|

|

Post by me200 on May 21, 2014 19:38:30 GMT 7

Below announcement might be the true reason why SMRT price shot up >40% recent.

Government to overhaul public transport sector

SINGAPORE - The public bus industry will undergo a major shift in the way it is run starting from the second half of this year, in a move to improve bus services further.On Wednesday, the Government announced its plans to overhaul the sector by shifting from the existing privatised model to a "Government contracting model".

Under this new model, the Land Transport Authority (LTA) will engage bus operators to run services through competitive bidding, determine the bus routes to be provided and set service standards. Operators will be paid a fee to run the services for a period of five years, while the Government bears revenue risk by retaining the fare revenue

SMRT says proposal for rail financing model submitted to govt - 2May2014

Transport operator SMRT said it has submitted its proposal for a rail financing model to the government a month ago.

I believe insider(s) reacted on this proposal and hope for positive outcome from government. Retail investors like us always lose because we are the last to know. Insider proactive, we reactive.

The recent rumour about asset sale to Government has blown out of all proportions. Many must have thought that the Government will pay well for the asset sale and henceforth, SMRT can concentrate in O&M and forget about having to furnishing the mountain of debts so far accumulated. However, this could be a far reaching scenario although the part of SMRT can concentrate in O&M while Government owning the asset has certain benefits but not a great deal. First, In 1987 when Government handed over MRTC to SMRT, SMRT paid only SGD$1/= for taking over the asset. Can we imagine how much Government will be willing to pay for the return of the asset? Second, the Government has paid for some major maintenance work including the $500 mil not so long ago for improving the MRT tracks. Is Government also thinking about paying for these when taking back the asset? Furthermore, Government is already responsible for the cost of maintaining the rolling stocks which is the bulk of the maintenance cost. What is then the difference of SMRT being a "train operator" under the present structure. Will the asset sale back to the Government made any difference under the new structure? Hong Kong MTRC can be profitable and excel because they can leverage on the property development around the MRT tracks. Imagine if SMRT were to return all these asset and become solely a train operator, they would have lost the chance to gain from their property development. Although Singapore Government and its citizens were not in favour of SMRT profiting from property development, SMRT has already existing properties that are worth billions of dollars; for example, the headquarter in North Bridge Road, the various depots with potential for further development. Outram Park station can be a good location for multi-story development where SMRT can leverage to earn some good buck. What about the valuable space underneath and within the boundary of the MRT tracks? SMRT has more to lose if these assets were to be returned to the Government. Have a feeling that the SMRT managements have been doing the extremes. The past management concentrated on property development and neglected the O&M; the present one just doing the opposite. Chartwise, SMRT has not shown any determination to break the resistance of 1.32 and retreated from breaking it 2 days ago. If SMRT continues to fall and breaks 1.16, it would want to try to find support around the 100-day, failing which, we should see SMRT meeting its "water-loo". The present chart indicated this counter is very much over-bought.  |

|

|

|

Post by me200 on May 22, 2014 6:15:00 GMT 7

Bus contracting model good news for SMRT, SBS Transit: analysts CNA 22Apr2014.

SINGAPORE: Analysts say the new bus contracting model -- under which the Government will own all bus assets -- is good news for the two incumbent public transport operators SMRT and SBS Transit.

Below announcement might be the true reason why SMRT price shot up >40% recent.

Government to overhaul public transport sector

SINGAPORE - The public bus industry will undergo a major shift in the way it is run starting from the second half of this year, in a move to improve bus services further.On Wednesday, the Government announced its plans to overhaul the sector by shifting from the existing privatised model to a "Government contracting model".

Under this new model, the Land Transport Authority (LTA) will engage bus operators to run services through competitive bidding, determine the bus routes to be provided and set service standards. Operators will be paid a fee to run the services for a period of five years, while the Government bears revenue risk by retaining the fare revenue

SMRT says proposal for rail financing model submitted to govt - 2May2014

Transport operator SMRT said it has submitted its proposal for a rail financing model to the government a month ago.

