning would have increase SS efficient and enable it to better compete with the first movers-e.g. red marts. Simply put, the strategy is to let NTUC engage in a costly competition with the first movers first, meanwhile SS focus on improving its physical distribution and go in later. Afterall, the first mover has the advantage of doing away their overhead cost.

- Mandai Link Distribution Centre: SS invested 65millions in this warehouse will lead to higher fixed cost and higher break even point. SS could have first rent a warehouse while continue to explore the option of cross-docking. This will remove the need of purchase expensive property on Singapore scarced land, and reduce its manpower which is another expensive resources in Singapore.

Should Have DoneIf you are thinking about Walmart now, you are right. The history of Walmart provide many important learning points and guidelines for SS in its quest toward dominance of Singapore market. - Invest In Better IT System: SS lack of good IT support is especially evident in its outlet stockpile. It is not rare to: pick up expired products, hear employees complaining about overordering goods that are not selling and not ordering goods that are lacking. Just look up ontop of SS's shelves, the large number of boxes stacked on the shelves are the amount of goods that the employees overordered. All these point to the fact that SS is lacking an IT system that keep track of its goods and is therefore unable to make informed decision. A good item system that is able predict demand and make informed ordering should help SS to reduce unnecessary inventory level (wastage), and free up space in the store which will replace the need of a warehouse.

- Setting Up Self Service Cashiers: These would reduce SS reliance on its massive manpower. Currently, much of the staff in SS stores are Malaysian workers.This is expected to increasing eat into SS profit as government continues to increase foreign levy. Just a little sidetrack, if you ever see a SS's staff standing infront of the store exit, he is not ideling- he is there to make sure there is no shoplifting going on. Assuming that the pay of that SS staff is $7 per hour, it would only make sense if SS starts losing a 5kg pack of rice (worth around $7) to shoplifting per hour. During peak hours, you can ever see more than one of these " security guards" . Reliance on security camera would make much more economic sense. Anyway, instead of reining in its staff cost, SS is still continuing its aggressive employment policy- overstaffing is what might follow.

- Change In Management: Members of the management team in SS are mostly made up of the founding father's family members. This gave rise to some kind of nepotism where the decision makers might not be the best and most capable. At least, the founding father, Lim Hock Chee remain to occupy the most powerful and important position in the firm. One need to understand that the founding father not necessary has the skills and experience require to manage the now much larger and complex company, and take it to greater height. This is true for many startups, though painful, it is a delimma between CASH AND KING Thus for SS, the resulting poor management decision making can be seen from cases such as buying 5 wet markets that can't be converted into supermarket, and the poor strategic decision to operate 24hours. It is advisable that SS start bringing in professional managers to its top management office. Otherwise more costly problems would be expected to set in as the business grow more complicated and goes outside the expertise of the current management.

In a nutshell, instead of engaging in costly battle for new markets, SS should focus on streamlining it current distribution network and aim to replace NTUC as Singapore top retailer. However, should SS continue its current stratgey that stray away from its original customer group, it will soon loses it competitive advantage. The resulting sign of SS failing would then be expected to surface in 2 years time, when economy growth is strong and consumers are turning away from basic products sold by SS. Based on the above forecast and the expectation that management would not made much changes from its current strategy, I have assigned SS a TP of 58cents. Disclaimer:

- The following analysis is purely my personal opinion. I urge you to do your own assessment and calculation for any relevant decision making purposes.

- The analysis is based purely on consideration of the company's financial and economic interest.

|

|

|

|

Post by zuolun on Dec 22, 2013 17:27:19 GMT 7

|

|

|

|

Post by zuolun on Dec 23, 2013 7:04:14 GMT 7

|

|

|

|

Post by zuolun on Jan 9, 2014 17:47:45 GMT 7

|

|