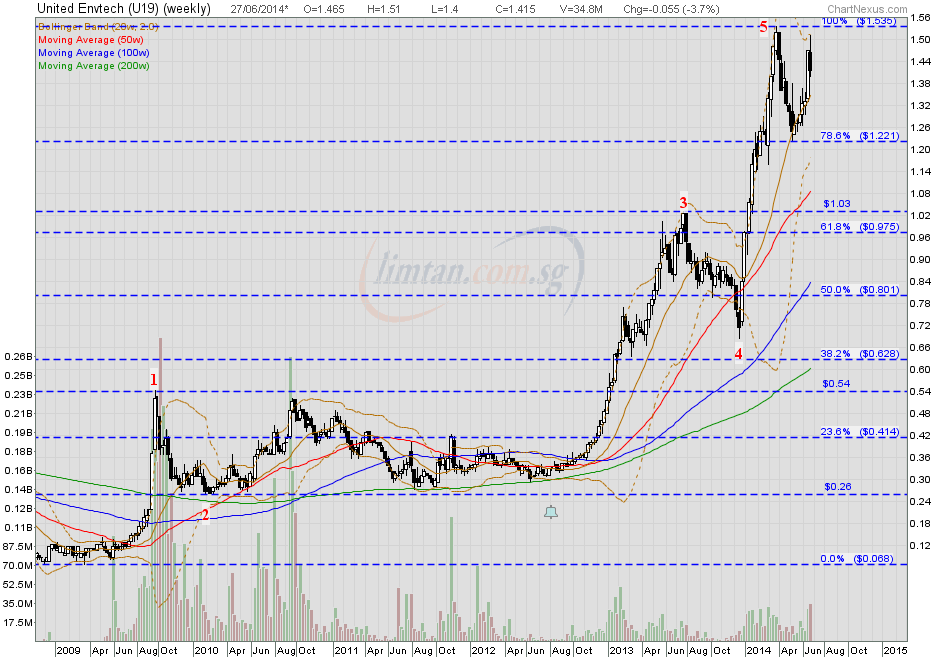

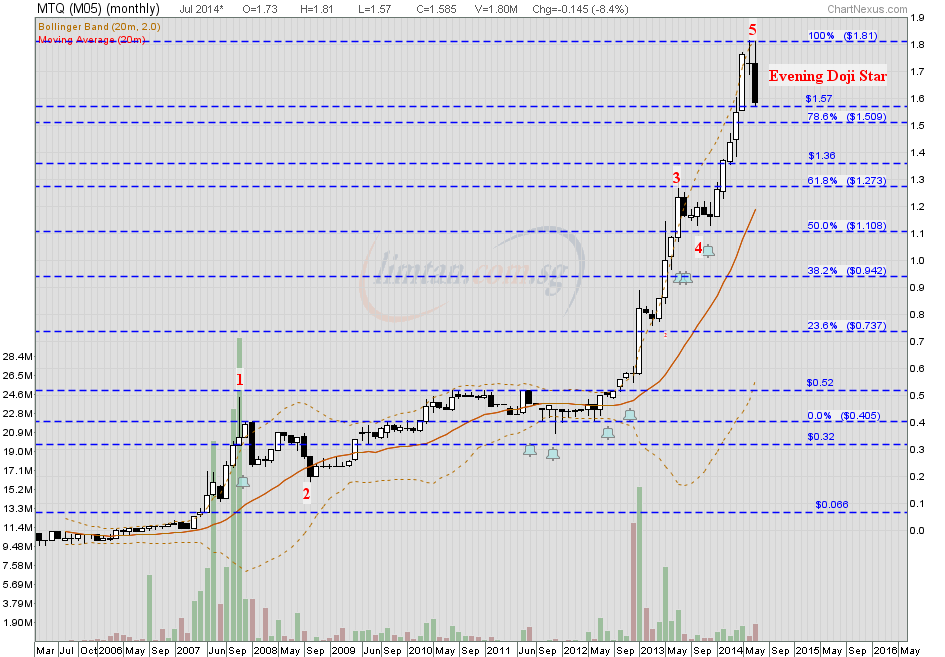

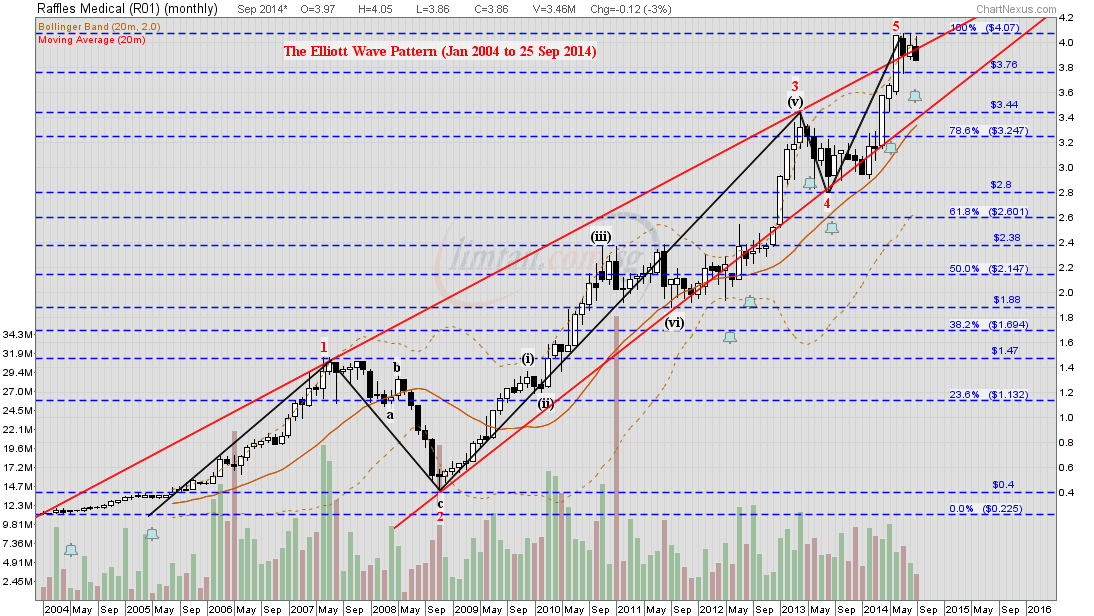

In the past, I used to focus almost exclusively on stocks which have significantly more assets than their market capitalisation. I liked stocks which had more cash than their market capitalisation as this then gives me their existing businesses and properties for free. One really cannot ask for a better margin of safety.

As the years went by, I looked at all the stocks that I have invested that have done well. Yes, all the stocks that I bought had this ridiculous margin of safety. But some stocks did well and others, not as well. So, I dissected each and every investment that I did over the past 10 years. I found out that the stocks that did very well belong to one or two categories.

Firstly, these were companies that were beaten down drastically by Mr Market and as a result, their share prices collapsed to below asset or sometimes, to below their cash value. These stocks were depressed because their core businesses suffered badly during the recession. But like all cyclical businesses, when the economy picks up, their businesses start flourishing and with it, their share prices. It was easy for me to hold on to these stocks because I bought most of these stocks at basement levels and as the company's prospects improved, I held on tightly to these stocks and only sold them when I felt that Mr Market had significantly over priced them. The best time to buy such companies is during a recession and hence, my general advice is to have sufficient money set aside for the next recession.

The second category were stocks that were transformed overnight by changes in the shareholding structure. As I also bought these stocks at basement levels, it was easy too for me to hold on to these and many of these returned me multiples of my original investment. Do note that I do not ride all these investments automatically. I would instead look at each and every situation and assess each one separately and only if I am comfortable with the proposed business model, will I continue riding these stocks. If I was in any doubt, I will not hesitate to liquidate my position and take immediate profits from the table.

Now, to the more interesting finding. For my investments that did not do so well, they also fall into 2 categories. Firstly, when I bought into these companies, they had more cash than their market capitalisation. However, as the years went by, these companies lose even more money and their cash reserves dwindle with time. Some, continue paying their management well and others, bought into obvious money losing businesses. In some of these cases, management own a small percentage of the shares while in others, management were the majority shareholders. Regardless, the company continued to drain money and as a result, my margin of safety deteriorated as the years went by. As I usually invest in small listed companies, they all still have a listed shell value on top of their asset value. Sooner or later, these stocks will become acquisition targets for others, so long as they are not delisted by the stock exchange.

