|

|

SMRT

Apr 24, 2014 15:42:56 GMT 7

oldman likes this

Post by zuolun on Apr 24, 2014 15:42:56 GMT 7

oldman, 当局者迷,旁观者清。

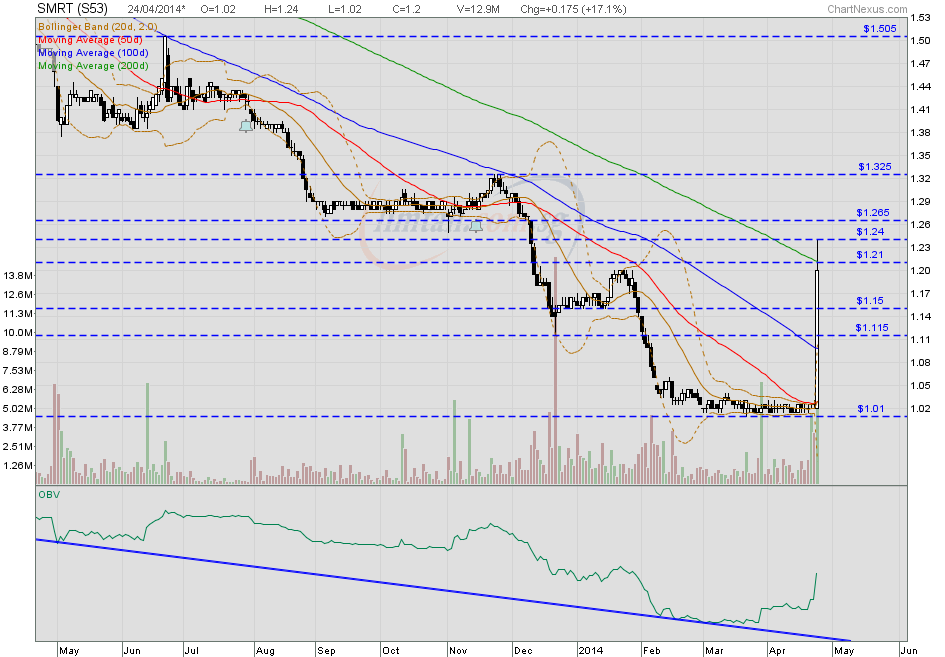

It means the accuracy/probable direction of price movement using TA is strictly based on one's ability to correctly read the charts without any emotions. It would be entirely different if one is heavily vested in a stock (long/short), especially the insider players.  (BBs could re-draw the charts anytime when face with opposing forces, example TA showed a huge monkey in OLAM's chart pattern ). — Bull Trap; Bullish Three–Drives BreakoutSMRT surged with a long white marubozu to high of S$1.24 and traded @ S$1.20 (+0.175, +17.1%) with extremely high volume done at 12.9m shares on 24 Apr 2014 at 4.40pm. Immediate resistance @ S$1.26, immediate support @ S$1.15, next support @ S$1.115. SMRT's primary trend is down, the dead cat bounce is an opportunity to sell into strengrh, not buy.   SMRT (weekly) — Bullish Three–Drives Formation SMRT (weekly) — Bullish Three–Drives Formation

|

|

|

|

Post by me200 on Apr 24, 2014 17:42:16 GMT 7

MRT reversal? Bye bye?

oldman, 当局者迷,旁观者清。

It means the accuracy/probable direction of price movement using TA is strictly based on one's ability to correctly read the charts without any emotions. It would be entirely different if one is heavily vested in a stock (long/short), especially the insider players. (BBs could re-draw the charts anytime when face with opposing forces, example TA showed a huge monkey in OLAM's chart pattern ). — Bull Trap; Bullish Three–Drives BreakoutSMRT surged with a long white marubozu to high of S$1.24 and traded @ S$1.20 (+0.175, +17.1%) with extremely high volume done at 12.9m shares on 24 Apr 2014 at 4.40pm. Immediate resistance @ S$1.26, immediate support @ S$1.15, next support @ S$1.115. SMRT's primary trend is down, the dead cat bounce is an opportunity to sell into strengrh, not buy. SMRT (weekly) — Bullish Three–Drives Formation

|

|

|

|

SMRT

Apr 24, 2014 17:59:52 GMT 7

odie likes this

Post by zuolun on Apr 24, 2014 17:59:52 GMT 7

|

|

|

|

Post by me200 on Apr 25, 2014 6:17:23 GMT 7

SMRT shares up 20% on asset sale speculation - NST 25Apr2014

LISTED public transport operator SMRT Corp's shares yesterday staged their biggest-ever one-day gain in recent memory, soaring almost 20 per cent, as investors speculated that a plan for SMRT to sell its rail assets to the Government was imminent

classical .... expect the unexpected.