I believe insider(s) reacted on this proposal and hope for positive outcome from government. Retail investors like us always lose because we are the last to know. Insider proactive, we reactive.

|

|

|

|

Post by oldman on May 22, 2014 7:26:07 GMT 7

I think the model is not the sticky point. It is how much the government is willing to pay for the existing infrastructural assets. If it is too much, it may look like a bailout as these listed companies did benefit from these assets in the past. My guess is that they will take the middle road and in the end, the euphoria in the share price may not justify the future increased competitive landscape and significantly reduced barrier to entry of its core businesses. |

|

|

|

Post by zuolun on May 22, 2014 7:45:57 GMT 7

odie, SMRT's share price still has the last catalyst to impact the current strong downtrend and the best one is none other than nationalisation. In other words, when a listed-company makes good profit, the shareholders benefit but when a listed-company makes losses and/or gets into sticky problems, get the government to fix it, i.e. bail out the listed-company with tax payers' money, similar pattern like OLAM. — 22 May 2014 SMRT Top 20 Shareholders as of 6th June 2013 |

|

|

|

Post by me200 on May 25, 2014 8:28:05 GMT 7

|

|

|

|

Post by zuolun on Jun 6, 2014 13:08:58 GMT 7

|

|

|

|

SMRT

Jun 30, 2014 14:33:29 GMT 7

oldman likes this

Post by zuolun on Jun 30, 2014 14:33:29 GMT 7

|

|

|

|

SMRT

Jul 7, 2014 16:12:06 GMT 7

Post by simplemind on Jul 7, 2014 16:12:06 GMT 7

ZL bro,

What do u think of smrt? Looks like forming steps upward.

|

|

|

|

Post by zuolun on Jul 7, 2014 16:51:20 GMT 7

ZL bro, What do u think of smrt? Looks like forming steps upward. simplemind, SMRT and MAS's major cheng Kay = Govt. The big punters of both countries got it right that the SG & M'sian gov't will use tax payers monies to bill out these 2 GLCs whenever they incur losses = 100% guaranteed no bankruptcy. The late-comers who want to join the party at current price now maybe still can get some breadcrumbs...  This is the same logic why the big players like Oei Hong Leong buying AIG shares in 2008 and why my Singaporean friend dare to buy afew million MAS shares at 20.5 sen on 10 Mar 2014, then. "There are three ways to make a living in this business: be first, be smarter, or cheat." — Margin CallSMRT's share price still has the last catalyst to impact the current strong downtrend and the best one is none other than nationalisation. In other words, when a listed-company makes good profit, the shareholders benefit but when a listed-company makes losses and/or gets into sticky problems, get the government to fix it, i.e. bail out the listed-company with tax payers' money, similar pattern like OLAM. Exclusive: State fund plans to take Malaysia Airlines private for restructuring: sources - 2nd July 2014 At MAS's current price of 21 sen per share, majority shareholder Khazanah would need to pay only 1.05 billion ringgit ($328 million) for the 30.6 percent of shares it does not already own, according to Reuters calculations.

MAS would have a "break-up" value of 4.15 billion ringgit, well above its current market value of 3.4 billion ringgit, Maybank Research said in an April report. The airlines' profitable units include MAS Engineering, Airport Terminal Services and its budget airline unit Firefly.

zuolun , your friend is brave. At 22.5 sen with 16.9 bil shares in issue, its market cap is RM 3.8 billion. It has borrowings of RM 11.75 bil with cash of RM 3.87 bil and aircraft PP&E of RM 14.6 bil. In June 2013, it had a 4 for 1 rights issue at 23 sen raising RM3 bil. Appears that most of its current cash holdings may have come from this rights issue. Last year, it lost RM 1.17 bil on revenues of RM 14.5 bil. With the loss of MH 730, it is likely that its financials will be impacted in the next quarter. Am actually quite surprised that the share price has held up quite well compared to its rights price. I don't think the share price is in bargain territory yet. MAS 2013 Financial Statement oldman, His gambling instinct on MAS was quite similar to Oei Hong Leong buying AIG shares in 2008. Everyone was extremely -ve on MAS after MH370 went missing last month. On Monday 10 Mar 2014 when market opened, my Singaporean friend was the only exceptional one in our group who bought afew million MAS shares at 20 sen, 20.5 sen and 21 sen, average 20.5 sen, none followed him. It reminds me of this Chinese saying, 物极必反,否极泰来! (When extremes meet, the situation is reversed.) |