The second category for my stocks that did not do so well are those stocks that became targets for reverse takeovers. These takeovers were arranged in such a way that the new shareholders benefited tremendously more than the existing shareholders. The existing management benefited from acquiring the existing businesses for very little or are assured of good executive salaries to take care of the original businesses before being granted the option to buy these businesses over cheaply. It is true that these stocks usually multiply in value on the announcement of the takeover but with time, their share price is more likely to decline. I usually sell these stocks on the euphoria of the announcements especially when I am not in favour of the terms and conditions of the proposed takeover. Usually, the way they structure a deal is a good reflection of the way they are likely to treat minority shareholders once the deal goes through.

So, at the end of the day, the success of my investments was not because I bought into undervalued companies but was because these companies were able to increase their profits significantly. Some did it organically by riding on its existing businesses when the economy recovered. Others did it by acquisition of a new business that delivered ever increasing profits. If you want your investments to multiply in value, you have to ride the profit making ability of these companies as the stock market values companies by giving a multiple of their profits and not a multiple of their assets.

Saying all that, I will still look for companies that give me that ridiculous margin of safety. Without this ridiculous margin of safety, I would not have the guts to hold on to these stocks and ride them all the way upwards. On top of this margin of safety, I am now more inclined to consider the future profitability of the company. So, this is really a refinement of my investment strategy.

For completeness, it is best for me to clarify what I mean by stocks that did well and stocks that did not do so well. When my stocks did well, they returned me multiples of my original investment. When my stocks did not do so well, they still give me a very good return. Most of these return me over 50% above my original investment capital. Some of the stocks that did not do well gave me double or triple my original investments but when compared to the shares that did well, they pale in comparison with regards to the return on my capital.

As you age, you will realise that time is not on your side and hence, the refinement of my original investment strategy to extract an even higher rate of return on my capital.

PS - Do read my article on investing in top entrepreneurs as it answers the questions in your second paragraph:

Investing in top entrepreneurs