|

|

|

|

Post by zuolun on Apr 25, 2014 8:08:19 GMT 7

SMRT shares up 20% on asset sale speculation - NST 25Apr2014

LISTED public transport operator SMRT Corp's shares yesterday staged their biggest-ever one-day gain in recent memory, soaring almost 20 per cent, as investors speculated that a plan for SMRT to sell its rail assets to the Government was imminent

classical .... expect the unexpected. haha...this type of bullish news never fails to cheer me up!  Always able to trap the silly bulls high and dry...it reminds me of SuperGroup!  |

|

|

|

Post by zuolun on Apr 25, 2014 17:39:31 GMT 7

|

|

|

|

SMRT

Apr 25, 2014 19:40:54 GMT 7

me200 likes this

Post by odie on Apr 25, 2014 19:40:54 GMT 7

SMRT shares up 20% on asset sale speculation - NST 25Apr2014

LISTED public transport operator SMRT Corp's shares yesterday staged their biggest-ever one-day gain in recent memory, soaring almost 20 per cent, as investors speculated that a plan for SMRT to sell its rail assets to the Government was imminent

classical .... expect the unexpected.

me200, for transport co which are government linked, only NOL has sold its building. SBS and SMRT hasn't sold any buildings to date. |

|

|

|

Post by odie on Apr 25, 2014 19:43:28 GMT 7

Though not ruled out entirely, is the possibility of nationalizing the company. Hard to imagine why that should be the case. We do not think it is in the interest of the government to “own” back the company, and subject itself to further abuse from disgruntled commenters whenever trains breakdown, or fare increase is necessitated. Yes, granted that Temasek owns 55% of the company, but this is not so Olam-like. Of course, many of us are left scratching our heads on that transaction.

This is so funny.

LOL

|

|

|

|

Post by zuolun on Apr 26, 2014 12:01:00 GMT 7

Though not ruled out entirely, is the possibility of nationalizing the company. Hard to imagine why that should be the case. We do not think it is in the interest of the government to “own” back the company, and subject itself to further abuse from disgruntled commenters whenever trains breakdown, or fare increase is necessitated. Yes, granted that Temasek owns 55% of the company, but this is not so Olam-like. Of course, many of us are left scratching our heads on that transaction.

This is so funny.

LOL

odie, In the US: "Don't fight the Fed". In Singapore: "Don't fight Temasek and GLC stocks".  odie, SMRT's share price still has the last catalyst to impact the current strong downtrend and the best one is none other than nationalisation. In other words, when a listed-company makes good profit, the shareholders benefit but when a listed-company makes losses and/or gets into sticky problems, get the government to fix it, i.e. bail out the listed-company with tax payers' money, similar pattern like OLAM. |

|

|

|

Post by me200 on May 1, 2014 6:41:32 GMT 7

SMRT (unaudited) FY14 result with EPS down to 4.1 cents from 5.5 cents (-25.7%).

Results for the Fourth Quarter ended 31 March 2014

With last closing price of $1.22, it's PE is ~30. IMO, this is extremely high.

Still wonder  if the recent 19% (Apr 24, 2014) price surge is due to government intervention!? if the recent 19% (Apr 24, 2014) price surge is due to government intervention!?

*** Surprisingly, it's rail Repair and Maint cost only increase marginally by 2.2% (everyone is expected SMRT get burnt with high R&M cost).