|

|

|

SMRT

Aug 18, 2014 16:49:00 GMT 7

Post by zuolun on Aug 18, 2014 16:49:00 GMT 7

|

|

|

|

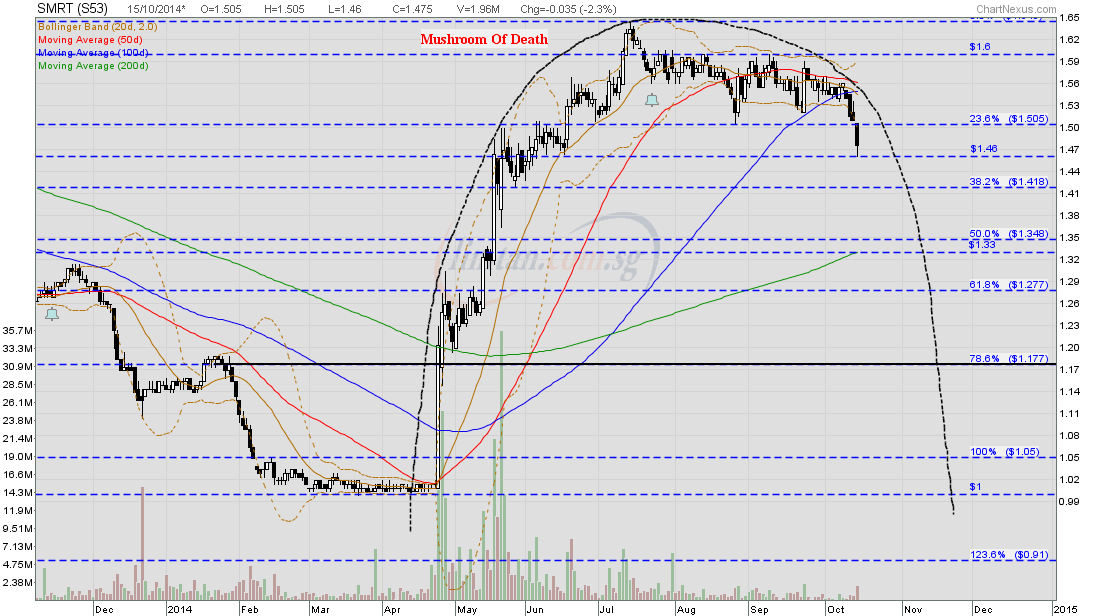

Post by zuolun on Oct 15, 2014 22:00:31 GMT 7

SMRT — Classic MOD chart pattern The last line of defense @ S$1.33, the 200d SMASMRT closed with a hammer @ S$1.475 (-0.035, -2.3%) with 1.96m shares done on 15 Oct 2014. Immediate support @ S$1.42, immediate resistance @ S$1.51.