Hi Candy, Refer to below EPS chart, I assume that SMRT Q4Fy2013 EPS is 0. Hence the 'forecast' EPS is <6.3 cent. However, SMRT Q4FY2013 is -0.7842 cents and thus FY2013 EPS is 5.5 cents. Base on 1Q and 2Q FY2014 EPS, I estimate (agak agak only) should be < 5.5 cents. Unless govt agrees to revise the ride fair upward, then we should see more earnings. p.s. Bus service is bleeding severely despite revenue increase. Hi me200, thank you for sharing the Fair value with reasonable margin of safety utilising FA. Would like to clarify, how did you derive the EPS figure of $0.063 since 2013 EPS is only $0.0548. Is $0.063 based on forecasted EPS for 2014?  Quote me200, Quote me200,"If one wish tho invest when the PER is ~15X, the share price willl be $0.945 (15 * 0.063)." Buffett’s Most Profitable Deals Good Businesses At Fair Prices Or Vice Versa?March 13, 2013 “More than 50 years ago, Charlie told me that it was far better to buy a wonderful business at a fair price than to buy a fair business at a wonderful price. Despite the compelling logic of his position, I have sometimes reverted to my old habit of bargain-hunting, with results ranging from tolerable to terrible. Fortunately, my mistakes have usually occurred when I made smaller purchases. Our large acquisitions have generally worked out well and, in a few cases, more than well.” |

|

|

|

Post by stockpicker on May 1, 2014 9:00:19 GMT 7

The recent rumour about asset sale to Government has blown out of all proportions. Many must have thought that the Government will pay well for the asset sale and henceforth, SMRT can concentrate in O&M and forget about having to furnishing the mountain of debts so far accumulated. However, this could be a far reaching scenario although the part of SMRT can concentrate in O&M while Government owning the asset has certain benefits but not a great deal. First, In 1987 when Government handed over MRTC to SMRT, SMRT paid only SGD$1/= for taking over the asset. Can we imagine how much Government will be willing to pay for the return of the asset? Second, the Government has paid for some major maintenance work including the $500 mil not so long ago for improving the MRT tracks. Is Government also thinking about paying for these when taking back the asset? Furthermore, Government is already responsible for the cost of maintaining the rolling stocks which is the bulk of the maintenance cost. What is then the difference of SMRT being a "train operator" under the present structure. Will the asset sale back to the Government made any difference under the new structure? Hong Kong MTRC can be profitable and excel because they can leverage on the property development around the MRT tracks. Imagine if SMRT were to return all these asset and become solely a train operator, they would have lost the chance to gain from their property development. Although Singapore Government and its citizens were not in favour of SMRT profiting from property development, SMRT has already existing properties that are worth billions of dollars; for example, the headquarter in North Bridge Road, the various depots with potential for further development. Outram Park station can be a good location for multi-story development where SMRT can leverage to earn some good buck. What about the valuable space underneath and within the boundary of the MRT tracks? SMRT has more to lose if these assets were to be returned to the Government. Have a feeling that the SMRT managements have been doing the extremes. The past management concentrated on property development and neglected the O&M; the present one just doing the opposite. Chartwise, SMRT has not shown any determination to break the resistance of 1.32 and retreated from breaking it 2 days ago. If SMRT continues to fall and breaks 1.16, it would want to try to find support around the 100-day, failing which, we should see SMRT meeting its "water-loo". The present chart indicated this counter is very much over-bought.  |

|

|

|

Post by zuolun on May 1, 2014 12:29:17 GMT 7

SMRT (weekly) chart had a Bullish Three-Drives formation dated 14 Apr 2014, the bullish breakout materialized on 24 Apr is strictly due to technical rebound, not fundamental rebound, i.e. it is a bull trap = a dead-cat bounce, which is unsustainable.  SMRT — Bull Trap; Bullish Three–Drives BreakoutSMRT surged with a long white marubozu to high of S$1.24 and traded @ S$1.20 (+0.175, +17.1%) with extremely high volume done at 12.9m shares on 24 Apr 2014 at 4.40pm. Immediate resistance @ S$1.26, immediate support @ S$1.15, next support @ S$1.115. SMRT's primary trend is down, the dead cat bounce is an opportunity to sell into strengrh, not buy. SMRT's primary trend is down, should the dead cat bounce materialize, it's an opportunity to run road, not buy. SMRT's next support @ S$0.94, the 38.2% FIBO retracement on the EW chart pattern. SMRT (weekly) — Bullish Three-Drives Formation SMRT — The Elliott Wave Chart Pattern SMRT — The Elliott Wave Chart Pattern |

|

|

|

Post by me200 on May 2, 2014 13:44:39 GMT 7

SMRT says proposal for rail financing model submitted to govt - 2May2014

Transport operator SMRT said it has submitted its proposal for a rail financing model to the government a month ago.

I believe insider(s) reacted on this proposal and hope for positive outcome from government. Retail investors like us always lose because we are the last to know. Insider proactive, we reactive.

The recent rumour about asset sale to Government has blown out of all proportions. Many must have thought that the Government will pay well for the asset sale and henceforth, SMRT can concentrate in O&M and forget about having to furnishing the mountain of debts so far accumulated. However, this could be a far reaching scenario although the part of SMRT can concentrate in O&M while Government owning the asset has certain benefits but not a great deal. First, In 1987 when Government handed over MRTC to SMRT, SMRT paid only SGD$1/= for taking over the asset. Can we imagine how much Government will be willing to pay for the return of the asset? Second, the Government has paid for some major maintenance work including the $500 mil not so long ago for improving the MRT tracks. Is Government also thinking about paying for these when taking back the asset? Furthermore, Government is already responsible for the cost of maintaining the rolling stocks which is the bulk of the maintenance cost. What is then the difference of SMRT being a "train operator" under the present structure. Will the asset sale back to the Government made any difference under the new structure? Hong Kong MTRC can be profitable and excel because they can leverage on the property development around the MRT tracks. Imagine if SMRT were to return all these asset and become solely a train operator, they would have lost the chance to gain from their property development. Although Singapore Government and its citizens were not in favour of SMRT profiting from property development, SMRT has already existing properties that are worth billions of dollars; for example, the headquarter in North Bridge Road, the various depots with potential for further development. Outram Park station can be a good location for multi-story development where SMRT can leverage to earn some good buck. What about the valuable space underneath and within the boundary of the MRT tracks? SMRT has more to lose if these assets were to be returned to the Government. Have a feeling that the SMRT managements have been doing the extremes. The past management concentrated on property development and neglected the O&M; the present one just doing the opposite. Chartwise, SMRT has not shown any determination to break the resistance of 1.32 and retreated from breaking it 2 days ago. If SMRT continues to fall and breaks 1.16, it would want to try to find support around the 100-day, failing which, we should see SMRT meeting its "water-loo". The present chart indicated this counter is very much over-bought. |

|

|

|

Post by zuolun on May 2, 2014 14:16:19 GMT 7

As usual and expected, Malaysia government will bail MAS out.

Yes, My Singaporean friend bought afew million MAS shares at average cost 20.5 sen on 10 Mar 2014, after MH370 went missing. He's in-the-money but only locked in some profit on half the qty, the balance he is still holding it; betting that MAS will be bailed out with taxpayers money. Both MAS and SMRT are superb trading stocks which can be played both sides; long and short, short and long many rounds as they're GLC stocks (won't go bankrupt, downside is protected by dumb money or generous bail-out). MAS Vs SMRT |

|

|

|

Post by stockpicker on May 3, 2014 11:41:03 GMT 7

In its recent press release, it is clear that SMRT just wanted to hand back the rail asset to Government and keep the rest of profit generating assets. Back in 2000 when MRTC was converting to SMRT Corporation from a Government department in LTA to public company, SMRT paid a lease of $1/= on condition that SMRT will continue to maintain as well as replace the train assets except for the rolling stocks. Now that SMRT has used it for more than 14 years, it is finding it an increasing financing burden to replace the train assets and decided it is time to hand the assets back to the Government.

It is not sure what exactly is the SMRT's proposal. There are 3 possible scenarios when Government takes over the train assets.

1) Government pays SMRT at the market value

2) Government pays back SGD$1/=

3) SMRT pays Government for the losses of lease in the last 14 years...

Scenarios 1 & 2 is tantamount to bailing out SMRT. Scenario 3 will depend on how much will be the losses of lease. All the above scenarios suggested that SMRT is proposing to "take the cake and eat it" as SMRT only wants to reduce its financial burden and retains those profit generating assets such as advertisement and property assets.

As the sale of assets back to Government will likely needs cabinet approval and it is expected that the decision will take some parliamentary debates.

|

|

if the recent 19% (Apr 24, 2014) price surge is due to government intervention!?

if the recent 19% (Apr 24, 2014) price surge is due to government intervention!?