|

|

|

|

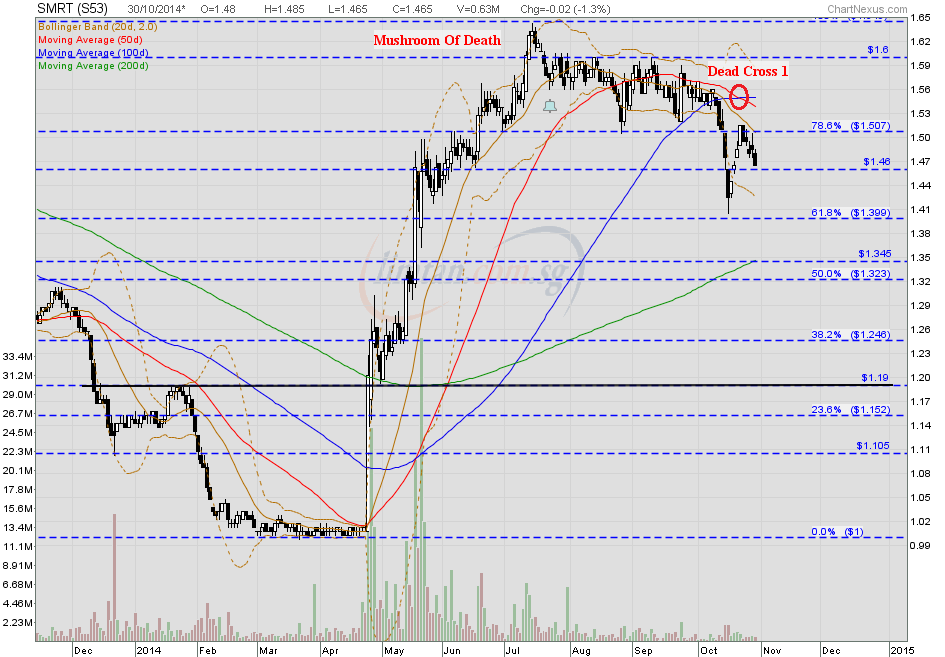

Post by zuolun on Oct 31, 2014 6:11:21 GMT 7

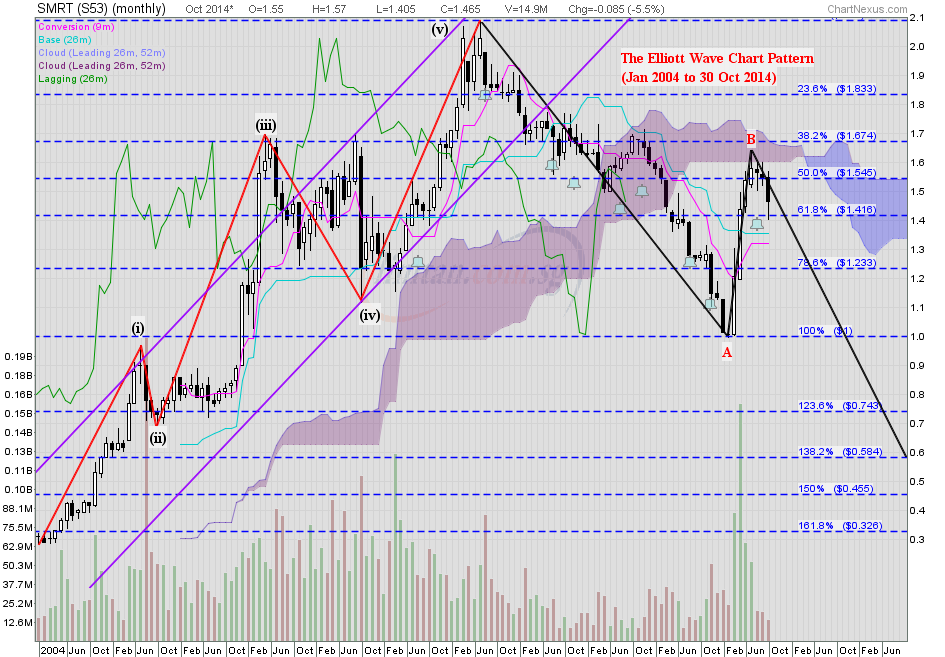

SMRT — Classic MOD chart pattern The last line of defense @ S$1.345, the 200d SMASMRT closed with a black marubozu @ S$1.465 (-0.02, -1.3%) with extremely thin volume done at 627 lots on 30 Oct 2014. Immediate support @ S$1.40, immediate resistance @ S$1.51.   SMRT (Jan 2004 to 30 Oct 2014) — The Elliott Wave Chart Pattern SMRT (Jan 2004 to 30 Oct 2014) — The Elliott Wave Chart Pattern SMRT (weekly) chart had a Bullish Three-Drives formation dated 14 Apr 2014, the bullish breakout materialized on 24 Apr is strictly due to technical rebound, not fundamental rebound, i.e. it is a bull trap = a dead-cat bounce, which is unsustainable.

|

|

|

|

Post by zuolun on Nov 7, 2014 16:39:55 GMT 7

|

|

|

|

Post by zuolun on Jul 11, 2015 10:41:52 GMT 7

|

|

|

|

Post by zuolun on Jul 13, 2015 0:31:25 GMT 7

|

|